ホスホン酸塩:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Phosphonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690961

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

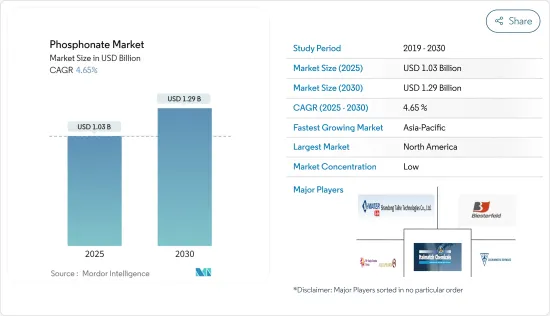

ホスホン酸塩市場規模は2025年に10億3,000万米ドルと推定され、2030年には12億9,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは4.65%です。

水処理産業の前向きな展望と、最近の洗剤・洗浄剤産業の着実な進展が、今後数年間のホスホン酸塩需要を牽引するとみられます。

主要ハイライト

- 水処理産業におけるホスホン酸塩の用途は広いです。洗浄剤・洗剤産業の急成長も、ホスホン酸塩の需要を牽引すると予想されます。

- しかし、ホスホン酸塩の非分解性による環境問題への懸念や、代替品の入手可能性が市場の成長を妨げると予想されます。

- ホスホン酸塩のプロドラッグやナノ多孔性ホスホン酸塩への新たな応用は、調査対象市場に新たな機会をもたらすと期待されています。

- アジア太平洋が市場を独占し、中国とインドからの需要が大半を占めると予想されます。

ホスホン酸塩市場の動向

水処理産業における需要の増加

- ホスホン酸塩の一種である正リン酸塩とポリリン酸塩は、水処理において極めて重要な役割を果たしています。その主要機能は、特に鉛や銅などのパイプからの腐食や金属溶出を抑制することです。リン酸塩はこれらの金属と反応することで、溶解性の低い化合物を形成し、汚染のリスクを最小限に抑えます。さらに、リン酸塩は鉄やマンガンを隔離し、水の変色を防ぎます。

- 水処理とは、化学品を使用してスケーリングを除去・防止し、腐食を抑え、バクテリアや藻類を死滅させ、水を浄化する先進的技術です。水処理薬品には主に、凝集剤、殺生物剤、スケール防止剤の3種類があります。

- HEDPホスホン酸塩は、さまざまな工業用水処理プロセスで化学添加剤として一般的に使用されています。HEDPはスケール防止剤の一種で、スケールや汚れを防止することができます。

- その他のスケール防止剤と比較して、HEDPには多くの利点があります。優れた耐汚れ性、低汚染性、優れた溶解性、優れた相乗効果を発揮します。

- 温室効果ガスの拡散による気候の変化によって、米国やメキシコなどの国々では干ばつの頻度が大幅に増加しています。

- 米国の干ばつモニターが報告しているように、2023年には米国の約28%が干ばつ状態に直面し、深刻なカテゴリーはここ数ヶ月で急増しています。このような干ばつは、地下水、ダム、運河の水を含む国の淡水資源を著しく枯渇させ、清潔な飲料水の危機的な不足につながります。

- 地方自治体の廃水を処理するために、いくつかの下水道インフラが整備されています。米国では、毎日約340億ガロンの廃水が処理されています。この都市廃水には、食品、屎尿、石鹸、洗剤から発生する窒素とリンがほとんど含まれています。

- 各国政府は、北米全域で廃水処理施策の推進に投資しています。例えば、米国環境保護庁は2024年2月、清潔な飲料水と廃水インフラのために約60億米ドルを投資すると発表しました。

- さらにインドでは、水不足と闘うために先進的な下水道計画が実施されています。AMRUT(Atal Mission for Rejuvenation & Urban Transformation)、Swachh Bharat Mission(Urban) 2.0、Smart Cities Missionといった取り組みが、住宅都市省の下でこうした取り組みを推進しています。

- 2022年12月、国家河川保全計画(NRCP)は、36の河川の汚染防止対策に約754億7,800万米ドル(6兆2,481億6,000万インドルピー)を計上しました。これらの治療は16州の80の町にまたがり、汚染対策として1日あたり27億4,570万リットル(MLD)の汚水処理能力を確立することを目指しています。

- 近年、産業部門からの水需要の増加と、水質汚染抑制を目的とした政府規制の進展が相まって、水処理ソリューションに対する需要の高まりに拍車をかけています。

- 工業団地における新たな水処理施設への投資が、調査対象市場の需要を押し上げると予想されます。例えば

- 2024年1月、ロートゲン出身のメンビオンは、画期的なメンビオンMBRモジュールに対して500万ユーロ(約550万米ドル)の投資を獲得しました。この特許取得済みのモジュールは、スペース効率が高く、占有面積が75%削減され、廃水中の細菌負荷を従来のプラントを凌ぐ1,000分の1に減少させることができます。このモジュールは、都市廃水と工業廃水の両方の治療用に設計されています。

- 2023年10月、ウォーター・コーポレーションはオーストラリアのモワンジュム廃水処理プラントの830万米ドル相当のアップグレードを完了しました。この取り組みは、新しいアボリジニ・コミュニティ・ウォーターサービス(ACWS)プログラムの一環であり、アボリジニ・コミュニティで初の認可プラントとなります。

- 2023年6月、米国環境保護庁(EPA)は、アメリカンインディアンとアラスカ先住民の部族のための上下水道インフラを強化するため、2億7,800万米ドルを超える画期的な投資を発表しました。

- 水不足と資源の減少に伴い、水処理に対する需要は世界的に高まっており、予測期間中にホスホン酸塩の巨大市場が形成されると予想されます。

アジア太平洋がホスホン酸塩市場を独占する見込み

- アジア太平洋は、中国、インド、日本などの国々における水使用量の増加により、ホスホン酸塩の消費量が増加し、ホスホン酸塩市場をリードしています。

- 中国とインドは、洗剤、水処理、油田用化学品、化粧品、その他の最終用途産業からの需要が高いため、ホスホン酸塩市場を牽引することになると考えられます。

- 中国では、特にCOVID-19の大流行後、衛生意識が高まり、特にタイルやフローリングの使用が一般的であることから、高級床クリーナーの需要に拍車がかかっています。

- インドは世界最大の洗剤生産・供給国のひとつです。インドにおける繊維用洗剤の需要は、主に洗濯機の普及率上昇に牽引されています。

- 主要洗剤メーカーは、市場の成長を後押しするため、製品の革新や新しい施設の設立を進めています。例えば

- 2023年12月、ゴドレイコンシューマー・プロダクツ(GCPL)は、洗濯体験の変革を目指した液体洗剤「Godrej Fab」を発売しました。

- 2022年5月には、Procter & Gamble(P& G)がインドのハイデラバード郊外に、20億インドルピー(2,683万米ドル)を投資して液体洗剤の製造装置を稼働させました。

- India Brand Equity Foundation(IBEF)は、インドの食器洗い機市場が、デリー、ムンバイ、バンガロールなどの大都市の需要に後押しされ、2025~2026年までに9,000万米ドルを超えると予測しています。

- このような動向から、アジア太平洋のホスホン酸塩市場は今後も安定した成長が見込まれます。

ホスホン酸塩産業概要

世界のホスホン酸塩市場は細分化されています。主要参入企業(順不同)には、Italmatch Chemicals、Shandong Taihe Water Treatment Technologies、Biesterfeld AG、Aquapharm Chemical Pvt. Ltd、Zschimmer & Schwarz Chemie GmbHなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場の促進要因

- 水処理産業におけるホスホン酸塩の幅広い用途

- 洗浄剤・洗剤産業の急成長

- その他の促進要因

- 市場抑制要因

- 非分解性による環境への影響

- 代替品の入手可能性

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ別

- ATMP

- HEDP

- DTPMP

- その他

- エンドユーザー産業別

- 洗剤・洗浄剤

- 水処理

- 油田用化学品

- 化粧品

- 建築材料

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Aquapharm Chemical Pvt. Ltd

- Biesterfeld AG

- Bozzetto Group

- Changzhou Kewei Fine Chemicals Co. Ltd

- Excel Industries

- Italmatch Chemicals

- Jiangsu Yuanquan Hongguang Environmental Protection Technology Co. Ltd

- Jiyuan Qingyuan Water Treatment Co. Ltd

- Mks DevO Chemicals

- Shandong IRO Water Treatment Co. Ltd

- Shandong Kairui Chemistry Co. Ltd

- Shandong Taihe Watre Treatment Technologies Co. Ltd

- ShanDong XinTai Water Treatment Technology Co. Ltd

- Uniphos Chemicals

- Zschimmer & Schwarz Chemie GmbH

第7章 市場機会と今後の動向

- プロドラッグとナノ多孔性ホスホン酸塩におけるホスホン酸塩の新たな用途

- その他の機会

目次

The Phosphonate Market size is estimated at USD 1.03 billion in 2025, and is expected to reach USD 1.29 billion by 2030, at a CAGR of 4.65% during the forecast period (2025-2030).

The positive outlook of the water treatment industry and steady progress in the detergent and cleaning agent industry in recent times are likely to drive the demand for phosphonates in the coming years.

Key Highlights

- There are wide applications of phosphonates in the water treatment industry. The rapid growth of the cleaners and detergents industry is also expected to drive the demand for phosphonates.

- However, environmental concerns due to its non-degradable nature and availability of substitutes are expected to hinder the market's growth.

- Nevertheless, emerging applications of phosphonates in pro-drugs and nano-porous phosphonates are expected to create new opportunities for the market studied.

- Asia-Pacific is expected to dominate the market, with the majority of demand coming from China and India.

Phosphonate Market Trends

Increasing Demand in the Water Treatment Industry

- Orthophosphate and polyphosphates, types of phosphonates, play a pivotal role in water treatment. Their primary function is to curb corrosion and metal leaching from pipes, notably lead and copper. By reacting with these metals, phosphates form less soluble compounds, thereby minimizing contamination risks. Furthermore, phosphates sequester iron and manganese, averting water discoloration.

- Water treatment is an advanced technique that uses chemicals to eliminate and prevent scaling, reduce corrosion, kill bacteria and algae, and purify water. There are three main types of water treatment chemicals: flocculants, biocides, and scale inhibitors.

- HEDP phosphonate is commonly used as a chemical additive in various industrial water treatment processes. HEDP is a type of scale inhibitor that can prevent scale and dirt.

- Compared to other scale inhibitors, HEDP has many advantages. It provides excellent dirt resistance, low pollution, good dissolution, and good synergy.

- The changing climate due to the proliferation of greenhouse gases has greatly increased the frequency of droughts in countries like the United States and Mexico.

- As reported by the US Drought Monitor, in 2023, around 28% of the United States faced drought conditions, with severe categories spiking in recent months. These droughts severely deplete the country's freshwater resources, including groundwater, dams, and canal water, leading to a critical shortage of clean drinking water.

- Several sewerage infrastructures have been created to process municipal wastewater. In the United States, approximately 34 billion gallons of wastewater is being processed every day. This municipal wastewater mostly contains nitrogen and phosphorus from food, human waste, soaps, and detergents.

- Governments are investing in promoting wastewater treatment policies across North America. For instance, in February 2024, the US EPA announced an investment of nearly USD 6 billion for clean drinking water and wastewater infrastructure.

- Furthermore, in India, advanced sewerage programs are being implemented to combat water scarcity. Initiatives like the Atal Mission for Rejuvenation & Urban Transformation (AMRUT), Swachh Bharat Mission (Urban) 2.0, and the Smart Cities Mission are driving these efforts under the Ministry of Housing & Urban Affairs.

- In December 2022, the National River Conservation Plan (NRCP) earmarked approximately USD 75,478 million (INR 6,248,160 million) for pollution control efforts on 36 rivers. These efforts span 80 towns across 16 states and aim to establish a sewage treatment capacity of 2,745.7 million liters per day (MLD) to combat pollution.

- In recent years, rising water demand from the industrial sector, coupled with evolving government regulations aimed at curbing water pollution, have spurred a heightened demand for water treatment solutions.

- Investments in new water treatment facilities in industrial complexes are expected to boost the demand of the market studied. For instance,

- In January 2024, Membion, hailing from Roetgen, garnered an investment of EUR 5 million (~USD 5.5 million) for its groundbreaking Membion MBR modules. These patented modules are space-efficient, occupying 75% less area, and can diminish bacterial load in wastewater by 1,000 times, surpassing traditional plants. They are designed for both municipal and industrial wastewater treatment.

- In October 2023, Water Corporation completed an upgrade worth USD 8.3 million to the Mowanjum wastewater treatment plant in Australia. This initiative is part of a new Aboriginal Communities Water Services (ACWS) program, leading to the first licensed plant in an Aboriginal community.

- In June 2023, The US Environmental Protection Agency (EPA) unveiled a landmark investment exceeding USD 278 million to enhance water and wastewater infrastructure for American Indian and Alaska Native tribes, marking the largest annual funding allocation for such initiatives.

- With rising water scarcity and fewer resources, the demand for water treatment is increasing globally, which is expected to provide a huge market for phosphonates during the forecast period.

Asia-Pacific Expected to Dominate the Phosphonate Market

- Asia-Pacific leads the phosphonate market, driven by rising water usage in nations like China, India, and Japan, subsequently boosting phosphonate consumption.

- China and India are set to propel the phosphonate market due to high demand from detergents, water treatment, oil field chemicals, cosmetics, and other end-use industries.

- Heightened hygiene awareness in China, especially after the COVID-19 pandemic, has spurred demand for premium floor cleaners, especially with the country's common use of tile and wood flooring.

- India is one of the largest producers and suppliers of detergent globally. The demand for fabric detergents in India is mainly driven by the rising penetration of washing machines.

- Key detergent manufacturers are innovating products and establishing new facilities to bolster the market's growth. For instance,

- In December 2023, Godrej Consumer Products (GCPL) launched "Godrej Fab," a liquid detergent aimed at transforming the laundry experience.

- In May 2022, Proctor & Gamble (P&G) inaugurated its inaugural liquid detergent manufacturing unit on the outskirts of Hyderabad, India, with an investment of INR 200 crore (USD 26.83 million).

- The India Brand Equity Foundation (IBEF) projects India's dishwasher market to exceed USD 90 million by 2025-2026, spurred by demand in major cities like Delhi, Mumbai, and Bangalore.

- Due to these trends, the Asia-Pacific phosphonate market is set for consistent growth in the years ahead.

Phosphonate Industry Overview

The global phosphonate market is fragmented in nature. The major players (not in any particular order) include Italmatch Chemicals, Shandong Taihe Water Treatment Technologies Co. Ltd, Biesterfeld AG, Aquapharm Chemical Pvt. Ltd, and Zschimmer & Schwarz Chemie GmbH.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Wide Applications of Phosphonates in the Water Treatment Industry

- 4.1.2 Rapid Growth of the Cleaners and Detergents Industry

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Environmental Impact Due to Non-Degradable Nature

- 4.2.2 Availability of Substitutes

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Types

- 5.1.1 ATMP

- 5.1.2 HEDP

- 5.1.3 DTPMP

- 5.1.4 Other Types

- 5.2 By End-user Industry

- 5.2.1 Detergent and Cleaning Agent

- 5.2.2 Water Treatment

- 5.2.3 Oil field chemicals

- 5.2.4 Cosmetics

- 5.2.5 Building Materials

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aquapharm Chemical Pvt. Ltd

- 6.4.2 Biesterfeld AG

- 6.4.3 Bozzetto Group

- 6.4.4 Changzhou Kewei Fine Chemicals Co. Ltd

- 6.4.5 Excel Industries

- 6.4.6 Italmatch Chemicals

- 6.4.7 Jiangsu Yuanquan Hongguang Environmental Protection Technology Co. Ltd

- 6.4.8 Jiyuan Qingyuan Water Treatment Co. Ltd

- 6.4.9 Mks DevO Chemicals

- 6.4.10 Shandong IRO Water Treatment Co. Ltd

- 6.4.11 Shandong Kairui Chemistry Co. Ltd

- 6.4.12 Shandong Taihe Watre Treatment Technologies Co. Ltd

- 6.4.13 ShanDong XinTai Water Treatment Technology Co. Ltd

- 6.4.14 Uniphos Chemicals

- 6.4.15 Zschimmer & Schwarz Chemie GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications of Phosphonates in Pro-drugs and Nano-porous Phosphonates

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日