|

市場調査レポート

商品コード

1690951

北米のマネージドサービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のマネージドサービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

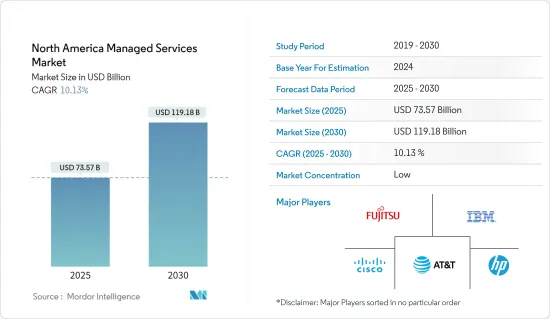

北米のマネージドサービス市場規模は、2025年に735億7,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは10.13%で、2030年には1,191億8,000万米ドルに達すると予測されます。

主なハイライト

- 北米市場は、ITインフラ、特にサイバーセキュリティソリューションのアウトソーシングに継続的に注力している中小企業(SME)の状況の変化により成長しています。例えば、米国の新興ITサプライ製造・販売業者の1つであるKPaul Properties LLCは、富士通を導入して物理サーバーを仮想化環境に置き換えました。これにより、同社のコストは約15%削減され、稼働率は95%に達しました。

- ソーラーウィンズ社によると、北米、特に米国では、サーバ、ストレージハードウェア、エンドポイントデバイス、ネットワーク機器のソリューション提供がMSPの主流となっています。マネージドセキュリティの提供は不足しているかもしれないが、ほとんどのソリューション・プロバイダーは、ネットワークとエンドポイントのハードウェアとソフトウェアでセキュリティ・ポイント製品を提供しています。

- この地域では、IT環境の完全な評価を行い、ビジネスライフサイクルの各段階で複雑なビジネス課題を解決するために必要なソリューションを提供することで、ビジネスニーズに合わせたITソリューションを統合しています。例えば、米国のマネージドソリューション社は、技術的なスキルセットと必要なリソースを統合し、課題の発見、問題領域の診断、ニーズに基づいた包括的な技術ロードマップのカスタム設計、提供、実行を行い、顧客の安全性、コンプライアンス、効率性を高めています。

- マネージドサービスには様々な利点があるが、信頼性の問題など特有の課題があり、予測期間中の市場の成長を妨げる可能性があります。重要なビジネス・インフラのホスティングをMSPに依頼するプロセスには、プロバイダーとの信頼関係が不可欠です。プロバイダーが競争市場で存続できない場合、プロバイダーに依存している企業は、ウェブホスティング、電子メール、カレンダー、その他の重要なインフラを全面的に交換しなければならない可能性があります。

- COVID-19の大流行により、米国ではリモートで仕事をする組織の数が増加しました。ALM Media Properties LLCによると、アメリカの知識労働者の推定58%がリモートで働いています。この数字はCOVID-19以前の平均から30%以上増加しており、米国の民間従業員1億4,000万人のうちおよそ7%が在宅勤務であると報告されていた以前の数字を凌駕しています。このような従来の職場からの大量流出は、多くの組織で雇用者の期待やテレワークポリシーに歓迎すべき変化をもたらしています。

北米のマネージドサービス市場の動向

IT・通信分野が大きな市場シェアを占める見込み

- IT・通信分野は、さまざまな技術の採用率の高さ、BYODポリシーの採用率の増加(業務運営をより快適で管理しやすいものにするため)、組織におけるデータ量の急増によるハイエンド・セキュリティのニーズの高まりなどから、マネージドサービスの重要な市場となっています。

- 通信業界はここ数年、成長を続けています。競争の激しい市場で顧客を維持するため、通信会社は革新的なサービスを低コストで提供しなければならないというプレッシャーに常にさらされているからです。複雑な競合環境に対応するため、マネージドサービスは通信事業者の幅広い需要となっています。

- さらに、その説得力のある経済的事例から、ほとんどの通信キャリアはネットワークハードウェアをソフトウェア(SDN &NFV)に置き換えると予想されています。SDNとNFVの需要を促進する主な要因には、市場投入までの時間の改善、CAPEXとOPEXの削減、ビジネスの観点からの新たな収入源の開拓などがあります。これらすべてが、調査された市場の成長を促進すると予想されます。このような取り組みがマネージドネットワークサービスの需要を促進しています。

- 北米の多くのSD-WANマネージドサービスプロバイダーは、幅広いセキュリティを提供することで差別化を図っています。例えば、Cato NetworksはNGFW、Secure Web Gateway、Advanced Threat Prevention、Cloud and Mobile Access Protection、Managed Threat Detection and Responseサービスを含むクラウドネイティブなプラットフォームを提供しています。コルトはレイヤー7ファイアウォールやDDoS防御機能付きレイヤー3/4ステートフル・ファイアウォールを提供し、センチュリーリンクはアダプティブ・ネットワーク・セキュリティと呼ばれる一連のセキュリティ・サービスを提供しています。

急成長が期待されるカナダ市場

- カナダのマネージドサービス市場は、主に新製品の展開、買収、合併、提携によって成長しており、北米市場全体を形成しています。カナダではテクノロジーの成長が加速しており、業務効率の向上、膨大なデータの活用、社内でのコラボレーション、企業と顧客間の交流など、ビジネスのあり方を変え続けています。

- スターポートはカナダを拠点とするマネージドITサービス・プロバイダーで、カナダ全土の中堅企業にトップクラスのIT設計、導入、継続的なネットワーク監視を提供しています。顧客の大半はグレーター・トロント・エリアに集中しています。投資銀行、製造業、商業不動産など、さまざまな業界の顧客にサービスを提供しています。

- また、カナダではマルチクラウド環境の適用や自動化の導入が進んでいます。同地域では、クラウド、モバイル、ソーシャル技術により、企業はITセキュリティに対して積極的なアプローチを取ることが求められているため、あらゆるセキュリティ管理レイヤーを提供する堅牢なマネージドサービスの展開に対する需要が高まっています。

- サービスとしてのユニファイド・コミュニケーション(UCaaS)と関連するサービスとしてのコンタクトセンター(CCaaS)市場は、マネージドサービス・プロバイダーにとってビジネスチャンスです。新興プロバイダーが、最小限の投資で導入できる革新的なクラウドベースのソリューションを提供しているからです。また、顧客は消費型の従量課金モデルに傾いています。

- カナダにおけるクラウドサービスの増加は、マネージドMPLS市場の需要を拡大すると予想されます。例えば、カナダ政府は「クラウドファースト」戦略を掲げており、情報技術への投資、イニシアチブ、戦略、プロジェクトを開始する際に、主要な提供オプションとしてクラウドサービスを特定・評価しています。また、クラウドによって、カナダ政府は民間プロバイダーのイノベーションを活用し、情報技術の機動性を高めることができると期待されています。

北米のマネージドサービス業界の概要

マネージドサービス市場は、複数の大手企業が存在するため競争が激しいです。同市場の主要企業には、シスコシステムズ社、IBM社、マイクロソフト社、富士通社、ウィプロ社などがあります。市場競争は激化の一途をたどっており、各社は戦略的提携やパートナーシップを結んでいます。

- 2021年5月- 富士通株式会社と楽天モバイル株式会社は、世界市場向けのOpen RANソリューションの共同開発における協力関係を深めるための覚書を締結したと発表しました。両社は、4Gおよび5GのOpen RANソリューションの開発を共同で行う。

- 2021年11月-AT&Tはセキュア・アクセス・サービス・エッジ(SASE)ポートフォリオに新たな製品を追加しました。AT&T SASE with Ciscoは、Software-Defined Wide-area Networking(SD-WAN)技術とセキュリティ機能を活用し、ビジネスの接続と保護を実現するネットワークとセキュリティの統合管理システム。

- 2021年10月- シトリックスは、マネージド、アンマネージド、BYO(Bring-Your-Own)デバイスからのアプリとデータアクセスを保護する新しいクラウドベースのZero-Trust Network Access(ZTNA)ソリューション、Citrix Secure Private Accessを発表。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- ハイブリッドITへのシフトの増加

- コストと業務効率の改善

- 市場の課題

- 統合、規制問題、信頼性への懸念

第6章 市場セグメンテーション

- 展開別

- オンプレミス

- クラウド

- タイプ別

- マネージドデータセンター

- マネージドセキュリティ

- マネージドコミュニケーション

- マネージドネットワーク

- マネージドインフラストラクチャ

- マネージドモビリティ

- 企業規模別

- 小企業

- 中堅企業

- 大企業

- 業界別

- BFSI

- IT・通信

- ヘルスケア

- エンターテイメント・メディア

- 小売

- 製造業

- 政府機関

- その他業界別

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Fujitsu Ltd

- Cisco Systems Inc.

- IBM Corporation

- AT&T Inc.

- HP Development Company LP

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Citrix Systems Inc.

- Rackspace Inc.

第8章 投資分析

第9章 市場の将来

The North America Managed Services Market size is estimated at USD 73.57 billion in 2025, and is expected to reach USD 119.18 billion by 2030, at a CAGR of 10.13% during the forecast period (2025-2030).

Key Highlights

- The North American market is growing due to the changing landscape of IT infrastructure, especially in small and medium enterprises (SMEs), which continually focus on outsourcing cybersecurity solutions. For instance, KPaul Properties LLC, one of the emerging manufacturers and distributors of IT supplies in the United States, onboarded Fujitsu to replace a physical server with a virtualized environment. This reduced the company's cost by around 15% and delivered 95% uptime.

- According to SolarWinds, in North America, server and storage hardware, endpoint devices, and networking gear solution offerings dominate among MSPs, especially in the United States. Though managed security offerings may be lacking, most solution providers offer security point products in network and endpoint hardware and software.

- In the region, companies are integrating IT solutions tailored to business needs by providing a full assessment of the IT environment and delivering the solutions needed to solve complex business challenges at every stage of the business lifecycle. For instance, Managed Solution, a US company, integrated technical skillsets and the required resources to discover challenges, diagnose problem areas, and custom design, deliver, and execute a comprehensive technology roadmap based on needs, making customers more secure, compliant, and efficient.

- Although managed services offer various benefits, specific challenges, like reliability concerns, may obstruct the market's growth over the forecast period. The process of hiring an MSP to host critical business infrastructure involves a belief in the providers' business relationship. In case of any failure by providers to sustain in the competitive market, enterprises relying upon them may have to entirely replace web hosting, emails, calendars, and other critical pieces of infrastructure, without which it is not possible to conduct business.

- The COVID-19 pandemic increased the number of organizations working remotely in the United States. According to ALM Media Properties LLC, an estimated 58% of American knowledge workers work remotely. This number is increasing by more than 30% from pre-COVID-19 averages and dwarfs previous figures that reported roughly 7% of the US' 140 million civilian employees worked from home. This mass exodus from the conventional workplace has been a welcome shift in many organizations' employer expectations and telework policies.

North America Managed Services Market Trends

IT and Telecom Sector Expected to Hold a Significant Market Share

- The IT and telecom sector is a significant market for managed services due to the high rate of various technological adoptions, increased rate of adoption of the BYOD policy (in order to make business operations much more comfortable and controllable), and increased need for high-end security due to rapidly increasing data volumes in organizations.

- The telecom industry has observed increased growth during the past few years as telecommunication companies are encountering constant pressure to deliver innovative services at lower costs to retain their customers in the competitive market. In order to address a complex and competitive environment, managed services have become a widespread demand for operators.

- Moreover, because of their compelling economic case, most telecom carriers are expected to replace their network hardware with software (SDN & NFV). Major factors driving the demand for SDN and NFV include improved time-to-market, reduction in CAPEX and OPEX, and opening up new revenue streams from a business standpoint. All these are expected to drive the growth of the market studied. Such initiatives are driving demand for managed network services.

- Many SD-WAN managed service providers in North America differentiate themselves with a broad range of security offerings. For instance, Cato Networks offers a cloud-native platform that includes NGFW, Secure Web Gateway, Advanced Threat Prevention, Cloud and Mobile Access Protection, and a Managed Threat Detection and Response service. Colt offers Layer 7 firewall or a Layer 3/4 stateful firewall with DDoS protection, and CenturyLink provides a suite of security services referred to as Adaptive Network Security.

Canada Expected to be the Fastest-growing Market

- The market for managed services in Canada is growing mainly due to new product roll-outs, acquisitions, mergers, and partnerships, shaping the overall North American market. The accelerated growth of technology in Canada continues to reshape how businesses improve operational efficiencies, leverage massive amounts of data, collaborate internally, and interaction between businesses and customers.

- Starport is a Canada-based managed IT services provider that delivers top-class IT design, implementation, and continuous network monitoring to mid-sized organizations, throughout Canada. Most of its clients are concentrated in the Greater Toronto Area. It offers its services to clients from various industries, including investment banking, manufacturing, and commercial real estate.

- Besides, Canada is witnessing high growth in the application of multi-cloud environments and increased adoption of automation. In the region, cloud, mobile, and social technologies demand that businesses take a proactive approach toward IT security, thus, boosting the demand for the deployment of robust managed services that would deliver in all security management layers.

- Unified Communications as a Service (UCaaS) and related Contact Center as a Service (CCaaS) markets represent a business opportunity for managed service providers. This is because emerging players are offering innovative cloud-based solutions that require a minimum investment and are easy to deploy. Customers are also leaning toward consumption-based, pay-as-you-go models.

- Rising cloud services in the country are expected to augment the demand for the managed MPLS market. For instance, the Government of Canada has a 'cloud-first' strategy, whereby cloud services are identified and evaluated as the principal delivery option while initiating information technology investments, initiatives, strategies, and projects. The cloud is also expected to allow the Government of Canada to harness the innovation of private sector providers to make its information technology more agile.

North America Managed Services Industry Overview

The managed services market is very competitive because of the presence of several major players. Some major players in the market are Cisco Systems Inc., IBM Corporation, Microsoft Corporation, Fujitsu Ltd, and Wipro Ltd. The market players are forming strategic collaborations and partnerships to sustain the intense competition in the market.

- May 2021 - Fujitsu Ltd and Rakuten Mobile Inc. announced a Memorandum of Understanding (MoU) to deepen their collaboration on joint efforts to develop Open RAN solutions for the global market. Both companies will jointly collaborate to develop 4G and 5G Open RAN solutions.

- November 2021 - AT&T added a new offering to its Secure Access Service Edge (SASE) portfolio. AT&T SASE with Cisco is a converged network and security management system that uses software-defined wide-area networking (SD-WAN) technology and security capabilities to connect and protect businesses.

- October 2021 - Citrix launched Citrix Secure Private Access, a new cloud-based Zero-Trust Network Access (ZTNA) solution that safeguards app and data access from managed, unmanaged, and Bring-Your-Own (BYO) devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Shift to Hybrid IT

- 5.1.2 Improved Cost and Operational Efficiency

- 5.2 Market Challenges

- 5.2.1 Integration, Regulatory Issues, and Reliability Concerns

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Managed Data Center

- 6.2.2 Managed Security

- 6.2.3 Managed Communications

- 6.2.4 Managed Network

- 6.2.5 Managed Infrastructure

- 6.2.6 Managed Mobility

- 6.3 By Enterprise Size

- 6.3.1 Small Enterprises

- 6.3.2 Medium Enterprises

- 6.3.3 Large Enterprises

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 IT and Telecom

- 6.4.3 Healthcare

- 6.4.4 Entertainment and Media

- 6.4.5 Retail

- 6.4.6 Manufacturing

- 6.4.7 Government

- 6.4.8 Other End-user Verticals

- 6.5 By Country

- 6.5.1 United States

- 6.5.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Ltd

- 7.1.2 Cisco Systems Inc.

- 7.1.3 IBM Corporation

- 7.1.4 AT&T Inc.

- 7.1.5 HP Development Company LP

- 7.1.6 Microsoft Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Citrix Systems Inc.

- 7.1.10 Rackspace Inc.