世界のヘルスケア相互運用性ソリューション- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Global Healthcare Interoperability Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690937

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

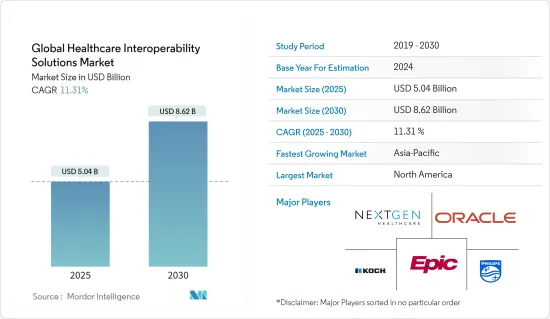

世界のヘルスケア相互運用性ソリューション市場規模は、2025年に50億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.31%で、2030年には86億2,000万米ドルに達すると予測されます。

COVID-19パンデミックは、COVID-19患者の急増により世界経済とヘルスケアインフラに大きな影響を与えました。さまざまな健康状態にあるCOVID-19患者が予期せぬ形で流入し、ヘルスケア提供施設の一般的な機能を混乱させたためです。例えば、2021年2月に発表された「COVID-19 Highlights Need for Laboratory Data Sharing and Interoperability」と題された記事によると、SARS-CoV-2パンデミックの結果、相互運用可能なヘルスケアシステムの必要性が明らかになりました。さらに同じ情報源によれば、相互運用可能なヘルスケアシステムによって、COVID-19に対する国の対応は大幅に改善されます。例えば、患者は症状をヘルスケア提供者に連絡することができ、ヘルスケア提供者は患者の完全なヘルスケア情報に迅速にアクセスし、根本的な問題を治療することができます。したがって、COVID-19パンデミックはヘルスケア相互運用性ソリューション市場に大きな影響を与えると予想されます。

ヘルスケア相互運用性ソリューション市場の成長を促進すると予想される主要因には、世界中のヘルスケアプロバイダによるデジタルヘルスケアソリューションの採用と投資の増加、ヘルスケア費増加に対する懸念の高まりなどがあります。ヘルスケア相互運用性ソリューションは、増加するヘルスケア費の削減に役立つため、予測期間中により広く採用され、市場の成長が見込まれています。例えば、ヘルスケア相互運用性ソリューションを採用する主要利点として、ヘルスケア効率の向上、ヘルスケアの質と患者の体験の改善、ヘルスケア費の削減、医師の燃え尽き症候群の緩和などが挙げられます。したがって、ヘルスケアITと相互運用性ソリューションへの投資は予測期間中に増加すると予想され、これがヘルスケア相互運用性ソリューション市場の成長を促進すると期待されています。例えば、2020年9月、米国のヘルスケア情報技術国家調整官室は、ヘルスケアエコシステム全体におけるヘルスケアIT標準の採用と使用のための新たな機会の探求のために、ヘルスケア情報技術におけるリーディングエッジアクセラレーションプロジェクトプログラムの下で、4つの組織に合計270万米ドルの資金を報奨しました。

さらに、世界中で増加するヘルスケア支出は政府にとって大きな懸念事項の一つであり、これを削減するためにヘルスケアITソリューションが採用・導入されています。例えば、ドイツ連邦統計局(Destatis)の2022年6月の報告書によると、ドイツのヘルスケア支出は年々増加しており、2020年には4,410億ユーロに達しています。

さらに、市場参入企業によるこのセグメントでの新製品の発売は、ヘルスケア相互運用性ソリューション市場の成長をさらに押し上げると予想されます。例えば、2021年12月にCareCloud Inc.は、ヘルスケア機関向けの次世代インターフェースとデータ管理エンジンであるCareCloud Connectorを発表しました。このソリューションは、すぐに使える統合を提供することで、データ管理と展開速度を向上させるとともに、インターフェースの制御と可視性の向上を実現しています。したがって、上記の要因から、調査対象市場は予測期間中に成長すると予想されます。しかし、このセグメントにおける熟練した専門家の不足が、予測期間中のヘルスケア相互運用性ソリューション市場の成長を抑制すると予想されます。

ヘルスケア相互運用性ソリューション市場の動向

予測期間中、サービスセグメントがヘルスケア相互運用性ソリューション市場で主要な市場シェアを占める見込み

相互運用性ソリューションのサービスプロバイダが多数存在することから、サービスセグメントが大きなシェアを占めると予測されます。さらに、ヘルスケアアプリケーションのパフォーマンスを向上させ、高速化するための全体的な運用コストを最小限に抑えるクラウドベースのプラットフォームとクラウドコンピューティングに対するヘルスケアと科学コミュニティの関心の高まりが、同セグメントの成長を促進しています。

さらに、同市場のサービスプロバイダは継続的に製品を革新しており、市場に大きな影響を与えると予想される新製品を発表しています。例えば、2021年7月、Googleクラウドは、ライフサイエンスとヘルスケア組織向けに、請求、ヘルスケア記録、研究データ、臨床検査など複数のソースからのデータを調和させるエンドツーエンドのソリューションであるヘルスケアデータエンジンを発表しました。同様に、2020年5月、NewWave TelecomはTechnologies, Inc.と協業し、ヘルスケアデータの相互運用を支援するために必要なサービスや製品をヘルスプランに提供することに特化した子会社Onyx Technologyを立ち上げました。したがって、このセグメントは予測期間中に成長すると予想されます。

さらに、ソフトウェアのアップグレード、トレーニング、メンテナンスを含むサービスの頻繁な購入、他の相互運用性ソリューションの採用が、調査対象セグメントの成長をさらに押し上げると予想されます。例えば、2021年4月、Reliq Health Technologies Inc.は、大規模企業の要件を満たすためにiUGO CareプラットフォームにFHIR(Fast Healthcare Interoperability Resources)標準を採用しました。したがって、上記の要因により、サービスセグメントは予測期間中、ヘルスケア相互運用性ソリューション市場で大きなシェアを占めると予想されます。

予測期間中、北米が市場で大きなシェアを占める見込み

北米地域は、ヘルスケアインフラのデジタル化への投資の増加、ヘルスケア費の増加、新製品の発売などにより、調査対象市場で大きなシェアを占めると予想されます。例えば、Canadian Institute for Health Informationの2021年11月のレポートによると、カナダのヘルスケアインフラは2019年の2,670億米ドルから2021年には3,080億米ドルに増加しました。同様に、米国のヘルスケア支出は2019年の3兆8,000億米ドルから2021年には4兆3,000億米ドルに増加しています。したがって、増加するヘルスケア費を抑制するために、ヘルスケア相互運用性ソリューションの需要が増加し、市場の成長を後押しすると予想されます。

さらに、北米地域では、米国は、電子カルテ(EHR)のようなデジタルヘルスケアソリューションがほぼすべての病院で広く使用されている主要国の1つであるため、ヘルスケア相互運用性ソリューションの地域の主要市場になると予想されています。例えば、2020年12月に発表された「米国と米国以外のヘルスケアシステム間での電子カルテ利用の評価」と題された調査研究によると、他国の同業者と比較した場合、米国の臨床医は非常に多くの臨床業務にEHRを積極的に利用しており、それゆえにヘルスケア相互運用性ソリューションの採用が進んでいます。

これに加えて、同国における主要市場参入企業の存在や、製品発売、M&A、提携などの事業拡大イニシアチブが、市場成長をさらに押し上げると予想されます。例えば、エンブラテルは2022年4月、臨床接続、情報統合、ヘルスケア記録の共有といった課題を解決し、ヘルスケアを統合的に把握しようとする公的機関や民間機関に適したEmbratel Saude Interoperabilidadeソリューションを発表しました。したがって、上記の要因から、北米地域が大きなシェアを占めると予想され、予測期間中、米国がヘルスケア相互運用性ソリューション市場の主要市場となると考えられます。

ヘルスケア相互運用性ソリューション産業概要

ヘルスケア相互運用性ソリューション市場は現在、大企業から中小企業まで複数の企業が存在する断片的な市場であり、そのため市場競争は緩やかです。現在市場を独占している企業には、Koninklijke Philips NV、Allscripts Healthcare LLC、Cerner Corporation、EPIC Systems Corporation、NextGen Healthcare Inc.、Infor Inc.、Jitterbit、Virtusa Corp.、Orion Health Group Limited、IBMなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- ITヘルスケアソリューションとヘルスケア相互運用性への投資の増加

- ヘルスケアコストの増加に対する懸念の高まり

- 市場抑制要因

- 熟練したヘルスケアIT専門家の不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 展開別

- クラウドベース

- オンプレミス

- レベル別

- 基礎

- 構造的

- セマンティック

- タイプ別

- ソリューション

- EHR相互運用性

- HIE相互運用性

- その他

- サービス別

- ソリューション

- エンドユーザー別

- ヘルスケアプロバイダ

- ヘルスケア支払者

- 薬局

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Koninklijke Philips NV

- Allscripts Healthcare LLC

- Oracle Corporation(Cerner Corporation)

- EPIC Systems Corporation

- NextGen Healthcare Inc.

- Koch Software Investments(Infor Inc.)

- Jitterbit

- Virtusa Corpopration

- Orion Health Group Limited

- International Business Machines Corporation(IBM)

第7章 市場機会と今後の動向

目次

The Global Healthcare Interoperability Solutions Market size is estimated at USD 5.04 billion in 2025, and is expected to reach USD 8.62 billion by 2030, at a CAGR of 11.31% during the forecast period (2025-2030).

The COVID-19 pandemic had a significant impact on the world economy and healthcare infrastructure due to the sudden surge in COVID-19 patients. It significantly increased the demand for healthcare interoperability solutions because of the unforeseen influx of COVID-19 patients with different health conditions which disrupted the general functioning of any healthcare providing facility. For instance, according to an article published in February 2021, titled 'COVID-19 Highlights Need for Laboratory Data Sharing and Interoperability', the necessity for an interoperable healthcare system has become abundantly clear as a result of the SARS-CoV-2 pandemic, and in the United States, each state has its requirements for responding to the COVID-19, figures are inconsistent and depend on the location and information source. Further, as per the same source, the country's response to COVID-19 would be significantly improved by an interoperable healthcare system. For instance, a patient could contact their provider with symptoms, and the provider would have rapid access to the patient's complete medical information to treat any underlying issues. Hence it is anticipated that the COVID-19 pandemic is expected to have a significant impact on the healthcare interoperability solutions market.

The major factors that are expected to fuel growth in the healthcare interoperability solutions market include increasing adoption and investment in digital healthcare solutions by healthcare providers across the world and rising concerns over increasing healthcare costs. The healthcare interoperability solutions can help in reducing the increasing healthcare costs due to which they are expected to be adopted more widely over the forecast period and the market is expected to grow. For example, some of the major benefits of adopting healthcare interoperability solutions are an increase in healthcare efficiency, improvement in quality of care and patient experience, reduction the healthcare cost, and lightening physician burnout among other benefits. Hence, the investment in healthcare IT and interoperability solutions is expected to increase over the forecast period which is expected to fuel growth in the healthcare interoperability solutions market. For instance, in September 2020, the Office of the National Coordinator for Health Information Technology of the United States rewarded four organizations with funding of a total of USD 2.7 million under the Leading Edge Acceleration Projects in Health Information Technology program for the exploration of new opportunities for the adoption and use of health IT standards across the healthcare ecosystem.

Further, the increasing healthcare expenditure across the world is one of the major concerns for the governments, and to reduce that healthcare IT solutions are being adopted and deployed which is further expected to increase the adoption of healthcare interoperability solutions as they will play a crucial role in transferring of data from one place to another. For instance, according to the June 2022 report of the Federal Statistical Office (Destatis) of Germany, the country's healthcare expenditure is increasing year over year and in 2020 it stood at EUR 441 billion.

Moreover, the launch of new products in the area by the market players is further expected to boost the growth of the healthcare interoperability solutions market. For instance, in December 2021, CareCloud Inc. launched CareCloud Connector, a next-generation interface and data management engine for healthcare organizations. The solution offers ready-to-use integration that enhances data management and deployment speed while delivering improved interface control and visibility. Therefore, owing to the above-mentioned factors, the studied market is expected to grow over the forecast period. However, a shortage of skilled professionals in the area is expected to restrain the growth of the healthcare interoperability solutions market during the forecast period.

Healthcare Interoperability Solutions Market Trends

Service Segment is Expected to Hold a Major Market Share in the Healthcare Interoperability Solutions Market Over the Forecast Period

The service segment is anticipated to account for the major share owing to the presence of a substantial number of service providers for interoperability solutions. Furthermore, increasing interest of healthcare and scientific communities in the cloud-based platform and cloud computing to minimize the overall operational costs for better and faster performance of healthcare applications is driving the segment growth.

In addition, the service providers in the market are continuously innovating their products and launching new products which are expected to have a significant impact on the market. For instance, in July 2021, Google Cloud introduced a healthcare data engine, an end-to-end solution for life science and healthcare organizations that harmonizes data from multiple sources, including claims, medical records, research data, and clinical trials. Similarly, in May 2020, NewWave Telecom collaborated with Technologies, Inc. for the launch of Onyx Technology, a subsidiary focused on delivering health plans with services and products required to assist healthcare data interoperability. Hence, the segment is expected to grow over the forecast period.

Moreover, the frequent purchases of services, including software upgradation, training, and maintenance, and adoption of other interoperability solutions are further expected to boost growth in the studied segment. For instance, in April 2021, Reliq Health Technologies Inc. adopted the FHIR (Fast Healthcare Interoperability Resources) standard for its iUGO Care platform to fulfill the requirements of the large-scale enterprise. Therefore, due to the above-mentioned factors, the service segment is expected to hold a significant share in the healthcare interoperability solutions market during the forecast period.

North America is Expected to Occupy a Significant Share in the Market Over the Forecast Period

The North American region is expected to hold a significant share in the studied market owing to the increasing investment in the digitalization of the healthcare infrastructure, increase healthcare expenditure, and launch of new products. For instance, according to the November 2021 report of the Canadian Institute for Health Information, the Canadian healthcare infrastructure increased from USD 267 billion in 2019 to USD 308 billion in 2021. Similarly, the healthcare expenditure of the United States increased from USD 3.8 trillion in 2019 to 4.3 trillion in 2021. Hence, to control the increasing healthcare cost, the demand for healthcare interoperability solutions is expected to increase which is expected to boost the market's growth.

Moreover, in the North American region, the United States is expected to be a major market in the region for healthcare interoperability solutions as it is one of the major countries where digital healthcare solutions like electronic health records (EHRs) are used widely in almost every hospital. For instance, according to the research study published in December 2020, titled 'Assessment of Electronic Health Record Use Between the US and Non-US Health Systems', when compared to their peers from other countries, clinicians from the United States used the EHR actively for a great deal more clinical tasks and hence, the adoption of healthcare interoperability solutions.

In addition to this, the presence of some key market players in the country and business expansion initiatives like product launches, mergers and acquisitions, and collaborations among others are expected to further boost the market growth. For instance, in April 2022, Embratel launched the Embratel Saude Interoperabilidade solution, suitable for public and private institutions that seek to solve the challenges of clinical connectivity, information integration, and sharing of medical records for an integral view of healthcare. Therefore, due to the above-mentioned factors, the North American region is expected to occupy a significant share, where the United States would be the major market for the healthcare interoperability solutions market over the forecast period.

Healthcare Interoperability Solutions Industry Overview

The healthcare interoperability solutions market is currently fragmented in nature with the presence of several large to small and medium-sized players due to which, the market is moderately competitive. Some of the companies currently dominating the market are Koninklijke Philips NV, Allscripts Healthcare LLC, Cerner Corporation, EPIC Systems Corporation, NextGen Healthcare Inc., Infor Inc., Jitterbit, Virtusa Corp., Orion Health Group Limited, and IBM.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Investment in IT Healthcare Solutions and Healthcare Interoperability

- 4.2.2 Rising Concerns Over Increasing Healthcare Costs

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Healthcare IT Professionals

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - in USD Million)

- 5.1 By Deployment

- 5.1.1 Cloud-based

- 5.1.2 On-premise

- 5.2 By Level

- 5.2.1 Foundational

- 5.2.2 Structural

- 5.2.3 Semantic

- 5.3 By Type

- 5.3.1 Solutions

- 5.3.1.1 EHR Interoperability

- 5.3.1.2 HIE Interoperability

- 5.3.1.3 Other Types

- 5.3.2 Services

- 5.3.1 Solutions

- 5.4 By End User

- 5.4.1 Healthcare Providers

- 5.4.2 Healthcare Payers

- 5.4.3 Pharmacies

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Koninklijke Philips NV

- 6.1.2 Allscripts Healthcare LLC

- 6.1.3 Oracle Corporation (Cerner Corporation)

- 6.1.4 EPIC Systems Corporation

- 6.1.5 NextGen Healthcare Inc.

- 6.1.6 Koch Software Investments (Infor Inc.)

- 6.1.7 Jitterbit

- 6.1.8 Virtusa Corpopration

- 6.1.9 Orion Health Group Limited

- 6.1.10 International Business Machines Corporation (IBM)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日