|

市場調査レポート

商品コード

1690904

アジア太平洋地域の建築サービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia Pacific Architectural Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の建築サービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

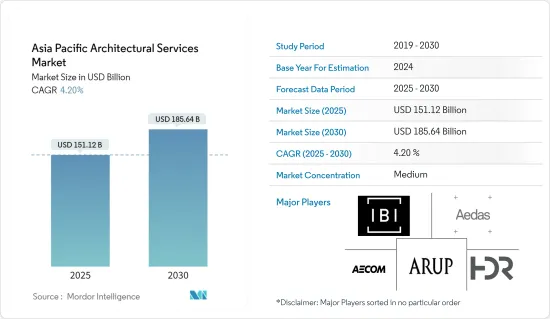

アジア太平洋地域の建築サービス市場規模は2025年に1,511億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.2%で、2030年には1,856億4,000万米ドルに達すると予測されます。

急速な都市化、スマートホームの需要増加、世界の商業・工業ビルインフラのアップグレード活動の活発化などが、市場成長を促進する大きな要因となっています。

主なハイライト

- 建築計画は、コンピューターソフトウェアの登場により、ここ数年でパラダイムシフトが起きています。デジタル設計ツール、コンピューター制御による製作、コンピューター制御による接続、相互接続の進歩は、設計・建築プロセスの新たな段階を可能にしました。

- アーキテクチャ・サービスは、フィージビリティ・スタディ、建築プログラミング、設計の助けを借りたプロジェクト管理、施工書類の作成、施工管理など、多種多様なプロセスで構成されています。持続可能な建設は本質的な利益とビジネスチャンスをもたらすため、環境に配慮した建物に対する需要の高まりが建築サービス市場を牽引しています。さらに、入居率とともに投資収益率も向上するため、運営コストも節約できます。

- アジア太平洋地域は、シンガポール、中国、日本、インドで進行中または今後予定されている大規模なインフラプロジェクト、特にスマートシティプロジェクトによって特徴付けられ、建築サービスの需要を生み出す可能性があります。インド・ブランド・エクイティ財団(IBEF)によると、インドの不動産セクターは2030年までに1兆米ドルに達し、2025年までに国内総生産(GDP)の13%以上を占めると予想されています。

- テクノロジーの導入という観点から、住宅は自動化を採用し、スマートホームへと変貌を遂げつつあります。新しいビルは、自動化を最優先事項として設計されています。自動化されたシステムは、セキュリティー、温度調節、照明などの機能を補助し、請求書を管理し、環境や周囲にプラスの影響を与えます。

- さらに、アジア太平洋地域の建築業界は著しく成長しており、革新的な設計やソフトウェアを携えて市場に参入する新しい建築事務所が増加しているため、都市計画の強化など、より優れたサービスを提供しています。こうした進歩により、3Dモデルやハイエンドの設計ソフトウェアを含む、アップグレードされた設計技術への需要が高まると予想されます。新規参入企業は、ベンチャーキャピタルからの複数の投資によって支えられており、これが調査対象市場の成長を支えています。

- しかし、先進地域と比較して認知度が低いこと、コストが高いこと、設計・施工の専門知識を有する有資格者が不足していることが、アジア太平洋地域の市場成長を妨げる最も大きな要因となっています。

- COVID-19の大流行は、建築サービスを提供する企業、特に初期段階に悪影響を及ぼしました。さまざまな国で広範な封鎖措置がとられたため、建設活動が大幅に減少し、建築サービスの需要が鈍化しました。しかし、この地域では予防接種が広く行われたため、状況が改善し、平常に近づくにつれて、市場は勢いを取り戻しました。予測期間中も同様のパターンが続くと予想されます。

アジア太平洋地域の建築サービス市場の動向

住宅部門が大きな市場シェアを占める

- 住宅部門は、建築サービスの最大エンドユーザーセグメントのひとつです。住宅プロジェクトの利害関係者は、異なるニーズに対応するため、さまざまな形態の建築ビジュアライゼーションを利用しています。これらの建築サービスは、住宅建設プロジェクトを成功させるために、住宅セクターにおいてインテリアデザインを含む様々な支援を提供しています。事業会社は信頼できるパートナー、サプライヤー、サービス・プロバイダーと協力し、利用者がプロジェクトの目標を達成できるよう支援します。

- 急速な都市化がアジア太平洋地域の住宅建築サービス市場を大きく押し上げます。アジア太平洋地域では、東アジア太平洋地域の都市化率がかなり高く、人口の約61%が都市部に滞在しています。南アジアでは、この数字はわずか35%です。(出典:世界銀行)。しかし、この割合は産業部門の成長とともに増加し、住宅需要、ひいては調査対象市場に大きく貢献すると予想されます。

- さらに、都市人口の増加により、政府は十分な居住スペースを確保するためにいくつかのイニシアチブを取っています。例えば、インド政府は最近、出稼ぎ労働者に手頃な賃貸住宅を提供するため、手頃な賃貸住宅制度(AHRC)を導入しました。これは、マハラシュトラ州首相による新たな農村住宅プロジェクト「マハ・アワス・ヨジャナ」の導入と相まって、インドの住宅建設セクターを前進させると予測されています。

- 同様に、マレーシアの2021年度予算では、政府は住宅取得を増やすためのいくつかのインセンティブを提案しました。例えば、マレーシア政府は、国内で初めて不動産を購入する場合、2025年まで印紙税の支払いを免除すると宣言しました。同国で住宅購入を希望するマレーシア人の何人かは、印紙税免除の恩恵を受けることになります。

- 2022年11月、タイの政府住宅銀行(GHB)は、低所得者に住宅を提供することを目的とした「100万戸」プロジェクトの第3期について、内閣と財務省に承認を求めました。このような取り組みにより、住宅分野での建築サービスに多くの機会が生まれることが期待されます。

大きな市場シェアを占める中国

- 中国の都市化率はアジア太平洋地域で最も高いです。中国国家統計局(NBS)によると、中国の都市化率は2018年の61.5%から2021年には64.72%に上昇しました。同国は2025年までに都市化率を65%以上に引き上げる計画です。

- 急速な工業化は、産業界で多くの労働力が必要とされることから、同国の都市人口数を増加させる重要な要因のひとつとなっています。都市化の成長を支えるため、政府は新しい住宅や商業スペースに投資し、住民の住居を確保するなど、いくつかのイニシアチブをとっています。

- 例えば、米国建築家協会(AIA)の上海報告書のデータによると、2025年までに中国は1990年代以降、ニューヨーク規模の都市10個分を建設することになります。さらに、中国国家経済部(NBS)によると、2021年には中国の不動産開発業者によって約1,369万戸のマンションが販売されました。

- 中国は依然として建築の実験場であり、建築サービスを提供する複数の企業を惹きつけています。しかし、過去の中国建設業界の開発では、建築設計は設計図面を提出した後、その後の建築建設プロセスに深く関与するのみで、建築設計と建築建設の間の分断状態を示しており、これは一連の欠点をもたらしました。伝統的な生産モデルの欠点は、総合エンジニアリング請負や全工程エンジニアリングコンサルティングといった新しいビジネスモデルの開発を促進し、研究市場の成長を支えています。

- さらに、中国では過去数年間、エネルギー・環境設計リーダーシップ(LEED)グリーンビルディングの急速な発展が記録されており、一流都市が最も積極的なプレーヤーであり続けています。米国グリーンビルディング協会のデータによると、2021年4月現在、中国では3億3,000万平方メートルを超える6,600件近くのプロジェクトがエネルギー・環境設計リーダーシップ(LEED)認証を取得、または取得に向けて取り組んでおり、LEED認証取得件数では米国に次ぐ第2位の市場となっています。

- 中国はまた、都市のデジタル変革に大規模な投資を行っており、すでに多くの大都市とその産業に適用されているスマートシティ・インフラを開発しています。さらに、中国の技術革新における国家主導の取り組みと官民企業の関与が、予測期間中の建築サービスの需要をさらに押し上げると予想されます。

アジア太平洋地域の建築サービス産業の概要

アジア太平洋地域の建築サービス市場は競合が緩やかであり、参入企業の増加によって競争が激化しています。同市場は、多数の地元企業と世界企業で構成されています。各プレイヤーは、地域全体で顧客基盤を拡大し、有機的・無機的成長戦略を採用することに注力しています。市場に参入している主なプレーヤーには、IBI Group Inc.、AECOM Ltd.、Aedas Architects Ltd.、HDR Architecture Inc.などがあります。

2022年12月、ザハ・ハディド・アーキテクツとアーキテクツ61は、シンガポールのジュロン湖地区に新しいサイエンス・センターの設計を発表しました。52,460平方メートルのこの複合施設は、教育プログラム、専門的な設備、インタラクティブな体験を通じて、科学、技術、工学、数学(STEM)をより身近なものにすることを目的としています。同社によると、この建物は2027年にオープンする予定。

2022年11月、シンガポール国立大学デザイン工学部(NUS CDE)傘下のアーキテクチャ学科は、新しい建築保存研究所(ArClab)を開設しました。これは、保存された建物の中にあるユニークな生きた研究室です。研究者、建築遺産専門家、大学院生が、建築環境の持続可能な開発に関する幅広い教育・研究活動を行う場として機能します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- グリーンビルディング需要の増加

- 3Dプリンティングの採用

- 市場抑制要因

- 設計における新しいスキルと知識の不足

- アジア太平洋地域における主要な建設ホットスポット

第6章 市場セグメンテーション

- エンドユーザー業界別

- 住宅

- 教育

- ヘルスケアとライフサイエンス

- 企業

- その他エンドユーザー別

- 国別

- 中国

- インド

- 日本

- シンガポール

- 香港

- その他アジア太平洋地域

第7章 競合情勢

- 企業プロファイル

- IBI Group Inc.

- Aedas Architects Ltd

- AECOM LTD.

- HDR Architecture Inc.

- M. Arthur Gensler Jr. & Associates Inc.

- HKS Inc.

- Stantec Inc.

- CallisonRTKL Inc.

- Skidmore, Owings & Merrill LLP

- DP Architects Pte. Ltd.

- B+H ARCHITECTS(SINGAPORE)Pte Ltd

- MORPHOGENESIS Realty Pvt. Ltd

- WSP Architects

- Safdie Architects LLC

- Aamer Architects

- Arup Group Limited

- Mitsubishi Jisho Sekkei

- KUME SEKKEI Co. Ltd

第8章 投資分析

第9章 市場の将来

The Asia Pacific Architectural Services Market size is estimated at USD 151.12 billion in 2025, and is expected to reach USD 185.64 billion by 2030, at a CAGR of 4.2% during the forecast period (2025-2030).

Rapid urbanization, increasing demand for smart homes, and rising commercial and industrial building infrastructural upgradation activities across the globe are among the significant factors driving market growth.

Key Highlights

- Architectural planning witnessed a paradigm shift in the last few years due to computer software's emergence. Advancements in digital design tools, computer-controlled fabrication, computer-controlled connectedness, and interconnectedness have enabled a new phase of the designing and building processes.

- Architectural services comprise a wide variety of processes, including feasibility studies, architectural programming, project management with the help of design, preparation of construction documents, and construction administration. The increasing demand for green buildings drives the architectural services market, as sustainable construction provides essential benefits and business opportunities. Moreover, the return on investment can be improved, along with the occupancy, thereby saving operating costs.

- The Asia Pacific region is characterized by significant ongoing and upcoming infrastructural projects, particularly smart city projects, across Singapore, China, Japan, and India, which may create a demand for architectural services. According to the India Brand Equity Foundation (IBEF), the real estate sector in India is expected to reach a value of USD 1 trillion by 2030, which may account for over 13% of the country's GDP by 2025.

- In the context of technology insertion, homes are adopting automation and transforming it into smart homes. New buildings are designed by keeping automation as the top priority. Automated systems aid in functions like security, temperature control, and lighting, which help control bills and positively impact the environment and the surroundings.

- Furthermore, the architectural industry in the Asia Pacific region is growing considerably, with an increasing number of new architectural firms entering the market with innovative designs and software, thereby providing better services, such as enhancements in urban planning. These advancements are expected to increase the demand for upgraded design technology involving 3D models and high-end designing software. The entry of new players is backed by several investments from venture capital firms, which supports the growth of the studied market.

- However, low awareness compared to the developed regions, along with higher costs involved and a shortage of qualified individuals with design and execution expertise, are among the most significant impediments to the growth of the studied market in the Asia Pacific region.

- The COVID-19 pandemic negatively impacted firms offering architectural services, especially during the initial phase. The widespread lockdown imposed across various countries significantly reduced construction activities, bringing a slowdown in demand for architectural services. However, the market regained momentum as the condition improved and moved towards normalcy due to the widespread vaccination in the region. It is expected to follow a similar pattern during the forecast period.

Asia Pacific Architectural Services Market Trends

Residential Sector to Hold Significant Market Share

- The residential sector is among the largest end-user segments for architectural services. The residential project stakeholders use different forms of architectural visualization to serve distinct needs. These architectural services provide various help, including interior design, in the residential sector to ensure a successful residential construction project. The operating firms work with trusted partners, suppliers, and service providers to help users achieve their project goals.

- Rapid urbanization significantly boosts the Asia-Pacific region's residential architectural services market. In the Asia Pacific region, the urbanization rate is considerably higher in the East Asia and Pacific region, as about 61% of the population stays in urban areas. In South Asia, this number accounts for only 35%. (Source: World Bank). However, this rate is expected to increase with the growth of the industrial sector and will contribute significantly to the demand for housing, in turn, the studied market.

- Furthermore, the growing urban population is driving the government to take several initiatives to ensure the sufficient availability of residential spaces. For instance, the Indian government recently introduced the Affordable Rental Housing Scheme (AHRC) to provide migrant workers with affordable rental housing. This, combined with the Maharashtra Chief Minister's introduction of the Maha Awas Yojana, a new rural housing project, is projected to propel India's residential construction sector forward.

- Similarly, in Malaysia's 2021 budget, the government proposed several incentives to increase homeownership. For example, the Malaysian government declared that first-time property buyers in the country will be exempt from paying stamp duty until 2025. Several Malaysians who want to buy a home in the nation will profit from the stamp duty exemption.

- In November 2022, Thailand's Government Housing Bank (GHB) sought approval from the cabinet and Finance Ministry for the third phase of the "One Million Home" project, which aims to provide housing to low income-earners. Initiatives such as these are expected to create many opportunities for architectural services in the residential arena.

China to Hold Significant Market Share

- China's urbanization rate is among the highest in the Asia-Pacific region. According to the National Bureau of Statistics (NBS) of China, the degree of urbanization in China has increased from 61.5% in 2018 to 64.72% in 2021. The country plans to take the urbanization rate beyond 65% by 2025.

- Rapid industrialization is among the significant factors driving the country's urban population count, as many workforces are required in industries. To support the urbanization growth, the government is taking several initiatives, such as investing in new residential and commercial spaces to ensure accommodation for inhabitants.

- For instance, according to the data from the American Institute of Architects (AIA) Shanghai reports, by 2025, China will have constructed the equivalent of 10 New York-sized cities since the 1990s. Furthermore, according to the NBS of China, in 2021, about 13.69 million units of apartments were sold by real estate developers in China.

- China remains a site for architectural experimentation and attracts multiple companies to provide architectural services. Although, in the past development of China's construction industry, architectural design only profoundly participated in the subsequent building construction process after submitting design drawings, showing a state of fragmentation between architectural design and building construction, which has brought a series of drawbacks. The shortcomings of the traditional production model have promoted the development of new business models, such as general engineering contracting and whole-process engineering consulting, which are supporting the growth of the studied market.

- Furthermore, China has registered rapid development of Leadership in Energy and Environmental Design (LEED) green buildings over the past few years, with first-tier cities remaining the most active players. As of April 2021, nearly 6,600 projects in China totaling more than 330 million square meters either received the Leadership in Energy and Environmental Design (LEED) certification or were working toward it, making it the second-largest market after the United States in terms of LEED certification, according to data by the US Green Building Council.

- China is also massively investing in the digital transformation of its cities and has developed smart city infrastructure that has already been applied to many of its major metropolises and their industries. Furthermore, China's state-led initiatives in technological innovation and public-private enterprise involvement are further expected to drive the demand for architectural services during the forecast period.

Asia Pacific Architectural Services Industry Overview

The Asia Pacific architectural services market is moderately competitive and is growing in competition with the entry of an increased number of players. The market consists of a significant number of local and global players. The players focus on expanding their client base across the region and adopting organic and inorganic growth strategies. Some major players operating in the market include IBI Group Inc., AECOM Ltd., Aedas Architects Ltd, and HDR Architecture Inc., among others.

In December 2022, Zaha Hadid Architects and Architects 61 unveiled the design for the new Science Center in Jurong Lake District, Singapore. The 52,460 square meters complex aims to make science, technology, engineering, and mathematics (STEM) more accessible through educational programs, specialized amenities, and interactive experiences. According to the company, the building is expected to open in 2027.

In November 2022, the Department of Architecture, under the National University of Singapore College of Design and Engineering (NUS CDE), opened the new Architectural Conservation Laboratory (ArClab). It is a unique living laboratory housed in a conserved building. It will serve as a site for researchers, built heritage professionals, and graduate students to conduct a wide range of teaching and research activities on sustainable development of the built environment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Green Building

- 5.1.2 Adoption of 3D Printing

- 5.2 Market Restraints

- 5.2.1 Lack of New Skills and Knowledge in Designing

- 5.3 Key Construction Hotspots in Asia-Pacific

6 MARKET SEGMENTATION

- 6.1 By End-user Vertical

- 6.1.1 Residential

- 6.1.2 Education

- 6.1.3 Healthcare and Life Sciences

- 6.1.4 Corporate

- 6.1.5 Other End-user Verticals

- 6.2 By Country

- 6.2.1 China

- 6.2.2 India

- 6.2.3 Japan

- 6.2.4 Singapore

- 6.2.5 Hong Kong

- 6.2.6 Rest of Asia Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBI Group Inc.

- 7.1.2 Aedas Architects Ltd

- 7.1.3 AECOM LTD.

- 7.1.4 HDR Architecture Inc.

- 7.1.5 M. Arthur Gensler Jr. & Associates Inc.

- 7.1.6 HKS Inc.

- 7.1.7 Stantec Inc.

- 7.1.8 CallisonRTKL Inc.

- 7.1.9 Skidmore, Owings & Merrill LLP

- 7.1.10 DP Architects Pte. Ltd.

- 7.1.11 B+H ARCHITECTS (SINGAPORE) Pte Ltd

- 7.1.12 MORPHOGENESIS Realty Pvt. Ltd

- 7.1.13 WSP Architects

- 7.1.14 Safdie Architects LLC

- 7.1.15 Aamer Architects

- 7.1.16 Arup Group Limited

- 7.1.17 Mitsubishi Jisho Sekkei

- 7.1.18 KUME SEKKEI Co. Ltd