|

市場調査レポート

商品コード

1690899

東南アジアのWtE(廃棄物発電):市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Southeast Asia Waste-to-Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 東南アジアのWtE(廃棄物発電):市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

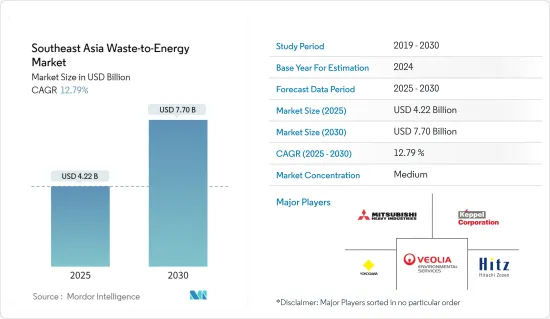

東南アジアのWtE(廃棄物発電)市場規模は2025年に42億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは12.79%で、2030年には77億米ドルに達すると予測されます。

主なハイライト

- 長期的には、廃棄物発生量の増加、持続可能な都市生活のニーズを満たすための廃棄物管理への関心の高まり、非化石燃料エネルギー源への注目の高まりが、東南アジア廃棄物エネルギー市場の需要を牽引しています。

- 逆に、資本コストが高いことが、調査期間中の市場成長の妨げになると予想されます。

- とはいえ、デンドロ・リキッド・エネルギー(DLE)のような新興のWtE(廃棄物発電)技術は、今後数年間、市場関係者に大きなビジネスチャンスをもたらすと期待されています。DLEは、発電効率が4倍高く、さらに工場敷地内での排出物や廃液の問題がないという特典もある、

- マレーシアは、東南アジア地域で最も急成長している国のひとつです。同国は廃棄物管理の改善への取り組みを強化しており、その中でWtE(廃棄物発電)は重要な役割を果たしています。

東南アジアのWtE(廃棄物発電)市場の動向

熱ベースの廃棄物エネルギー変換への需要の高まり

- 熱ベースの廃棄物エネルギー変換とは、熱エネルギーを利用して廃棄物を電気、熱、燃料などの利用可能なエネルギーに変換することです。このアプローチには、廃棄物をエネルギーに変換する触媒として熱を利用する様々な技術の応用が含まれます。

- 急速な人口増加と都市化により、廃棄物の発生量は大幅に増加し、廃棄物管理の課題となっています。熱を利用した廃棄物のエネルギー転換は、埋め立てや焼却しなければならない廃棄物の量を効果的に管理し、削減します。

- 2023年1月、オランダに本社を置くハーベスト・ウェイスト社(前身はアムステルダム・ウェイスト・エンバイロメンタル・コンサルタンシー・アンド・テクノロジー社)は、ベトナムのメコンデルタ地方ソクチャン省で、廃棄物熱エネルギー化事業の初期調査を開始しました。プロジェクトの総事業費は約1億米ドルと見積もられています。

- 信頼性が高く持続可能なエネルギー源に対するニーズが高まっています。熱ベースのWtE(廃棄物発電)技術は、廃棄物を電気や熱などの利用可能なエネルギーに変換することができます。エネルギー生成に貢献し、エネルギー・ミックスの多様化にも役立つため、化石燃料への依存度が低下します。

- 東南アジアは、世界で最も急速に都市人口が増加している地域のひとつです。都市人口の急速な増加は、この地域全体の都市人口から発生する廃棄物の量を爆発的に増加させました。この廃棄物の大半は、シンガポールを除いて有機物である(約50%以上)。

- 人口の増加に伴い、この地域の電力需要は近年大幅に増加しています。例えばタイでは、2021年から2022年にかけて電力消費量が3%以上増加しています。

- したがって、上記の点から、熱ベースのWtE(廃棄物発電)システムの需要は予測期間中に増加すると予想されます。

著しい成長が期待されるマレーシア

- マレーシア政府は、持続可能な廃棄物管理の実践と再生可能エネルギー開発を積極的に推進しています。WtE(廃棄物発電)部門を支援するために、固定価格買取制度、税制優遇措置、規制枠組みなど、さまざまな取り組みや政策を実施しています。これらの施策は、この産業への投資と成長を促す環境を作り出しています。

- 他の多くの国と同様、マレーシアも人口増加、都市化、工業化により廃棄物発生量が増加しています。そのため、効率的な廃棄物管理ソリューションが急務となっています。WtE(廃棄物発電)プロジェクトは、再生可能エネルギーを生み出しながら、増え続ける廃棄物量に取り組む持続可能な方法を提供します。

- 2023年5月、マラッカ州政府は、スンガイ・ウダン衛生固形廃棄物処分場での廃棄物エネルギー(WTE)プラントまたは焼却炉の迅速な建設を命じた。彼らは、2026年という当初の目標よりも早く、来年に施設を稼働させることを目指しています。

- さらにマレーシアでは、廃棄物からエネルギーへの転換プロセスに適した有機廃棄物がかなりの割合を占めています。食品廃棄物や農業残渣などの有機廃棄物は、嫌気性消化や堆肥化に効率的に利用でき、バイオガスや肥料の生産につながります。有機廃棄物資源が豊富なことは、WtE(廃棄物発電)プロジェクトにとって好条件です。

- さらにマレーシア政府は、国のエネルギーミックスに占める再生可能エネルギーの割合を増やすため、再生可能エネルギー目標を設定しています。WtE(廃棄物発電)技術は、廃棄物資源から再生可能エネルギーを生成することで、こうした目標の達成に貢献します。WtE(廃棄物発電)技術は、国の持続可能性目標に合致し、低炭素経済への移行を支援します。

- 国際再生可能エネルギー機関によると、2022年の再生可能エネルギー設備容量は9044MWで、2018年から2022年の間に20%以上の成長率を記録しています。

- したがって、上記の点から、マレーシアは予測期間中、市場調査において重要な役割を果たすと予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模(MW)と需要予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 廃棄物発生量の増加

- 環境への懸念と持続可能性の目標

- 抑制要因

- WtE(廃棄物発電)インフラにかかる高い資本コスト

- 促進要因

- サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 技術

- 物理的

- 熱

- 焼却

- コプロセシング

- 熱分解/ガス化

- 生物学的

- 嫌気性消化

- 地域別市場分析{2028年までの市場規模と需要予測(地域別のみ)}:マレーシア

- マレーシア

- インドネシア

- タイ

- シンガポール

- ベトナム

- その他の東南アジア地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Mitsubishi Heavy Industries Ltd

- Keppel Corporation

- PT Yokogawa Indonesia

- Veolia Environment SA

- Hitachi Zosen Corp

- MVV Energie AG

- Martin GmbH

- Babcock & Wilcox Volund AS

第7章 市場機会と今後の動向

- 国際的な提携と投資

目次

Product Code: 72358

The Southeast Asia Waste-to-Energy Market size is estimated at USD 4.22 billion in 2025, and is expected to reach USD 7.70 billion by 2030, at a CAGR of 12.79% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the increasing amount of waste generation, growing concern for waste management to meet the need for sustainable urban living, and increasing focus on non-fossil fuel sources of energy are driving the demand for the Southeast Asia Waste-to-Energy Market.

- Conversely, the high capital costs are expected to hinder market growth during the study period.

- Nevertheless, emerging waste-to-energy technologies, such as Dendro Liquid Energy (DLE), are expected to create significant opportunities for market players over the coming years. It is four times more efficient in terms of electricity generation, with the additional benefits of no emission discharge and effluence problems at plant sites,

- Malaysia is one of the fastest-growing countries in the Southeast Asian region. The country ramped up its efforts in improving waste management, in which waste-to-energy plays a key role.

Southeast Asia Waste-to-Energy Market Trends

Growing Demand for Thermal-Based Waste-to-Energy Conversion

- Thermal-based waste-to-energy conversion refers to utilizing thermal energy to convert waste materials into usable forms of energy, such as electricity, heat, or fuel. This approach involves the application of various technologies that use heat as a catalyst for converting waste into energy.

- Rapid population growth and urbanization led to a significant increase in waste generation, posing challenges for waste management. Thermal-based waste-to-energy conversion effectively manages and reduces the waste volume that must be landfilled or incinerated.

- In January 2023, Harvest Waste, a company based in the Netherlands (formerly Amsterdam Waste Environmental Consultancy and Technology), commenced initial studies for a thermal waste-to-energy venture in the Mekong Delta province of Soc Trang in Vietnam. The project is estimated to cost around USD 100 million.

- There is a growing need for reliable and sustainable energy sources. Thermal-based waste-to-energy technologies allow waste conversion into usable energy forms, such as electricity and heat. It contributes to energy generation and helps diversify the energy mix, reducing dependence on fossil fuels.

- Southeast Asia includes one of the fastest-growing urban populations globally. The rapid growth in the urban population led to explosive growth in the amount of waste generated by the urban population across the region. Most of this waste is organic (about or more than 50%) except in Singapore.

- With the growing population, the region's electricity demand increased significantly in recent years. For instance, in Thailand, electricity consumption increased by more than 3% between 2021 and 2022.

- Therefore, as per the above points, the demand for thermal-based waste-to-energy systems is expected to increase during the forecasted period.

Malaysia Expected to Witness Significant Growth

- The Malaysian government actively promoted sustainable waste management practices and renewable energy development. They implemented various initiatives and policies to support the waste-to-energy sector, including feed-in tariffs, tax incentives, and regulatory frameworks. These measures create a conducive environment for investment and growth in the industry.

- Like many other countries, Malaysia is experiencing a rise in waste generation due to population growth, urbanization, and industrialization. It creates a pressing need for efficient waste management solutions. Waste-to-energy projects offer a sustainable method to tackle the growing waste volume while generating renewable energy.

- In May 2023, the Melaka state government ordered the expedited construction of the Waste to Energy (WTE) plant or incinerator at the Sungai Udang Sanitary Solid Waste Disposal Site. They aim to include the facility operational next year, earlier than the original target of 2026.

- Furthermore, Malaysia includes a significant proportion of organic waste, which is well-suited for waste-to-energy conversion processes. Organic waste, such as food waste and agricultural residues, can be efficiently utilized for anaerobic digestion or composting, leading to biogas or fertilizer production. The abundance of organic waste resources presents favorable conditions for waste-to-energy projects.

- Additionally, the Malaysian government set renewable energy targets to increase the share of renewable energy in the country's energy mix. Waste-to-energy technologies contribute to fulfilling these targets by generating renewable energy from waste resources. It aligns with the country's sustainability goals and supports the transition to a low-carbon economy.

- According to International Renewable Energy Agency, the total renewable energy installed capacity in 2022 was 9044 MW registering a growth rate of more than 20% between 2018 and 2022.

- Therefore, according to the above points, Malaysia is expected to play a key role in the market studies during the forecasted period.

Southeast Asia Waste-to-Energy Industry Overview

The Southeast Asia waste-to-energy market is moderately consolidated. The key players in the market (in no particular order) include Mitsubishi Heavy Industries Ltd, Keppel Corporation, PT Yokogawa Indonesia, Veolia Environment SA, and Hitachi Zosen Corp, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in MW, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Waste Generation

- 4.5.1.2 Environmental Concerns and Sustainability Goals

- 4.5.2 Restraints

- 4.5.2.1 High Capital Costs Involved in Waste-to-Energy Infrastructure

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Physical

- 5.1.2 Thermal

- 5.1.2.1 Incineration

- 5.1.2.2 Co-processing

- 5.1.2.3 Pyrolysis/gasification

- 5.1.3 Biological

- 5.1.3.1 Anaerobic Digestion

- 5.2 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.2.1 Malaysia

- 5.2.2 Indonesia

- 5.2.3 Thailand

- 5.2.4 Singapore

- 5.2.5 Vietnam

- 5.2.6 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Mitsubishi Heavy Industries Ltd

- 6.3.2 Keppel Corporation

- 6.3.3 PT Yokogawa Indonesia

- 6.3.4 Veolia Environment SA

- 6.3.5 Hitachi Zosen Corp

- 6.3.6 MVV Energie AG

- 6.3.7 Martin GmbH

- 6.3.8 Babcock & Wilcox Volund AS

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 International Collaborations and Investments