|

市場調査レポート

商品コード

1690883

ゼロエミッション航空機:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Zero-emission Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ゼロエミッション航空機:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

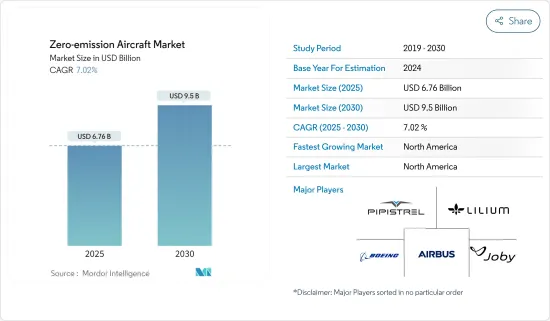

ゼロエミッション航空機市場規模は2025年に67億6,000万米ドルと推定・予測され、予測期間中(2025~2030年)のCAGRは7.02%で、2030年には95億米ドルに達すると予測されます。

COVID-19パンデミックの発生は、旅行制限により民間と一般航空市場を混乱させました。また、経済にも影響を与え、いくつかの航空宇宙企業は革新的なプロジェクトに向けた資金を一時停止する結果となりました。こうした決定は、ゼロエミッション航空機市場の成長に一時的な影響を与えました。しかし、航空機運航会社が運航コストと二酸化炭素排出量の削減を模索していることから、予測期間中に全電気航空機への投資、検査、採用が大幅に増加するものと考えられます。

排ガス規制の厳格化により、メーカーはゼロエミッションのコンセプトへとシフトしています。エンジンメーカーは、航空産業が新しいコンセプトへと移行するために重要な役割を果たすと考えられます。サステイナブル航空燃料(SAF)は、AirbusやBoeingのような企業が100%SAFでのフライトを目標としているように、産業のCO2排出量を削減するための航空ロードマップの重要な部分でもあります。

技術的課題だけでなく、航空産業の移行には、規制やインフラのエコシステムを変える必要があります。インフラや製造コストを引き下げるためには、産業を超えた協力が必要であり、これは相互に利益をもたらし、ゼロエミッション航空機の開発を加速させる一助となると考えられます。

電気航空機は一般航空市場に浸透しています。しかし、長距離商業航空への採用は、予測期間の後半に大きな開発が期待されるため、間もなく現実のものとなるにはまだ遠いです。

ゼロエミッション航空機市場の動向

進化する排出規制が開発ペースを牽引

2015年、米国環境保護庁(EPA)は、航空機に使用される特定クラスのエンジンから排出される温室効果ガスが大気汚染の一因となり、公衆衛生と福祉を危険にさらすと認定しました。2016年、ICAOは国連加盟国の旅客便と貨物便に適用される世界の排出削減スキームを最終決定しました。2020年の世界の航空排出量をベンチマークとし、2020年の排出量の約80%を2035年まで航空会社がオフセットすることが決定されました。

このような画期的な決定により、メーカーは二酸化炭素排出量を削減するサステイナブル方法に頼ろうとし、電気航空機の開発への道が開かれました。市場関係者は電気航空機技術への投資を開始し、すでに試作機の成功や軽飛行機の商業化という形で成功を収めています。

新しい技術が登場するにつれて、その商業的実現可能性を向上させるための規制が策定されつつあります。CS-23のような規制は、航空機の目的と設計に依存しない要件を再確立するものです。これにより、全電気推進とハイブリッド推進の開発におけるさまざまな機会の道が開かれました。焦点は、設計要件を満たすことから、消費者の安全性と航空機の自動化を向上させることに移りました。これによって設計者は、航空機全体をゼロから再設計し、設計上の制約から不可能であった必要な改造を行うことに集中できるようになりました。

予測期間中は北米と欧州が市場を独占する

北米と欧州は航空市場が成熟しています。主要な航空機OEMに近いため、複数の航空宇宙企業がこれらの地域に進出しています。NASA、Airbus、Boeing、ロールスロイスなどの航空宇宙大手の存在は、ゼロエミッション航空機市場の成長を支えると考えられます。現在、ゼロエミッションコンセプトに取り組んでいる企業の90%以上が米国と欧州に拠点を置いています。2020年9月、Airbusは2035年までに就航可能なゼロエミッション民間航空機の3つのコンセプトを明らかにしました。これらのコンセプトはすべて、一次動力源として水素に依存しています。Rolls-Royceは最近、今後10年間でエネルギー貯蔵システムに8,000万ポンドを投資する計画を発表しました。同社は、1回の充電で100マイル以上のゼロエミッション飛行を可能にするエネルギー貯蔵システム(ESS)を開発しています。Rolls-Royceの航空宇宙認定ESSソリューションは、アーバンエアモビリティ市場ではeVTOL(電動垂直離着陸機)、コミューター市場では最大19席の固定翼機用の電気とハイブリッド電気推進システムに電力を供給します。2020年12月初め、水素電気航空機開発会社のZeroAviaは、Amazonやシェルを含む多数の大手投資家から2,140万米ドルの支援を受け、2023年から初の業務用ゼロエミッション飛行機を運航する計画を支援するための最初の資金調達ラウンドを完了しました。同社はまた、British Airwaysと提携し、同航空の機体で使用するゼロエミッション航空機の開発を模索しています。同社はまた、航空宇宙技術ラボ(ARI)を通じて、英国政府から1,630万米ドルの資金援助を受けました。このような市場の開拓は、予測期間中、北米と欧州の市場成長を促進すると予想されます。

ゼロエミッション航空機産業概要

複数の新興企業がこの市場に参入しているため、市場は急速に細分化しています。新興企業はプロトタイプを設計しており、航空機開発の様々な段階にあります。これらの企業は、大手航空宇宙企業や投資会社からの一連の資金調達に依存しています。最近の動向では、能力、効率の拡大、開発サイクルの推進を目的とした新たな提携がいくつか見られます。例えば、Rolls-Royceは最近、航空宇宙メーカーのTecnamとスカンジナビア最大の地域航空会社Wideroeと提携し、新しいバッテリー駆動の航空機を製造しました。この提携は、Rolls-RoyceとTecnamが過去に手がけた「P-Volt」と呼ばれる全電気式航空機を基に、2026年までにノルウェーで通勤者向けの全電気式旅客機を就航させることを目的としています。このパートナーシップは、Rolls-Royceが複数の航空市場において、全電気とハイブリッド電気推進・動力システムのリーディングサプライヤーになるという野心を示しています。他にも、AirbusのシティAirbusやBoeingのeVTOLなど、いくつかの航空宇宙メーカーがバッテリー駆動の航空機を計画しています。そのほとんどは、都市間や空港から市街地へのフェリーを目的とした短距離機です。同市場における他の有力企業には、PIPISTREL d.o.o.、Bye Aerospace、Aurora Flight Sciences、Eviation、Joby Aviation、NASA、Lilium GmbH、ZeroAvia, Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- 民間と一般航空

- 軍用機

- 地域

- 北米

- 欧州

- その他

第6章 競合情勢

- 企業プロファイル

- Bye Aerospace

- Ampaire Inc.

- PIPISTREL d.o.o.

- Airbus SE

- Eviation

- ZeroAvia, Inc.

- Heart Aerospace

- Lilium GmbH

- Aurora Flight Sciences(The Boeing Company)

- Wright Electric

- Joby Aero, Inc.

- NASA

- Rolls-Royce plc

- Avinor AS

- Equator Aircraft AS

- BETA Technologies, Inc.

- Evektor, spol. s r. o.

第7章 市場機会と今後の動向

The Zero-emission Aircraft Market size is estimated at USD 6.76 billion in 2025, and is expected to reach USD 9.50 billion by 2030, at a CAGR of 7.02% during the forecast period (2025-2030).

The outbreak of the COVID-19 pandemic disrupted the commercial and general aviation market due to travel restrictions. It also had an impact on the economy and resulted in several aerospace companies to pause funds towards innovative projects. Such decisions have temporarily impacted the growth of the zero-emission aircraft market. However, as aircraft operators looking to reduce their operational costs and carbon emission, there will be significant growth in investment, testing, and adoption of all-electric aircraft during the forecast period.

Increasing stringency on the emission regulations has made manufacturers shift towards zero-emission concept. Engine manufacturers will play a vital role for the aviation industry to move towards the new concept. Sustainable aviation fuel (SAF) is also an important part of the aviation roadmap to reduce the industry's CO2 emissions as companies like Airbus and Boeing are targeting flights on 100% SAF.

Beyond technology challenges, the aviation industry's transition will require the regulatory and infrastructure ecosystems to change. Cross-industry collaboration will be required to drive down infrastructure and production costs, which will be mutually beneficial and help speed up development of the zero-emission aircraft.

Electric aircraft has penetrated the general aviation market. However, its adoption in long-haul commercial aviation is still far away from becoming reality soon with major developments expected in the later half of the forecast period.

Zero-Emission Aircraft Market Trends

Evolving Emissions Regulations Driving the Pace of Development

In 2015, the US Environmental Protection Agency (EPA) found that the greenhouse gas emissions from certain classes of engines used in aircraft contribute to air pollution and endanger public health and welfare. In 2016, the ICAO finalized a global emissions-reduction scheme applicable to passenger and cargo flights in the member countries of the UN. It was decided that the global aviation emission in 2020 will be used as a benchmark, and around 80% of the emission levels in 2020 will be offset by the airlines until 2035.

Such a landmark decision paved the way for the development of electric aircraft as manufacturers sought to resort to sustainable ways of reducing carbon footprint. The market players started investing in electric aircraft technologies and have already been successful in the form of successful prototypes and commercialization of light aircraft.

With new technology coming into the foray, regulations are being framed to improve their commercial feasibility. Regulations, such as CS-23, reestablish the objectives and design independent requirements of an aircraft. This has opened various avenues of opportunities in the development of all-electric and hybrid propulsion. The focus has shifted from fulfilling design requirements to improving consumer safety and automation in aircraft. This has enabled the designers to focus on redesigning the total aircraft from scratch and make necessary modifications that were otherwise impossible due to design restrictions.

North America and Europe will Dominate the Market During the Forecast Period

North America and Europe have a matured aviation market. Several aerospace companies are in these regions due to their proximity to major aircraft OEMs. The presence of aerospace giants like NASA, Airbus, Boeing, and Rolls Royce among others will support the growth of the zero-emission aircraft market. Over 90% of the companies currently working on the zero-emission concept are based in the US and Europe. In September 2020, Airbus revealed three concepts for zero-emission commercial aircraft which could enter service by 2035. All of these concepts rely on hydrogen as a primary power source. Rolls-Royce recently announced its plan to invest £80 million in energy storage systems over the next decade. The company is developing energy storage systems (ESS) that will enable aircraft to undertake zero-emission flights of over 100 miles on a single charge. Aerospace-certified ESS solutions from Rolls-Royce will power electric and hybrid-electric propulsion systems for eVTOLs (electric vertical takeoff and landing) in the urban air mobility market and fixed-wing aircraft, with up to 19 seats, in the commuter market. Earlier in December 2020, Hydrogen-electric aircraft developer ZeroAvia secured USD 21.4 million of backing from a raft of major investors, including Amazon and Shell, as the company completed its first fundraising round in support of plans to run its first commercial zero emission planes from 2023. The company has also partnered with British Airways to explore the development of zero emission aircraft for use in the airline's fleet. It also received approval of USD 16.3 million of U.K. government funding via the Aerospace Technology Institute (ARI). Such developments are anticipated to drive the market growth in the North America and Europe region during the forecast period.

Zero-Emission Aircraft Industry Overview

The market is rapidly becoming fragmented as several new companies are venturing into this market. Start-ups are designing prototypes and are at various stages of aircraft development. These companies are dependent on series funding from major aerospace companies and investment firms. Several new collaborations have been observed in the recent past as companies look to expand capabilities, efficiency, and propel the development cycle. For instance, Rolls Royce has recently partnered with aerospace manufacturer Tecnam and Scandinavia's largest regional airline, Wideroe, to produce a new battery-powered aircraft. The partners aim to launch an all-electric passenger aircraft for commuters in Norway by 2026, building on previous work by Rolls Royce and Tecnam on an all-electric aircraft called the P-Volt. This partnership demonstrates Rolls-Royce's ambitions to be the leading supplier of all-electric and hybrid-electric propulsion and power systems across multiple aviation markets. Several other aerospace manufacturers have plans for battery-powered aircraft, including Airbus with the CityAirbus and Boeing's eVTOL. Most are short-range aircraft designed to ferry people between cities or from airports to city centers. Some of the other prominent players in the market are PIPISTREL d.o.o., Bye Aerospace, Aurora Flight Sciences, Eviation, Joby Aviation, NASA, Lilium GmbH, and ZeroAvia, Inc. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 Application

- 5.1.1 Commercial and General Aviation

- 5.1.2 Military Aviation

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Bye Aerospace

- 6.1.2 Ampaire Inc.

- 6.1.3 PIPISTREL d.o.o.

- 6.1.4 Airbus SE

- 6.1.5 Eviation

- 6.1.6 ZeroAvia, Inc.

- 6.1.7 Heart Aerospace

- 6.1.8 Lilium GmbH

- 6.1.9 Aurora Flight Sciences (The Boeing Company)

- 6.1.10 Wright Electric

- 6.1.11 Joby Aero, Inc.

- 6.1.12 NASA

- 6.1.13 Rolls-Royce plc

- 6.1.14 Avinor AS

- 6.1.15 Equator Aircraft AS

- 6.1.16 BETA Technologies, Inc.

- 6.1.17 Evektor, spol. s r. o.