中東のミリタリービークル(軍用移動手段):市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Middle East Military Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690846

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

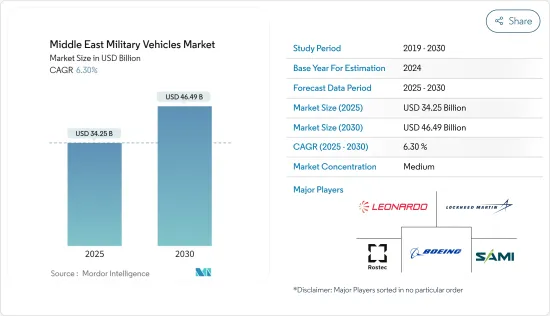

中東のミリタリービークル(軍用移動手段)の市場規模は2025年に342億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.3%で、2030年には464億9,000万米ドルに達すると予測されます。

サウジアラビア、イスラエル、アラブ首長国連邦などの国々が近代的なミリタリービークルを運用する一方で、この地域のいくつかの国々は近代化を必要とするソ連時代の車両を保有しています。そのため、これらの国々は新しいミリタリービークルの調達に投資しています。

加えて、ミリタリービークル(軍用移動手段)の老朽化により、あと何年か有効に機能させるのであれば、車両の効率性、殺傷能力、洗練性を向上させるためのアップグレードプログラムへの投資を余儀なくされている国もあります。

新興諸国のミリタリービークルの近代化と拡大が健全なペースで進む一方で、この地域は、自国生産能力を開発することで、自給自足と外国からの独立を強めています。いくつかの国々は、独自にミリタリービークルを開発しているか、あるいは外国のパートナーと提携し、技術移転協定の助けを借りて現地で車両を製造しています。

しかし、原油価格の変動などの要因が中東のいくつかの国の経済に影響を及ぼしており、ひいては軍事費の伸びにも影響を及ぼしています。

中東のミリタリービークル(軍用移動手段)市場の動向

装甲車セグメントは予測期間中に最も高い成長を遂げる

過去数年間、イエメン、リビア、ソマリアでの紛争やシナイ半島の反乱により、中東地域の軍備調達は急ピッチで増加しました。

UAEは、能力開発を継続するため、UAE軍の全部隊を新鋭の軍事装備で近代化する計画です。例えば、2023年2月、フランスの主要陸上防衛企業であるネクスターは、UAE軍の主要サプライヤーであるインターナショナル・ゴールデン・グループと、UAE軍のルクレール主力戦車(MBT)の近代化に向けた提携契約を締結しました。

UAEはまた、兵力保護の強化、人道支援活動の実施、重要インフラの保護にMRAP車両を活用する意向です。2023年2月、ラブダン8x8歩兵戦闘車(IFV)400両の最初のバッチがUAE陸軍に納入され、製造元のオトカー社は、今後の追加発注に期待を寄せています。

イランには、一連の改造を施すことで火力支援などの任務を遂行するための装備が可能な装輪装甲車や砂装甲車が非常に多く存在します。たとえば、BTR50、60シリーズやBMP1、2兵員輸送車などがその一例です。このような装甲車の保有数を急速に増やすという中東諸国の政府の強固な計画は、今後数年間のミリタリービークル市場の成長を促進すると予想されます。

予測期間中、トルコが市場シェアを独占

トルコは、防衛産業への投資と生産拡大に力を入れています。最近の国内設計と生産への注力は、ロシアや様々な過激派組織からの潜在的脅威の増加や、NATO同盟国によるトルコの防衛産業への制裁に起因しています。こうした状況の中、2023年5月、トルコのFNSSディフェンス・システムズは、トルコ陸軍のACV-15新型装甲兵員輸送車(AAPC)の能力強化を提供する契約を結びました。この契約は、車両の性能を向上させ、耐用年数をさらに20年延長するために締結されました。同社によると、未公表の数のAAPCに最新のサブシステムが搭載され、より多くの任務をサポートし、戦場での高度な脅威への対処を支援します。

トルコの調達・防衛当局は、既存のF-16ブロック30戦闘機の構造寿命を8,000飛行時間から12,000飛行時間に延ばすことを目的としたプログラムを開始しました。このアップグレードは、1機あたり1,200から1,500の部品に及ぶ可能性があります。

さらに、トルコは装甲車製造において大きく前進しており、艦隊を近代化するために新しい車両を取得しており、市場の成長にさらに貢献するために海軍艦隊のアップグレードに関心を持っています。例えば2023年4月、トルコ海軍はトルコ初の上陸用プラットフォーム・ドックである水陸両用強襲揚陸艦TCG Anadoluを受領しました。同軍は同艦から重ヘリコプター、無人機、軽攻撃機を配備する予定です。

中東のミリタリービークル(軍用移動手段)産業の概要

中東のミリタリービークル市場は半固定的であり、複数の国内外のプレーヤーがより大きな市場シェアを争っています

ミリタリービークルの国産化に注目が集まっていることから、予測期間中に地元企業の市場シェアが高まると予想されます。トルコ、サウジアラビア、アラブ首長国連邦のような国々が、国産化のフロントランナーです。例えば、サウジアラビアは、サウジアラビア政府のビジョン2030に沿って、軍備や兵器の輸出依存度を減らすために、防衛兵器や弾薬の製造能力を強化することに注力しています。同政府は、2030年までに国内の軍事装備支出を50%まで増やす計画です。サウジアラビア軍需産業(SAMI)、BMC Otomotiv Sanayi ve Ticaret AS、Denel SOC Ltdが著名な現地メーカーです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 米ドルの通貨換算レート

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 軍用機

- 戦闘機

- 戦闘機

- 戦闘ヘリコプター

- 非戦闘機

- 偵察・監視機

- 練習機

- 輸送機

- その他の非戦闘機

- 戦闘機

- 艦艇

- 駆逐艦

- フリゲート

- コルベット

- 潜水艦

- その他の艦艇

- 装甲車両

- 装甲兵員輸送車

- 歩兵戦闘車

- 地雷対応待ち伏せ防御車

- 主力戦車

- その他の装甲車

- 地域

- サウジアラビア

- アラブ首長国連邦

- カタール

- トルコ

- イスラエル

- その他中東地域

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Rostec

- Lockheed Martin Corporation

- The Boeing Company

- Abu Dhabi Ship Building Co.

- IAI

- BMC Otomotiv Sanayi ve Ticaret A.S.

- Fincantieri S.p.A.

- Saudi Arabian Military Industries(SAMI)

- Dassault Aviation SA

- Naval Group

- Denel SOC Ltd.

- BAE Systems plc

- Oshkosh Corporation

- Airbus SE

- Leonardo S.p.A.

- Patria Group

- FNSS Savunma Sistemleri A.S.

第7章 市場機会と今後の動向

目次

The Middle East Military Vehicles Market size is estimated at USD 34.25 billion in 2025, and is expected to reach USD 46.49 billion by 2030, at a CAGR of 6.3% during the forecast period (2025-2030).

While countries like Saudi Arabia, Israel, and the United Arab Emirates operate modern military vehicles, several countries in the region possess Soviet-era vehicles that require modernization. Hence, these countries are investing in the procurement of new military vehicles.

In addition, the aging fleet of military vehicles is also forcing some countries to invest in upgrade programs to improve the efficiency, lethality, and sophistication of the vehicles if they are slated to be effectively functional for some more years.

While the modernization and expansion of the region's vehicle fleets continue at a healthy pace, the region is also becoming increasingly self-sufficient and independent of foreign countries by developing indigenous manufacturing capabilities. Several countries have been developing military vehicles on their own or are partnering with their foreign counterparts and manufacturing vehicles locally with the help of technology transfer agreements.

However, factors like fluctuations in oil prices are affecting the economies of several countries in Middle East, in turn affecting growth in military spending.

Middle East Military Vehicles Market Trends

Armored Vehicles Segment to Witness Highest Growth During the Forecast Period

Over the past few years, the military equipment procurement of the region increased at a rapid pace, due to the conflicts in Yemen, Libya, and Somalia and the Sinai insurgency.

UAE plans to modernize all units of the UAE armed forces with new and advanced military equipment to continue developing capabilities. For instance, in February 2023, Nexter, the leading French land defense company, signed a teaming agreement with International Golden Group, the leading supplier of the UAE Armed forces, to prepare for the modernisation of the UAE Army's Leclerc main battle tank (MBT).

The UAE also intends to utilize the MRAP vehicles to increase force protection, conduct humanitarian assistance operations, and protect critical infrastructure. In February 2023, the first batch of 400 Rabdan 8x8 infantry fighting vehicles (IFVs) was delivered to the UAE Army and manufacturer Otokar is hopeful that additional orders will be placed in the future.

Iran has a very large fleet of wheeled and sand-blasted armored vehicles that can be equipped to carry out missions such as fire support by making a series of modifications. For example, BTR 50 and 60 series and BMP 1 and 2 personnel carriers are among these armored vehicles. Such robust plans of the government of countries in Middle East to rapidly increase the fleet of armored vehicles are anticipated to propel the growth of the military vehicles market in the coming years.

Turkey to Dominate Market Share During the Forecast Period

Turkey has been significantly investing in its defense industry and expanding production. The recent focus on domestic design and production stems from an increase in potential threats from Russia and various militant groups and from sanctions placed on Turkey's defense industry by its NATO allies. In this context, in May 2023, Turkey's FNSS Defence Systems was contracted to provide capability enhancement to the Turkish Army's ACV-15 advanced armored personnel carriers (AAPCs). The agreement was signed to boost the vehicle's performance and extend its service life for an additional 20 years. According to the company, an undisclosed number of AAPCs will be fitted with modern subsystems to support more missions and help address sophisticated threats on the battlefield.

Turkey's procurement and defense authorities have launched a program designed to increase the structural life of the country's existing fleet of F-16 Block 30 jets from 8,000 flight hours to 12,000. The upgrades may cover 1,200 to 1,500 parts per aircraft.

In addition, Turkey has vastly advanced in armored vehicle manufacturing and is acquiring new vehicles to modernize its fleet and with its interest in upgrading its naval fleet to further contribute to the growth of the market. For instance, in April 2023, the Turkish Navy received its largest vessel, the amphibious assault ship TCG Anadolu which is Turkey's first landing platform dock. The military will deploy heavy helicopters, drones and light-attack aircraft from the vessel.

Middle East Military Vehicles Industry Overview

The Middle East military vehicles market is semi-consolidated and is marked by the presence of several local and international players vying for a larger market share. Some of the prominent players include Rostec, Lockheed Martin Corporation, The Boeing Company, Saudi Arabian Military Industries (SAMI), and Leonardo S.p.A.

The growing focus on indigenous manufacturing of military vehicles is anticipated to increase the market share of local players during the forecast period. Countries like Turkey, Saudi Arabia, and the United Arab Emirates are the frontrunners in indigenous manufacturing. For instance, Saudi Arabia is focused on enhancing its defense weapon and ammunition manufacturing capability to reduce its dependency on the export of military equipment and weapons in line with the Saudi government's Vision 2030. The government plans to increase the local military equipment spending to 50% by 2030. Saudi Arabian Military Industries (SAMI), BMC Otomotiv Sanayi ve Ticaret AS, and Denel SOC Ltd are prominent local manufacturers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Military Aircraft

- 5.1.1 Combat Aircraft

- 5.1.1.1 Fighter Aircraft

- 5.1.1.2 Combat Helicopters

- 5.1.2 Non-combat Aircraft

- 5.1.2.1 Reconnaissance and Surveillance Aircraft

- 5.1.2.2 Trainer Aircraft

- 5.1.2.3 Transport Aircraft

- 5.1.2.4 Other Non-combat Aircraft

- 5.1.1 Combat Aircraft

- 5.2 Naval Vessels

- 5.2.1 Destroyers

- 5.2.2 Frigates

- 5.2.3 Corvettes

- 5.2.4 Submarines

- 5.2.5 Other Naval Vessels

- 5.3 Armored Vehicles

- 5.3.1 Armored Personnel Carriers

- 5.3.2 Infantry Fighting Vehicles

- 5.3.3 Mine-Resistant Ambush Protected

- 5.3.4 Main Battle Tanks

- 5.3.5 Other Armored Vehicles

- 5.4 Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Turkey

- 5.4.5 Israel

- 5.4.6 Rest of the Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Rostec

- 6.2.2 Lockheed Martin Corporation

- 6.2.3 The Boeing Company

- 6.2.4 Abu Dhabi Ship Building Co.

- 6.2.5 IAI

- 6.2.6 BMC Otomotiv Sanayi ve Ticaret A.S.

- 6.2.7 Fincantieri S.p.A.

- 6.2.8 Saudi Arabian Military Industries (SAMI)

- 6.2.9 Dassault Aviation SA

- 6.2.10 Naval Group

- 6.2.11 Denel SOC Ltd.

- 6.2.12 BAE Systems plc

- 6.2.13 Oshkosh Corporation

- 6.2.14 Airbus SE

- 6.2.15 Leonardo S.p.A.

- 6.2.16 Patria Group

- 6.2.17 FNSS Savunma Sistemleri A.S.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日