|

市場調査レポート

商品コード

1690834

米国と欧州の再利用可能プラスチック製リターナブル輸送包装:市場シェア分析、産業動向、成長予測(2025~2030年)United States and Europe Reusable Plastic Returnable Transport Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国と欧州の再利用可能プラスチック製リターナブル輸送包装:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

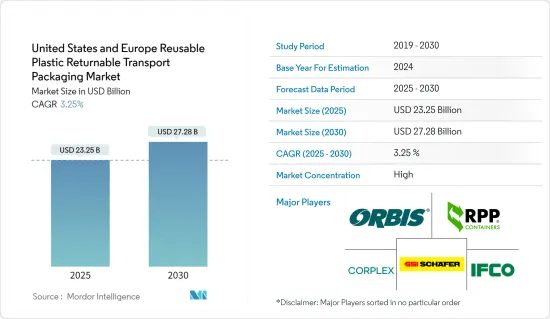

米国と欧州の再利用可能プラスチック製リターナブル輸送包装市場規模は、2025年に232億5,000万米ドルと推定・予測され、2030年には272億8,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは3.25%です。

物流産業では、サステイナブルリターナブル包装を採用することで、事業全体の物流包装コストを削減し、市場の需要を生み出しています。

主要ハイライト

- RPCを使用する利点、例えば、低コストで無駄の少ないサプライチェーンが収益に直接節約をもたらし、品質と鮮度を守り、サプライチェーン全体を最適化し、包装の無駄を防ぐことで環境への影響を減らす、などが市場の成長を促進する要因です。

- 米国と欧州におけるeコマース産業の成長と相まって、商品の輸出入需要が増加していることが、予測期間中に市場の成長を大きく促進すると予想されます。米国国勢調査局によると、2021年の米国における物品の輸出入総額はそれぞれ2兆8,329億米ドル、1兆7,546億米ドルを占めています。

- しかし、再利用可能プラスチック製RTPを採用するかどうかは、サプライチェーン全体の利害関係者がその利点を認識するかどうかに大きくかかっています。Orbis Corporationの調査によると、サプライチェーン幹部の46%が、サプライチェーンの業績を阻害する主要因として、プロセス変更への抵抗を挙げています。このように、産業の人々の受け入れ不足は、調査対象市場の成長にとって課題となっています。

- 調査対象地域の政府も、廃棄物のない循環型経済を可能にするために、再利用可能でリサイクル可能な代替包装の使用を強調しており、これは調査対象市場の成長に寄与する重要な要因の一つです。欧州委員会は、固形廃棄物を削減し、循環型経済を推進するための立法努力を強めています。

- 市場の主要企業数社は、業務効率を高めるために技術的な進歩を伴うソリューションを開発しています。例えば、2022年4月、CHEPはBXBデジタルと提携し、モノのインターネット(IoT)によるデジタルソリューションを開発し、顧客のサプライチェーンの業務効率化を図りました。CHEPの再利用可能なパレットとコンテナのセットには、南欧州全域で追跡・追跡装置が装備され、プラットフォームとその上で輸送される製品の可視性を高めています。

- COVID-19の発生は、世界中の国際貿易と、必要不可欠な商品サービスと必要不可欠でない商品サービスのサプライチェーンに影響を与えました。パンデミックによる工業生産の減少は、市場の成長に大きな影響を与えました。

米国と欧州の再利用可能プラスチック製リターナブル輸送包装の市場動向

パレットが主要市場シェアを占める

- プラスチックパレットは、製品を満載して保管・出荷するために使用されます。その輪郭のあるオールプラスチック構造は、釘、錆、破片(木製パレットによく見られる)による損傷から製品を保護します。このことが、米国におけるペレットの需要を牽引しています。

- さらに、再利用可能な包装は、カッターナイフ、ホッチキス、壊れた木製パレットによる怪我をなくします。米国西部に240店舗を展開する大手スポーツ用品小売業者Big 5 Corporationは、入れ子式プラスチックパレットに移行し、木製パレットがばらばらになることによる怪我や備品の損傷をなくしました。この移行により、人間工学が改善され、施設が清潔になり、作業員の生産性が向上し、倉庫のスペースが節約されました。

- 食品産業や製薬産業のさまざまな小売業者が木製パレットをプラスチックパレットに置き換えているのは、衛生と安全が両部門の最優先事項であり、変形した木製パレットが機械式コンベアベルトを塞ぐ恐れがあるため、企業の倉庫に自動化技術を採用することで需要に対応しているためです。例えば、最近、フランス最大の食品小売業者のひとつが、物流業務において木製パレットを置き換え、現在はプラスチックパレットの在庫を増やしています。29の倉庫と1,600のスーパーマーケットを結ぶ内部フロー用に、この運送業者は33万枚のクレイマーCS1プラスチックパレットを購入しました。

- この地域の企業は、エンドユーザーのニーズに応えるため、HDPEプラスチックパレットを絶えず発売しています。例えば、2021年9月、Craemer Groupは、安全性と衛生面を第一に考え、完全に滑り止め加工されたトップデッキを備えた完全密閉型プラスチックパレット、TC3-5 Palgripの発売を発表しました。高密度ポリエチレン(HDPE)プラスチック製で、トップデッキとボトムデッキが完全に密閉されているため、衛生第一のオペレーションに最適。

大きく成長する飲食品エンドユーザー市場

- 飲食品産業では、RTP包装は飲食品原料の農場から加工工場への輸送など、サプライチェーン全体で使用されています。プラスチック製食品パレットなどのRTP包装ソリューションは、サプライチェーン全体を通じて、加工、保管、流通用途で飲料ボトルや缶を保護します。再利用可能プラスチック容器(RPC)は、米国と欧州において、農場や食品加工施設から小売店や外食産業への生鮮食品の包装と輸送のために設計され、使用されています。

- 欧州では、飲料を考慮すると、国境を越えた製品の流れには、牛乳、水、乳製品、ビール、ソフトドリンク、ワインの輸送が含まれます。欧州連合(EU)の調査によると、ワイン以外の飲料は生産国で90%以上が消費されています。しかし、EU域内市場では相当量のワインが国境を越えて流通し、消費地ではその多くがバルクコンテナで輸出されています。

- 欧州のいくつかの国では、様々な種類の包装のリサイクルに力を入れています。以前は、リターナブルの輸送用プラスチック包装は各国政府の包装法には含まれていなかったが、近年ではこの包装も含まれるようになっています。例えば、2021年7月にドイツ包装法が改正され、B2B輸送包装、商業包装、リターナブル包装などを含む事業所包装がある場合、2022年7月からLUCIDポータルへの登録が義務付けられました。

- バリューチェーン内での様々なパートナーシップなどの市場開拓が、この地域の市場成長を後押ししています。例えば、2021年2月、サプライチェーンソリューション企業であるCHEPは、Coca-Cola European Partners(CCEP)と新たに5年契約を締結し、2025年4月まで西欧地域全体でプールパレットを供給すると発表しました。

米国と欧州の再利用可能プラスチック製リターナブル輸送包装産業概要

米国と欧州の再利用可能プラスチック製リターナブル輸送包装市場はセグメント化されており、市場参入企業は激しい競争の中で事業を展開し、その地位を維持するために製品ポートフォリオを継続的にアップグレードしています。

- 2021年8月-Sohner Kunststofftechnikは、折りたたみ可能な大型荷物用キャリアMegaPack ALPHA 1500 x 800 x 800とMegaPack BETA 1800 x 800 x 800の製品レンジに、2つの大判標準ソリューションを追加しました。これらのプラスチックコンテナは、シートフレーム、パネル、配線など、比較的重量の軽い自動車部品の大量輸送に適しています。

- 2021年11月-Toscaは新製品NeRa Palletを発表しました。入れ子式、ラック式、積み重ね可能な頑丈なプラスチックパレットで、自動化された流通サプライチェーン全体において画期的な効率化を実現。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場力学

- 市場の促進要因

- 有利な政府規制

- 自動化による再利用可能プラスチックRTPの需要増加

- 市場抑制要因

- 様々な利害関係者によるプロセス変更への抵抗

- 代替材料の入手可能性

- 市場機会

- eコマース食品セグメントからの需要増加

第6章 世界のRTP産業動向概要

第7章 市場セグメンテーション

- 製品別

- 再利用可能プラスチック容器

- パレット

- 段ボール箱パネル

- IBC

- クレートとトート

- その他

- エンドユーザー産業別

- 飲食品

- 自動車

- 耐久消費財

- 工業(化学を含む)

- その他のエンドユーザー別

- 地域別

- 米国

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- その他の欧州(イタリア、ポーランドなど)

第8章 競合情勢

- 企業プロファイル

- IFCO Systems

- Corplex Corporation

- Schaefer Systems International Inc.

- RPP Containers

- Orbis Corporation(Menasha Corporation)

- Friedola TECH GmbH(Con-Pearl)

- Sohner Plastics LLC

- Tosca Ltd

- Sustainable Transport Packaging(Reusable Transport Packaging)

- CABKA

- Auer

- Wisechemann

- Soehner

- Duro-Therm

- Conteyor

- KTP

- Wellplast

- Kiga

- WI Sales

第9章 投資分析

第10章 投資分析市場の将来展望

The United States and Europe Reusable Plastic Returnable Transport Packaging Market size is estimated at USD 23.25 billion in 2025, and is expected to reach USD 27.28 billion by 2030, at a CAGR of 3.25% during the forecast period (2025-2030).

Adopting sustainable returnable packaging in the logistics industry to reduce the cost of their logistics packaging across their operations creates demand in the market.

Key Highlights

- The benefits of using RPC, such as lower cost and less wasteful supply chain that delivers savings directly to the bottom line, protect quality and freshness, optimizes the overall supply chain reducing environmental impact by preventing packaging waste, are the factors propelling the growth of the market.

- The increasing demand for the export and import of goods, coupled with the growing e-commerce industry in the United States and Europe, is expected to drive the growth of the market significantly during the forecast period. According to the US Census Bureau, the total imports and exports of goods in the United States accounted for USD 2,832.9 billion and USD 1,754.6 billion, respectively, in 2021.

- However, adopting reusable plastic RTP largely depends on the stakeholders across the supply chain realizing its benefits. According to a survey by Orbis Corporation, 46% of the supply chain executives mentioned resistance to process change as the major factor that may impede their supply chain performance. Thus, the lack of acceptance from people in the industry poses a challenge to the growth of the studied market.

- The governments in the studied regions are also emphasizing using reusable and recyclable packaging alternatives to enable a waste-free and circular economy, which is one of the important factors contributing to the growth of the studied market. The European Commission has increased its legislative efforts to reduce solid waste and promotes a circular economy.

- Several key players in the market are developing solutions with technological advancements to increase their operational efficiency. For instance, in April 2022, CHEP, in partnership with BXB Digital, developed digital solutions based on the Internet of Things (IoT) that seek to increase the operational efficiency of their customers' supply chains. A set of CHEP's reusable pallets and containers have been equipped with track and trace devices across Southern Europe to increase visibility over the platforms and the products transported on them.

- The COVID-19 outbreak affected international trade and the supply chains of essential and non-essential goods and services worldwide. The decline in industrial production due to the pandemic significantly affected the growth of the market.

Reusable Plastic Returnable Transport Packaging in the US & Europe Market Trends

Pallets to Account for Major Market Share

- Plastic pallets are used to store and ship full loads of products. Their contoured, all-plastic structure protects the product from damage from nails, rust, or splinters (commonly found in wood pallets). This factor is driving the demand for these pellets in the United States.

- In addition, reusable packaging eliminates injuries from box cutters, staples, and broken wooden pallets. Big 5 Corporation, a major sporting goods retailer with 240 stores in the Western United States, shifted to nestable plastic pallets, which eliminated injuries and equipment damage from wood pallets falling apart. This move improved ergonomics, made for cleaner facilities, increased worker productivity, and saved space in the warehouse.

- Various retailers from the food and pharmaceutical industries are replacing wooden pallets with plastic pallets due to sanitation and safety are top priorities in both sectors and the adoption of automation technology in the company's warehouse is catering to the demand because deformed wooden pallets threaten to block the mechanical conveyor belts. For instance, recently, one of France's largest food retailers has replaced its wooden pallet in its logistics operations and is now building up its inventory of plastic pallets. For the internal flow of goods between its 29 warehouses and 1,600 supermarkets in the chain, the freight forwarder has purchased 330,000 Craemer CS1 plastic pallets.

- Companies in the region are constantly launching HDPE Plastic pallets to meet the end-user needs. For instance, in September 2021, Craemer Group announced the launch of TC3-5 Palgrip, the completely closed plastic pallet with a fully anti-slip coated top deck that puts safety and hygiene at the forefront. It is made from high-density polyethylene (HDPE) plastic, perfect for hygienic-first operations since the top and bottom decks are completely closed.

Food and Beverage End-user Vertical to Grow Significantly

- In the food and beverage industry, RTP packaging is used throughout the supply chain, such as for transporting food and beverage raw materials from farms to processing plants. RTP packaging solutions such as plastic food pallets protect beverage bottles and cans during processing, storage, and distribution applications throughout the supply chain. Reusable Plastic Containers (RPCs) are designed and used for packing and transporting perishable food items from farm and food processing facilities to retail and food service establishments in the United States and Europe.

- In Europe, considering beverages, cross-border product flows include transportation of milk, water, dairy products, beer, soft drinks, and wine. According to the European Union Study, except wine, all the other beverages are consumed by more than 90% in the country where they are produced. However, a substantial amount of wine travels across borders in the EU-internal market while a large amount of that is exported in bulk containers in the area of consumption.

- Several countries in Europe are emphasizing on recycling of various types of packaging. Earlier, returnable transport plastic packaging was not included in the packaging laws by the national governments; however, in recent years, they have included this packaging also. For instance, in July 2021, the German Packaging Act was amended, which made it mandatory to register in the LUCID portal from July 2022 if any business place packaging, including B2B transport packaging, commercial packaging, and returnable packaging, among others.

- Market developments such as various partnerships within the value chain are helping the market growth in the region. For instance, in February 2021, CHEP, a supply chain solutions company, announced a new five-year contract with Coca-Cola European Partners (CCEP), which will be in effect until April 2025, to supply pooled pallets across the Western Europe region.

Reusable Plastic Returnable Transport Packaging in the US & Europe Industry Overview

The US and European Reusable Plastic Returnable Transport Packaging Market is fragmented, as the market players are operating in a highly competitive landscape and are continuously upgrading their product portfolio in order to hold their positions.

- August 2021 - Sohner Kunststofftechnik added two large-format standard solutions to its range of foldable large load carriers MegaPack ALPHA 1500 x 800 x 800 and MegaPack BETA 1800 x 800 x 800. These plastic containers are appropriate for shipping high-volume automotive components with relatively low weights, such as seat frames, paneling, and wiring.

- November 2021 - Tosca introduced a new product NeRa Pallet. It is a nestable, rackable, and stackable heavy-duty plastic pallet that can deliver game-changing efficiencies throughout the automated distribution supply chain.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Favorable Governmental Regulations

- 5.1.2 Automation to Increase the Demand for Reusable Plastic RTP

- 5.2 Market Restraints

- 5.2.1 Resistance to Process Change by Various Stakeholders

- 5.2.2 Availability of Alternative Materials

- 5.3 Market Opportunities

- 5.3.1 Increasing Demand from E-commerce Food Sector

6 SUMMARY ON GLOBAL RTP INDUSTRY TRENDS

7 MARKET SEGMENTATION

- 7.1 By Product

- 7.1.1 Reusable Plastic Containers

- 7.1.2 Pallets

- 7.1.3 Corrugated Boxes and Panels

- 7.1.4 IBCs

- 7.1.5 Crates and Totes

- 7.1.6 Other Product Types

- 7.2 By End-user Vertical

- 7.2.1 Food and Beverage

- 7.2.2 Automotive

- 7.2.3 Consumer Durables

- 7.2.4 Industrial (including Chemicals)

- 7.2.5 Other End-user verticals

- 7.3 By Geography

- 7.3.1 United States

- 7.3.2 Europe

- 7.3.2.1 United Kingdom

- 7.3.2.2 Germany

- 7.3.2.3 France

- 7.3.2.4 Spain

- 7.3.2.5 Rest of Europe (Italy, Poland, etc.)

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 IFCO Systems

- 8.1.2 Corplex Corporation

- 8.1.3 Schaefer Systems International Inc.

- 8.1.4 RPP Containers

- 8.1.5 Orbis Corporation (Menasha Corporation)

- 8.1.6 Friedola TECH GmbH (Con-Pearl)

- 8.1.7 Sohner Plastics LLC

- 8.1.8 Tosca Ltd

- 8.1.9 Sustainable Transport Packaging (Reusable Transport Packaging)

- 8.1.10 CABKA

- 8.1.11 Auer

- 8.1.12 Wisechemann

- 8.1.13 Soehner

- 8.1.14 Duro-Therm

- 8.1.15 Conteyor

- 8.1.16 KTP

- 8.1.17 Wellplast

- 8.1.18 Kiga

- 8.1.19 WI Sales