|

市場調査レポート

商品コード

1698579

リユーザブル輸送用パッケージング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Reusable Transport Packaging (RTP) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| リユーザブル輸送用パッケージング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月12日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

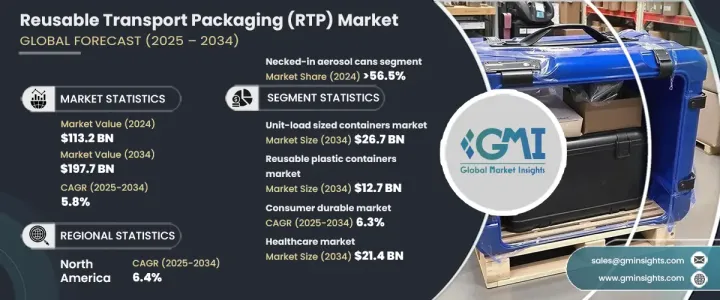

リユーザブル輸送用パッケージングの世界市場は、2024年に1,132億米ドルに達し、2025年から2034年にかけてCAGR 5.8%で成長すると予測されています。

温室効果ガス排出に対する懸念の高まりが、持続可能な包装ソリューションへのシフトを促しています。企業はコスト効率の高いロジスティクスに注目しており、リユーザブル輸送用パッケージング(RTP)は、包装コストや廃棄物処理コストを削減できることから支持を集めています。RFIDやIoTトラッキングなどの先進技術は、効率をさらに高めています。政府や業界の利害関係者は、気候変動と闘うためにリユーザブル包装を推進しており、その取り組みの中心は二酸化炭素排出量の削減です。

リユーザブル輸送用パッケージングには、ハンドヘルド・クレート、パレット、ダンネージ、貨物保護、リユーザブルプラスチック・コンテナ、単位積載サイズのコンテナ、タンク、ドラム缶、樽が含まれます。2024年に683億米ドルと評価されるパレット市場は、出荷条件の改善のために技術革新が進んでいます。ハンドヘルド・クレートは、2034年までに256億米ドルに達すると予想され、効率的な製品取り扱いのために小売業者に広く採用されています。2024年に33億米ドルと評価されるダンネージと貨物保護セグメントは、壊れやすい品物を保護するためにますます使用されるようになっています。2034年までに267億米ドルに達すると推定されるユニットロードサイズのコンテナは、スペースの最適化と廃棄物の削減に不可欠です。リユーザブルプラスチック容器市場は2034年までに127億米ドルに達すると予測され、センサーの統合によりリアルタイムの追跡が強化されます。タンク、ドラム缶、樽は、2034年までに62億米ドルに達すると予測され、バルク液体や危険物を輸送する産業にとって引き続き不可欠です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,132億米ドル |

| 予測金額 | 1,977億米ドル |

| CAGR | 5.8% |

材料タイプ別に見ると、市場はプラスチック、金属、木材に区分されます。2024年には、プラスチックが26.4%の市場シェアを占め、高密度ポリエチレン(HDPE)木箱のような軽量で耐久性のあるソリューションへの需要が牽引しています。金属製包装市場は2034年までに261億米ドルに達すると予想され、頑丈な用途向けの堅牢なソリューションを提供します。2034年までに1,252億米ドルに達すると予想される木材ベースの包装は、輸送のニーズに対してコスト効率が高く、生分解可能な選択肢であり続けています。メーカーは、持続可能性と効率性を確保するために、リユーザブル材料で製品を拡大しています。

市場はさらに、飲食品、耐久消費財、自動車、ヘルスケアなどの最終用途産業別に分類されます。飲食品分野は2024年に364億米ドルとなり、腐敗を防ぐためにリユーザブル容器の需要が増加しています。耐久消費財分野は、持続可能なロジスティクス・ソリューションが電子機器や家電製品に採用されつつあることから、CAGR 6.3%の成長が見込まれています。自動車市場は2034年までに429億米ドルに達すると予測され、メーカーは高強度の再利用可能パレットに依存しています。ヘルスケア分野は2034年までに214億米ドルに達すると予測され、デリケートな医療機器を輸送するために、使い捨てプラスチックからリユーザブル容器に移行しつつあります。

北米のリユーザブル輸送用パッケージング市場は、予測期間中にCAGR 6.4%で成長する見込みです。同地域では持続可能な包装ソリューションに対する需要が急増しており、企業や消費者は環境に優しい物流を優先しています。企業はリユーザブル輸送用パッケージングを採用することで、環境への影響を減らしつつコストを削減しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- リユーザブル輸送用パッケージングソリューションの需要につながる世界の温室効果ガス排出量の増加

- シングルユースパッケージからリユーザブル包装容器へのシフトの高まり

- リユーザブルパッケージの持続可能なオプションに対する嗜好の高まり

- リユーザブルパッケージの導入における政府からの支援の高まり

- 効率的な輸送と物流処理のための革新的なリユーザブルパッケージングデザインの開発増加

- 業界の潜在的リスク&課題

- リユーザブル容器の状態を追跡するリアルタイム透明性の欠如

- 製造と設計に伴う高コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:包装タイプ別、2021年~2034年

- 主要動向

- パレット

- ハンドヘルド・クレート

- ダンネージと貨物保護

- ユニットロードコンテナ

- リユーザブルプラスチック容器

- タンク、ドラム、バレル

- その他

第6章 市場推計・予測:素材別、2021年~2034年

- 主要動向

- プラスチック

- 金属

- 木材

第7章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 飲食品

- 耐久消費財

- 自動車

- ヘルスケア

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Auer Packaging

- Borealis AG

- CABKA

- CDF Corporation

- DS Smith

- DW Reusables

- Georg Utz Holding AG

- Greif Inc.

- GWP Group

- IFCO SYSTEMS

- IPL, Inc.

- Mauser Packaging Solutions

- Myers Industries

- Nefab Group

- ORBIS Corporation

- Rotovia Deventer bv

- Schoeller Allibert

- Schutz GmbH &Co. KGaA

- SSI SCHAEFER

- Werit

The Global Reusable Transport Packaging Market reached USD 113.2 billion in 2024 and is projected to grow at a CAGR of 5.8% from 2025 to 2034. Rising concerns over greenhouse gas emissions are driving a shift towards sustainable packaging solutions. Businesses are focusing on cost-efficient logistics, and reusable transport packaging (RTP) is gaining traction due to its ability to reduce packaging and waste disposal costs. Advanced technologies such as RFID and IoT tracking are further enhancing efficiency. Governments and industry stakeholders are promoting reusable packaging to combat climate change, with efforts centered on reducing carbon emissions.

Reusable transport packaging includes handheld crates, pallets, dunnage and cargo protection, reusable plastic containers, unit-load-sized containers, tanks, drums, and barrels. The pallet market, valued at USD 68.3 billion in 2024, is undergoing innovations for improved shipment conditions. Handheld crates, expected to reach USD 25.6 billion by 2034, are widely adopted by retailers for efficient product handling. The dunnage and cargo protection segment, valued at USD 3.3 billion in 2024, is increasingly used for safeguarding fragile items. Unit-load-sized containers, estimated to reach USD 26.7 billion by 2034, are critical for space optimization and waste reduction. The reusable plastic container market is forecasted to reach USD 12.7 billion by 2034, with sensor integration enhancing real-time tracking. Tanks, drums, and barrels, projected to hit USD 6.2 billion by 2034, remain essential for industries transporting bulk liquids and hazardous materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $113.2 Billion |

| Forecast Value | $197.7 Billion |

| CAGR | 5.8% |

By material type, the market is segmented into plastic, metal, and wood. In 2024, plastic held a 26.4% market share, driven by the demand for lightweight and durable solutions such as high-density polyethylene (HDPE) crates. The metal packaging market is expected to reach USD 26.1 billion by 2034, offering robust solutions for heavy-duty applications. Wood-based packaging, anticipated to reach USD 125.2 billion by 2034, remains a cost-effective and biodegradable option for transportation needs. Manufacturers are expanding their offerings with reusable materials to ensure sustainability and efficiency.

The market is further categorized by end-use industries, including food and beverages, consumer durables, automotive, and healthcare. The food and beverage sector, valued at USD 36.4 billion in 2024, is witnessing an increase in demand for reusable containers to prevent spoilage. The consumer durables segment is expected to grow at a CAGR of 6.3% as sustainable logistics solutions are increasingly adopted for electronics and home appliances. The automotive market is projected to reach USD 42.9 billion by 2034, with manufacturers relying on high-strength reusable pallets. The healthcare sector, forecasted to reach USD 21.4 billion by 2034, is shifting from single-use plastics to reusable containers for transporting delicate medical equipment.

North America's reusable transport packaging market is expected to grow at a CAGR of 6.4% during the forecast period. The region is experiencing a surge in demand for sustainable packaging solutions, with businesses and consumers prioritizing eco-friendly logistics. Companies are adopting reusable transport packaging to lower costs while reducing environmental impact.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global greenhouse gas emissions leading to demand of reuseable transport packaging solutions

- 3.2.1.2 Growing shift from single-use packages to reusable packaging containers

- 3.2.1.3 Rising preferences towards the sustainable options of reusable packages

- 3.2.1.4 Growing support from the government in implementing reusable packaging

- 3.2.1.5 Increasing development of innovative reusable packaging design for efficient transport and logistic handling

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of real-time transparency in tracking the status of reusable containers

- 3.2.2.2 High cost associated with manufacturing and design

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Packaging Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pallets

- 5.3 Handheld crates

- 5.4 Dunnage & cargo protection

- 5.5 Unit-load sized containers

- 5.6 Reusable plastic containers

- 5.7 Tanks, drums, & barrels

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Metal

- 6.4 Wood

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Consumer durables

- 7.4 Automotive

- 7.5 Healthcare

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Auer Packaging

- 9.2 Borealis AG

- 9.3 CABKA

- 9.4 CDF Corporation

- 9.5 DS Smith

- 9.6 DW Reusables

- 9.7 Georg Utz Holding AG

- 9.8 Greif Inc.

- 9.9 GWP Group

- 9.10 IFCO SYSTEMS

- 9.11 IPL, Inc.

- 9.12 Mauser Packaging Solutions

- 9.13 Myers Industries

- 9.14 Nefab Group

- 9.15 ORBIS Corporation

- 9.16 Rotovia Deventer bv

- 9.17 Schoeller Allibert

- 9.18 Schutz GmbH & Co. KGaA

- 9.19 SSI SCHAEFER

- 9.20 Werit