|

市場調査レポート

商品コード

1940718

欧州の施設管理:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の施設管理:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

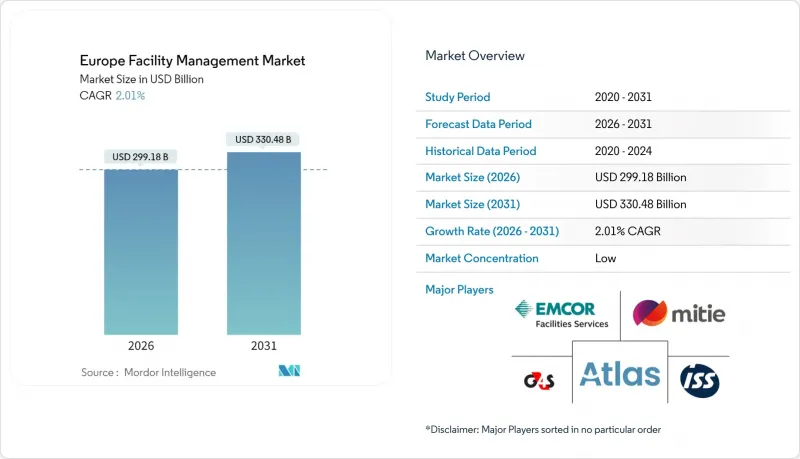

欧州の施設管理市場規模は、2026年に2,991億8,000万米ドルと推定され、2025年の2,932億8,000万米ドルから成長が見込まれます。

2031年の予測では3,304億8,000万米ドルに達し、2026年から2031年にかけてCAGR2.01%で拡大する見通しです。

着実な拡大は、コスト主導の保守からデータ活用型パフォーマンスサービスへの移行、厳格化する省エネルギー規制、公共部門におけるアウトソーシング拡大を反映しています。老朽化する建築設備が機械・電気・配管の集中的なメンテナンスを必要とする中、ハードサービスは業界の基盤であり続けます。一方、健康・ウェルネス・体験重視の職場環境を背景に、ソフトサービスは加速しています。ロシア・ウクライナ紛争以降のエネルギー価格上昇により、顧客は時間・材料制業務よりも最適化契約を好む傾向が強まっています。ESG報告規則やデジタル技術の複雑化が専門知識を要求する中、アウトソーシングは規模を拡大しています。テケム社の72億米ドル取引に代表されるプライベート・エクイティの関心は、このセグメントの継続的収益構造に対する信頼を裏付けています。

欧州施設管理市場の動向と洞察

老朽化した建築ストック:改修主導のFM支出

欧州の建築ストックの4分の3は築50年以上であり、技術的メンテナンスとエネルギー効率化を組み合わせた包括的な改修プログラムへの持続的な需要を生み出しています。セントリカ社がセントジョージ大学病院と締結した15年間の契約(年間6,000トンの二酸化炭素削減と110万米ドルの節約を実現)のようなパフォーマンス契約モデルは、改修を主眼とした施設サービスの財務的実現可能性を示しています。ドイツとフランスのポートフォリオは、ネット・ゼロ・エネルギー建築基準の強化に伴い、改修時にIoTセンサー、予知保全、エネルギー性能分析を統合する必要性が最も差し迫っています。欧州投資銀行は、エネルギー効率化のための年間資金不足額を1,850億ユーロと試算しており、施設サービスプロバイダーが資本調達における重要な仲介者としての役割を担っています。

財政緊縮後の公共部門におけるアウトソーシングの勢い

政府機関は効率化目標とESG開示義務の達成に向け、複合サービスを一括して外部事業者に委託しています。英国労働年金省はISS社と年間1億7,500万米ドル規模の7年契約を締結し、清掃・給食・設備保守を一元管理。北欧・ドイツ自治体もこれに追随し、リンカンシャー州議会とVINCI Facilities社が締結した10年枠組み契約では協働型エネルギー管理を優先しています。医療施設は、24時間365日の運営、感染管理、高エネルギー消費の空調設備負荷により専門的な支援が必要となるため、特に導入が進んでいます。

経済的圧力(インフレ、コスト最適化)

人件費、資材費、エネルギーコストの上昇を受け、クライアントは契約の再交渉を進め、裁量的なFM支出を抑制しています。CBREの調査によれば、2023年にFM予算を増額した組織は35%であったもの、29%が依然としてサプライチェーンの混乱を最大の脅威として挙げています。ソデクソの欧州事業は、医療クライアントが入札を延期したため、2025年度上半期の有機的成長率がわずか2.1%に留まりました。価格感応度の高さがコモディティ化を促進する南欧・東欧地域では、利益率の圧迫が特に深刻です。

セグメント分析

ハードサービスは2025年時点で欧州施設管理市場の61.05%を占め、老朽化する建物基盤全体におけるMEP(機械電気設備)、HVAC(空調設備)、防火安全の維持管理の必要性を浮き彫りにしています。継続的な改修活動により、業界全体の成長は緩やかであるもの、ハードサービス分野の欧州施設管理市場規模は拡大を続けています。予測型資産管理は、設備のライフサイクル延長やエネルギー使用規制への対応を求める顧客の需要により、普及が進んでいます。

ソフトサービスは規模こそ小さいもの、従業員体験戦略において高度な清掃、コンシェルジュ、セキュリティパッケージが優先されることから、4.61%の予測CAGRを達成すると見込まれます。ハイブリッドワークの普及により、スペース予約、柔軟なケータリング、非接触型アクセス制御の需要が高まり、従来型フロント業務にテクノロジーが組み込まれています。来客数分析などのソフトサービスデータがエネルギーアルゴリズムにフィードバックされることで統合機会が生まれ、プロバイダーはクライアントの業務計画にさらに深く関与しています。

欧州施設管理市場は、サービス種別(ハードサービスとソフトサービス)、提供形態(社内提供と外部委託)、エンドユーザー産業(商業、ホスピタリティ、公共インフラ・機関、医療、工業・プロセス、その他エンドユーザー産業)、国別にセグメンテーションされます。市場予測は金額ベース(米ドル)で提示されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 欧州商業用不動産における現在の稼働率

- 主要FMプロバイダーの収益性ベンチマーク

- 労働力指標- 熟練労働者と非熟練労働者の参加状況

- サービス種類別施設管理市場シェア(%)

- ハードサービス別施設管理市場シェア(%)

- ソフトサービス別施設管理市場シェア(%)

- 主要都市圏における都市化と人口増加

- 欧州におけるセクター投資優先順位インフラ整備計画

- 労働基準および安全基準に特化した規制上の促進要因

- EUグリーンディールにおけるエネルギー効率目標がFM需要に与える影響

- 技術統合:IoTとAIがサービス提供を変革

- 変化する職場環境:ハイブリッドワークがFMの優先事項を再構築

- 市場促進要因

- 老朽化した建築ストック:改修主導のFM支出

- 財政緊縮後の公共部門におけるアウトソーシングの動向

- エネルギー価格の変動性によるエネルギー最適化FMサービスの加速

- ESG報告義務化によるデータ駆動型FMソリューションの必要性

- パンデミック後の健康・安全認証需要

- プライベート・エクイティによる統合が統合型FM導入を促進

- 市場抑制要因

- 経済的圧力(インフレ、コスト最適化)

- EU域内の規制体制の分断が標準化された提供を阻害

- 限定的なプロップテック相互運用性が統合コストを増加させる

- 接続されたビルシステムに対するサイバーセキュリティリスク

- バリューチェーン分析

- PESTEL分析

- 新規参入企業向けの規制・法的枠組み

- マクロ経済指標がFM需要に与える影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資と資金調達分析

第5章 市場規模と成長予測

- サービスタイプ別

- ハードサービス

- 資産管理

- MEPおよびHVACサービス

- 消防システムと安全対策

- その他のハードFMサービス

- ソフトサービス

- オフィスサポートおよびセキュリティ

- 清掃サービス

- ケータリングサービス

- その他のソフトFMサービス

- ハードサービス

- 提供形態別

- 社内

- 外部委託

- 単一FM

- 包括的施設管理サービス

- 統合型施設管理(Integrated FM)

- エンドユーザー業界別

- 商業(IT・通信、小売・倉庫)

- ホスピタリティ(ホテル、飲食店、大規模レストラン)

- 公共・公共インフラ(政府、教育、交通機関)

- 医療(公的・民間施設)

- 工業・プロセス産業(製造業、エネルギー、鉱業)

- その他のエンドユーザー産業(集合住宅、娯楽、スポーツ・レジャー)

- 国別

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- スロベニア

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Mitie Group PLC

- Emcor Facilities Services WLL

- Atlas FM Ltd.

- G4S Facilities Management UK Ltd.

- ISS Global

- Engie FM Ltd.(Cofely AG)

- Andron Facilities Management

- Apleona GmbH

- Dussmann Group

- Vinci Facilities Ltd.

- Okin Group

- Aramark Corporation

- CBRE Group Inc.

- Assured Europe

- Jones Lang LaSalle Inc.

- Sodexo SA

- Johnson Controls International plc

- Bouygues Energies and Services

第7章 市場機会と将来の動向

- 空白領域と未充足ニーズの評価

- 技術主導型統合FM(IoT、BMS、AIベースの予知保全)

- ESG準拠のFMソリューションへの需要

- 将来のサービスモデルの変化(成果連動型契約)