中国のデータセンター:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

China Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 196 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690785

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

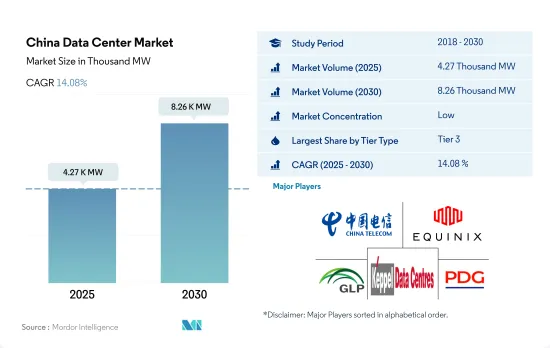

中国のデータセンター市場規模は、2025年に4,270kWと推定され、2030年には8,260kWに達し、CAGR 14.08%で成長すると予測されます。

また、2025年のコロケーション収益は40億1,170万米ドル、2030年には97億660万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは19.33%で成長します。

2023年はティア3データセンターが数量ベースで大半のシェアを占め、ティア4は急成長セグメント

- ティア3データセンターは、オンサイト支援、電力、冷却の冗長性などの機能により、最も好まれています。このセグメントは、2022年の1,115.1MWからCAGR 5.7%で2029年には1,874MWに成長すると予想されています。これらのデータセンターは、主にビジネスクリティカルなデータの保存と処理に利用され、増大するビジネスニーズと拡大性ニーズに対応しています。国内にはティア3データセンターが約110カ所あり、ティア3仕様のデータセンターが37カ所建設中です。

- ティア4データセンターは、そのパフォーマンス、ダウンタイムの少なさ、99.99%のアップタイムにより、大企業に次に好まれています。これらのデータセンターは比較的コストがかかりますが、提供されるパフォーマンスは価格を上回り、大企業の競争と成長のニーズをサポートしています。2022年には、Princeton Digital GroupとSpaceDC Pte Ltdが所有するティア4データセンターが7カ所ありました。

- ティア1と2のデータセンターは、ダウンタイムの長さ、電源と冷却の冗長性、オンサイトのリモートアシスタンスなどの理由から、最も好まれないです。これらのデータセンターはティア3やティア4に比べて比較的安価なため、中小企業や新興企業が好んで利用しています。ティア1とティア2のデータセンターは最も好まれないため、予測期間中は成長が停滞する可能性があります。

中国のデータセンター市場の動向

Huawei、Apple、Xiaomi、Oppo、Vivoは、ハイエンド機能を備えた安価なスマートフォンを提供し、消費者の購買意欲を高めています。

- 2022年の中国のスマートフォンユーザー数は9億5,000万人で、予測期間(2023~2029年)末には18億人に達すると予想され、CAGRは10.2%を記録します。4Gと5G接続が全国に普及したことで、モバイル通信が向上し、スマートフォンが人々の基本的な必需品となっています。

- 中国のスマートフォン企業は、ハイエンドの機能を備えた手頃な価格のスマートフォンを提供しており、国内のスマートフォンユーザーの増加につながっています。ユーザーの約50%が12~18ヵ月ごとに携帯電話を買い替えているため、各社は頻繁に携帯電話を革新しています。現在、市場の主要企業はHuawei、Apple、Xiaomi、Oppo、Vivoです。

- このようなスマートフォンユーザーの増加は、国内のデータセンター市場の成長にプラスの影響を与えています。スマートフォンユーザー数が5倍に増加した調査期間中、データセンターのラック数は2017年の約7万台から2021年には28万台に増加しました。この動向は予測期間中も見られると予想されます。

中国政府の「ブロードバンド・チャイナ戦略」とファイバー接続の拡大が国内のデータセンターを後押し

- 中国政府の「ブロードバンド中国戦略」は2013年に立案され、2015年に実施されました。この戦略の下、2021年にはブロードバンド速度が都市部では住宅用で100Mbps、農村部では20Mbpsに達します。一方、商業・産業用のブロードバンド速度は、2015年の平均速度100Mbpsから2021年には1Gbpsに向上します。光ファイバー接続網のさらなる拡大により、平均速度は今後数年で大幅に上昇すると推定されます。

- 高速データ通信を実現するため、中国市場では光ファイバーケーブルの敷設距離が年々伸びています。同国における光ファイバケーブルネットワークの展開は、2017~2022年にCAGR 8.5%を記録しました。光ファイバーケーブルの配備は、同国のラストマイルインターネット接続に拍車をかけた。これらのケーブルは、より優れた接続性と高い帯域幅を提供するため、ほとんどの企業は、より優れたアップグレードされたサービスを提供するために、従来の銅線ケーブルと交換しました。

- 主にファイバーケーブル経由の安定したブロードバンドスピードは、データセンターの拡大や、他のデータセンターやインターネットエクスチェンジ(IX)との通信に欠かせないです。企業がビジネスの重要データをクラウド、コロケーション、自社内に保管することは一般的になっています。これらの保管場所において、さまざまなサービスがさまざまなサーバーにまたがって顧客に提供されています。通信ポイントの増加に伴い、通信を可能な限り高速に保つことが重要になっています。そのため、中国全土の強力なブロードバンド接続が、予測期間中にデータセンターが100%のアップタイムを維持できるようサポートすることが期待されています。

中国のデータセンター産業概要

中国のデータセンター市場は細分化されており、上位5社で17.92%を占めています。この市場の主要企業は、China Telecom Corporation Ltd、Equinix Inc.、GLP Pte Limited、Keppel DC REIT Management Pte. Ltd、Princeton Digital Groupです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 市場展望

- 耐荷重

- 床面積

- コロケーション収入

- 設置ラック数

- ラックスペース利用率

- 海底ケーブル

第5章 主要産業動向

- スマートフォンユーザー数

- スマートフォン1台当たりのデータトラフィック

- モバイルデータ速度

- ブロードバンドデータ速度

- 光ファイバー接続ネットワーク

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第6章 市場セグメンテーション

- ホットスポット

- 北京

- 広東省

- 河北省

- 江蘇省

- 上海

- その他の中東・アフリカ

- データセンターの規模

- 大規模

- 超大規模

- 中規模

- 極超大規模

- 小規模

- ティアタイプ

- ティア1と2

- ティア3

- ティア4

- 吸収量

- 非利用

- 利用

- コロケーションタイプ別

- ハイパースケール

- リテール

- ホールセール

- エンドユーザー別

- BFSI

- クラウド

- eコマース

- 政府機関

- 製造業

- メディア&エンターテイメント

- テレコム

- その他

第7章 競合情勢

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- BDx Data Center Pte. Ltd

- Chayora Ltd

- China Telecom Corporation Ltd

- Chindata Group Holdings Ltd

- Equinix Inc.

- GDS Service Co. Ltd

- GLP Pte Limited

- Keppel DC REIT Management Pte. Ltd

- Princeton Digital Group

- Space DC Pte Ltd

- Telehouse(KDDI Corporation)

- Zenlayer Inc.

第8章 CEOへの主要戦略的質問

第9章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

The China Data Center Market size is estimated at 4.27 thousand MW in 2025, and is expected to reach 8.26 thousand MW by 2030, growing at a CAGR of 14.08%. Further, the market is expected to generate colocation revenue of USD 4,011.7 Million in 2025 and is projected to reach USD 9,706.6 Million by 2030, growing at a CAGR of 19.33% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, Tier 4 is fastest growing segment

- Tier 3 data centers are the most preferred due to features such as on-site assistance, power, and cooling redundancy. The segment is expected to grow from 1,115.1 MW in 2022 to 1,874 MW by 2029 at a CAGR of 5.7%. These data centers are mainly chosen by companies for storing and processing business-critical data to cater to their growing business and scalability needs. There are around 110 Tier 3 data centers in the country, and around 37 upcoming data centers are under construction with Tier 3 specifications.

- Tier 4 data centers are the next most preferred by large businesses due to their performance, lower downtime, and 99.99% uptime. These data centers are relatively costly; however, the performance offered by them outweighs the price and supports the competitive and growing needs of large businesses. In 2022, the country had seven Tier 4 data centers owned by Princeton Digital Group and SpaceDC Pte Ltd.

- Tier 1 & 2 data centers are the least preferred due to their higher downtime durations, power and cooling redundancies, and on-site remote assistance. Since these data centers are relatively cheap compared to Tier 3 and Tier 4, small businesses and startup companies prefer them. Since Tier 1 & 2 data centers are the least preferred, stagnant growth could be seen during the forecast period.

China Data Center Market Trends

Huawei, Apple, Xiaomi, Oppo, and Vivo offer cheap smartphones with high end features which attracts consumers to spend more these products creating a hige demand in smartphones in the country

- The number of Chinese smartphone users was 950 million in 2022, and the figure is expected to reach 1.8 billion by the end of the forecast period (2023-2029), registering a CAGR of 10.2%. The spread of 4G and 5G connectivity across the country has improved mobile communication, making smartphones a basic necessity for people.

- Chinese smartphone companies are offering affordable smartphones with high-end features, leading to an increase in smartphone users in the country. Around 50% of users replace their phones every 12-18 months, making companies innovate their phones frequently. Currently, the major market players are Huawei, Apple, Xiaomi, Oppo, and Vivo.

- This increase in smartphone users has positively impacted the growth of the data center market in the country. During the study period, when the number of smartphone users increased fivefold, the number of racks in data centers increased from around 70k in 2017 to 280k in 2021. This trend is expected to be witnessed during the forecast period as well.

Chinese government's "Broadband China Strategy coupled with increased fiber connectivity, boost the data centers in the country

- The Chinese government's "Broadband China Strategy," drafted in 2013 and implemented in 2015, is accredited for spreading broadband connectivity across the country, primarily in remote locations. In 2021, under this strategy, the broadband speed reached 100 Mbps for residential use in cities and 20 Mbps in rural regions. On the other hand, the broadband speed for commercial/industrial use increased from an average speed of 100 Mbps in 2015 to 1 Gbps in 2021. With further expansion of the fiber connectivity network, average speeds are estimated to rise significantly in the coming years.

- In order to provide high data speeds, the Chinese market increased the distance of laying fiber optic cables over the years. The deployment of optic fiber cable networks in the country registered a CAGR of 8.5% during 2017-2022. The deployment of fiber optic cables spurred last-mile internet connectivity in the country. As these cables offer better connectivity and higher bandwidths, most companies replaced them with traditional copper cables to offer better and upgraded services.

- Stable broadband speed, predominantly via fiber cables, is crucial for the expansion of data centers and their communication with other data centers and internet exchanges (IX). It has become common for companies to store their business's critical data in the cloud, colocation, and in-house. Within these storage locations, various services are provided to their customers across different servers. With the increase in the number of points of communication, it becomes critical to keep communication as fast as possible. Therefore, strong broadband connectivity across the country is expected to support the data centers to maintain 100% uptime during the forecast period.

China Data Center Industry Overview

The China Data Center Market is fragmented, with the top five companies occupying 17.92%. The major players in this market are China Telecom Corporation Ltd, Equinix Inc., GLP Pte Limited, Keppel DC REIT Management Pte. Ltd and Princeton Digital Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 China

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Hotspot

- 6.1.1 Beijing

- 6.1.2 Guangdong

- 6.1.3 Hebei

- 6.1.4 Jiangsu

- 6.1.5 Shanghai

- 6.1.6 Rest of China

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 BDx Data Center Pte. Ltd

- 7.3.2 Chayora Ltd

- 7.3.3 China Telecom Corporation Ltd

- 7.3.4 Chindata Group Holdings Ltd

- 7.3.5 Equinix Inc.

- 7.3.6 GDS Service Co. Ltd

- 7.3.7 GLP Pte Limited

- 7.3.8 Keppel DC REIT Management Pte. Ltd

- 7.3.9 Princeton Digital Group

- 7.3.10 Space DC Pte Ltd

- 7.3.11 Telehouse (KDDI Corporation)

- 7.3.12 Zenlayer Inc.

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 196 Pages

- 納期

- 2~3営業日