|

市場調査レポート

商品コード

1910906

中東のデータセンター:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Middle East Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東のデータセンター:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

概要

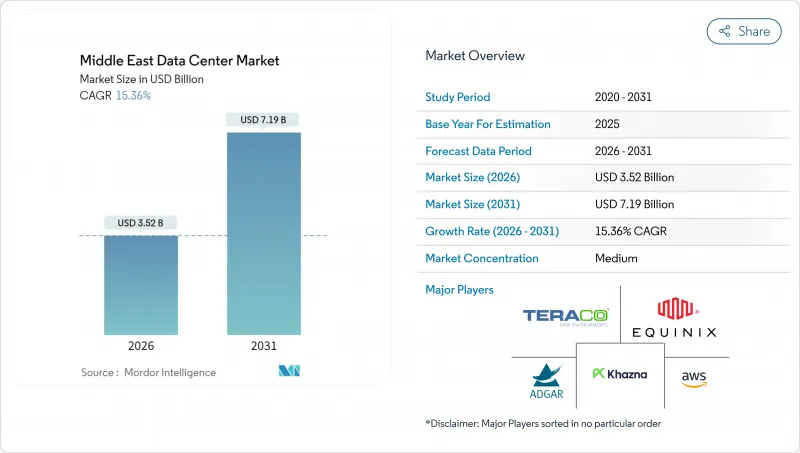

中東のデータセンター市場は、2025年の30億5,000万米ドルから2026年には35億2,000万米ドルへ成長し、2026年から2031年にかけてCAGR 15.36%で推移し、2031年までに71億9,000万米ドルに達すると予測されております。

設置ベースにおいては、市場は2025年の1,820メガワットから2030年までに2,840メガワットへ成長し、2025年から2030年の予測期間においてCAGR9.23%で推移すると見込まれます。市場セグメンテーションのシェアおよび推定値は、MW単位で算出・報告されています。堅調な政府資金、ハイパースケール容量の義務化、高密度海底ケーブルの陸揚げ、クラウド優先の支援的規制が相まって、資本と人材を地域に呼び込み、従来の建設サイクルを短縮し、稼働率を向上させています。サウジアラビアのHUMAINやUAE-フランスAI協定といった国家プログラムはGPU集積型ホールの確実な基幹需要を生み出しており、油田廃ガス発電パイロット事業は構造的に低いエネルギーコストを示唆しています。これにより欧州やアジア地域に対するコスト優位性が拡大する可能性があります。土地・電力供給管理と液体冷却技術のノウハウを組み合わせた事業者は、他地域での容量不足を回避したいハイパースケーラー企業から長期契約を獲得しています。国内の有力企業、世界のコロケーションブランド、エネルギー大手がリヤド、アブダビ、テルアビブでの立地を争う中、競合圧力は高まっており、土地価格を押し上げる一方で、国境を越えたワークロードの移動性を向上させるキャンパス間ファイバーの構築を加速させています。

中東のデータセンター市場の動向と洞察

サウジアラビアとUAEにおける国家クラウドファースト政策の急速な導入

拘束力のあるクラウドファースト指令により、各省庁や国有企業は、通常のコスト最適化を考慮しないスケジュールでワークロードの移行を義務付けられており、開発者を景気循環による減速から保護する需要の底堅さを効果的に創出しています。これらの指令には厳格なデータ主権条項も組み込まれており、プレミアム価格が設定されるソブリンクラウドゾーンの促進につながっています。公共部門の契約獲得にはコンプライアンスが必須であるため、外国のクラウドプロバイダーはライセンシングを受けた現地事業者と提携する必要があり、これにより国内での価値獲得が強化され、現地労働力へのスキル移転が加速しています。

政府支援によるハイパースケール容量目標は2030年までに1.3GWを超える見込み

サウジ・テレコム社の「センター3」のような旗艦プログラムは1GWのロードマップを目標とし、主要テナントの確保を保証するとともに、電力購入特権をバンドルすることが多く、リスクプレミアムを低下させ、開発期間を18~24ヶ月に短縮します。政府主導の資金調達により、オフテイク契約を巡る通常の争奪戦が不要となり、純粋な商業市場では資金調達が困難な複数キャンパス同時立ち上げが可能となります。初期段階における供給過剰は、欧州とアジア間の低遅延冗長性を求める国際的なハイパースケーラーにとって、参入障壁をさらに低減します。

気候変動による冷却運用コストの増加

砂漠の周囲温度は、温帯地域と比較して年間PUEを3~5%押し上げ、GPUラックを仕様範囲内に維持するために、事業者には大規模な冷水プラントの資金調達または液体冷却の採用を迫ります。AIクラスターは熱負荷をさらに悪化させ、水不足規制は蒸発冷却システムの導入を制限するため、新規参入者による価格圧力が高まるまさにそのタイミングで、電気駆動の冷却装置への依存度が高まり、運用コストを押し上げます。

セグメント分析

大規模施設は、企業の継続利用と資産の完全償却により、導入容量の39.62%を占めました。しかしながら、次世代キャンパスが稼働を開始するにつれ、この割合は低下する見込みです。一方、国家主導のAIプログラムや50MWを超える連続電力ブロックを必要とするハイパースケーラー企業に牽引された大規模キャンパスは、セグメント内で最も高い成長率(CAGR16.69%)を記録しました。2026年から2031年にかけて、中東のデータセンター市場はこうした大規模建設により規模が2倍以上に拡大すると予測されます。数百メガワット規模の送電網接続を確保した事業者には、現在優先調達権が付与されています。

この変化はDataVoltのような開発者に有利に働きます。同社がNEOMに建設中の1.5GWネットゼロAI工場は、国家主導の計画が従来のコロケーションにおける段階的拡張ロジックをいかに回避するかを示しています。メガおよび中規模フォーマットは、国別の拠点が必要でありながら大規模なフットプリントの経済性を吸収できない地域クラウドサービスにとって、依然として重要な役割を担っています。小規模なエッジノードは、低遅延が要求される使用事例や規制上の居住条項への対応を継続し、同一地域エコシステム内でハイパースケールとマイクロデプロイメントを融合させるバーベル型の構造を保証します。

2025年時点で中東データセンター市場の67.05%をTier 3施設が占め、マルチテナントアプリケーションにおける信頼性とコスト効率の最適解としての地位を確固たるものにしております。しかしながら、AIトレーニング、デジタル決済の清算処理、国家安全保障ワークロードが耐障害性の基準を引き上げる中、Tier 4は16.55%のCAGRで拡大を続けております。中東のデータセンター市場においてティア4に割り当てられる規模は、重要インフラプロジェクトに対する国家レベルの許可手続きの迅速化を背景に、2020年代末までに3倍に拡大すると予測されています。

地域事業者は長期的な信頼性を示すため、Tier 4導入への意欲を表明しています。エティサラット社の運用持続性におけるティア3ゴールド認証など、アップタイム・インスティテュートの認証は、地政学的リスクの認識を低減する成熟した品質文化を実証しています。しかしながら、ティア3とティア4のMW当たり設備投資額(CAPEX)の差は、価格に敏感なテナントが主流の地方都市では依然として障壁となっています。開発業者は、冗長性のレベルを地域の需要弾力性に調整する必要があり、同一サイト内にティア3とティア4のホールを混在させるケースが少なくありません。

中東データセンター市場レポートは、データセンター規模(大規模、超大規模、中規模、メガ、小規模)、ティア基準(ティア1・2、ティア3、ティア4)、データセンタータイプ(ハイパースケール/自社建設、エンタープライズ/エッジ、コロケーション)、エンドユーザー産業(BFSI、ITおよびITES、Eコマース、政府、メディア・エンターテインメントなど)、地域別に分類されています。市場予測はIT負荷容量(MW)単位で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- サウジアラビアおよびアラブ首長国連邦における国家クラウド優先政策の急速な導入

- 政府が支援するハイパースケール容量目標は、2030年までに1.3ギガワットを超える見込みです。

- 国家主導のAI資金調達の急増(例:1000億米ドル規模のHUMAINプログラム)

- 海底ケーブルの密度化が地域間相互接続性を促進

- 未利用の油田廃ガスをデータセンター電源として再利用

- イスラエルからGCC事業者へのAI最適化液体冷却システムの輸出

- 市場抑制要因

- 気候変動による冷却運用コストの増加

- 認定データセンター技術者の不足

- LNG連動電力料金の変動性

- 保険における地政学的サイバーリスクプレミアム

- テクノロジーの展望

- 市場見通し

- IT負荷容量

- 高床式フロア面積

- コロケーション収益

- 設置済みラック

- ラックスペース利用率

- 海底ケーブル

- 主要な業界動向

- スマートフォン利用者数

- スマートフォン1台あたりのデータトラフィック

- モバイルデータ通信速度

- ブロードバンドデータ通信速度

- 光ファイバー接続ネットワーク

- 規制の枠組み

- サウジアラビア

- アラブ首長国連邦

- イスラエル

- バリューチェーン及び流通チャネル分析

- ファイブフォース分析分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 業界間の競争

第5章 市場規模と成長予測

- データセンター規模別

- 大規模

- 巨大

- 中規模

- メガ

- 小規模

- ティア基準別

- ティア1および2

- ティア3

- ティア4

- データセンタータイプ別

- ハイパースケールまたは自社建設

- エンタープライズまたはエッジ

- コロケーション

- 未稼働

- 稼働

- 小売コロケーション

- ホールセールコロケーション

- エンドユーザー産業別

- BFSI

- ITおよびITES

- 電子商取引

- 政府

- 製造業

- メディアとエンターテイメント

- 通信

- その他のエンドユーザー産業

- 国別

- サウジアラビア

- アラブ首長国連邦

- イスラエル

- その他中東

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Khazna Data Centers LLC

- Digital Realty Trust Inc.

- Teraco Data Environments Proprietary Limited

- Adgar Investments and Development Ltd.

- MedOne Data Centers Ltd.

- Africa Data Centres Ltd.

- Electronia Company Limited

- Gulf Data Hub LLC

- Amazon Web Services Inc.

- Paratus Group Holdings Ltd.

- Etihad Etisalat Company

- Center3 Company

- Emirates Integrated Telecommunications Company PJSC

- Data Hub Integrated Solutions Moro L.L.C(Moro Hub)

- Equinix Inc.