|

市場調査レポート

商品コード

1690142

英国のデータセンター- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)United Kingdom Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のデータセンター- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 194 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

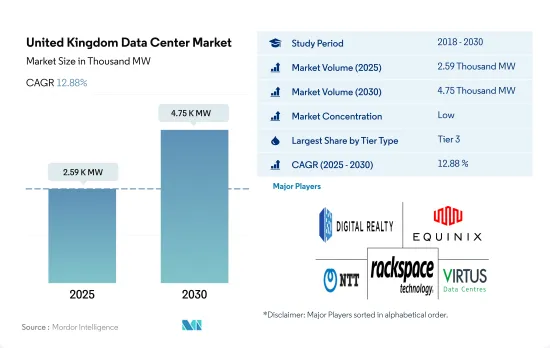

英国のデータセンター市場規模は、2025年に2,590kWと推定され、2030年には4,750kWに達し、CAGR 12.88%で成長すると予測されます。

また、2025年のコロケーション収益は26億6,100万米ドル、2030年には67億9,950万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは20.64%です。

ティア3データセンターは、2023年に数量ベースで大半のシェアを占め、予測期間中もその優位性は続きます。

- ティア3データセンターは、オンサイト支援、電力、冷却の冗長性などの特徴により、最も好まれています。ティア3 DC市場は、2022年には1,540.98MWで稼働していました。予測期間中に予想される容量は、CAGR 10.88%で2023年の1,813.19MWから2029年には3,369.24MWに成長する見込みです。これらのデータセンターは、主要な差別化要因として冗長コンポーネントを備えた「同時保守可能」です。

- 中小企業は一般的に、提供される冗長保護がはるかに優れているため、少なくともティア3ランクのシステムを好んで使用します。英国では、中小企業が企業人口の99.9%を占めています。2022年初頭には、英国の民間セクタには550万社の企業があると推定されています。ティア3施設の主要採用は、BFSI、電気通信、メディアエンターテイメントユーザーがホールセールとハイパースケールコロケーションを主に採用していることに反映されています。2022年現在、国内には約148のティア3データセンターがあり、約28のティア3データセンターが建設中です。

- ティア4は、フォールトトレラント機能、低ダウンタイム、99.99%のアップタイムにより、大企業が次に好むデータセンターです。クラウドや通信セグメントの主要エンドユーザーがハイパースケールコロケーションを採用することで、予測期間中に市場は潜在的な成長を見せると予想されます。英国政府のG-Cloudプログラムは、公共部門による情報通信技術の購入方法を変えつつあります。2022年、同国にはExascale LtdとServerManiaが所有する2つのティア4データセンターがありました。

- Tier1& 2データセンターは、電力と冷却のための単一経路であり、Tier3とTier4施設と比較して99.671%(年間28.8時間のダウンタイム)の予想稼働時間を提供するため、最も好まれません。

英国のデータセンター市場動向

スマートフォン普及率の上昇、4Gと5Gサービスの登場が市場成長を後押し

- 同国のスマートフォンユーザー数は2022年には6,346万人で、予測期間中のCAGRは1.01%で、2029年には6,800万人に達すると予測されます。

- 英国のスマートフォン普及率は年々上昇しており、2022年には全体の93%に達します。16~24歳の年齢層では、2022年のスマートフォン所有率は99%でした。英国のモバイルインターネットユーザー数は6,230万人に達し、この数字は4Gと5Gの出現により約286万人増加し、2026年には6,500万人を超えると予測されています。さらに、COVID-19が流行して以来、人々はスマートフォンの利用を増やし、オンラインゲームやメディアストリーミングプラットフォームにより多くの時間を費やすようになりました。その結果、2020年4月、産業はオンライン決済を支援するため、個人の非接触カード決済の利用限度額を30英ポンドから45英ポンドに引き上げました。このようなシナリオはスマートフォンの普及率を高め、現在も同じ傾向にあります。

- ユーザー数の増加は、データセンター市場の需要を押し上げました。この増加率は、大量のデータが生成されるeコマース、メディア娯楽、BFSIセグメントでの成長を支えています。スマートフォンは大量のデータをリアルタイムで処理する必要があるため、ストレージ用のデータセンターが必要となります。スマートフォンの普及率が2017年の72%から2022年には90%以上に増加した過去の期間中、データセンターのラック数は2017年の約21万5,000から2022年には38万8,000に増加しました。この動向は予測期間中もさらに見られると予想されます。

2G、3Gの段階的廃止と4G、5Gネットワークの採用、モバイル機器の利用増加が市場成長を牽引

- 英国初の5Gネットワークは2019年5月に稼働し、4Gは2012年10月に開始されました。稼働以来、両ネットワークともデータ通信速度の向上を示しています。4Gの通信速度は2012年の12Mbpsから2022年には36.40Mbpsに向上しました。同様に、5Gの速度は2019年の139.5 Mbpsから2022年には160.15 Mbpsに増加しました。2022年5月の産業調査によると、英国(英国)では回答者の約67%がスマートフォンで4Gサービスを利用しており、約25%が5Gサービスを利用していました。

- 英国は2033年までに2Gと3Gのモバイルサービスを段階的に廃止します。すべての通信事業者にとっての主要戦略は、2Gと3Gのネットワークを停止し、5Gを展開しながら4Gの顧客体験をさらに向上させることに投資と周波数リソースを集中させることです。英国政府は、1億1,000万英ポンド(1億3,500万米ドル)相当の投資を支援し、5Gと6Gの開発促進に投資する意向を示しています。さらに、2Gと3Gの切替日は、モバイルネットワーク事業者のVodafone、EE、Virgin Media、O2、Threeと合意しています。

- 高速化と全体的な接続性の向上は、他のエンドユーザー産業にも道を開いています。2021年、英国のユーザーは1日平均4時間モバイル機器を使用しました。これは2020年から0.3時間の増加です。2022年初頭の英国のソーシャルメディアユーザー数は全人口の84.3%に相当し、2021~2022年の間に460万人増加しました。全体として、これはモバイルデータの速度を増加させ、データトラフィックを増加させ、それによってデータを格納し、処理するためのデータセンターが必要になります。

英国データセンター産業概要

英国のデータセンター市場は細分化されており、上位5社で34.50%を占めています。この市場の主要企業は、Digital Realty Trust Inc.、Equinix Inc.、NTT Ltd、Rackspace Technology Inc.、Virtus Data Centres Properties Ltd(STT GDC)です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 市場展望

- 耐荷重

- 床面積

- コロケーション収入

- 設置ラック数

- ラックスペース利用率

- 海底ケーブル

第5章 主要産業動向

- スマートフォンユーザー数

- スマートフォン1台当たりのデータトラフィック

- モバイルデータ速度

- ブロードバンドデータ速度

- 光ファイバー接続ネットワーク

- 規制の枠組み

- 英国

- バリューチェーンと流通チャネル分析

第6章 市場セグメンテーション

- ホットスポット

- ロンドン

- その他の中東・アフリカ

- データセンターの規模

- 大規模

- 超大規模

- 中規模

- 極超大規模

- 小規模

- ティアタイプ

- ティア1と2

- ティア3

- ティア4

- 吸収量

- 非利用

- 利用

- コロケーションタイプ別

- ハイパースケール

- リテール

- ホールセール

- エンドユーザー別

- BFSI

- クラウド

- eコマース

- 政府機関

- 製造業

- メディア&エンターテイメント

- テレコム

- その他

第7章 競合情勢

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Colt Technology Services

- CyrusOne Inc.

- Digital Realty Trust Inc.

- Equinix Inc.

- Global Switch Holdings Limited

- Global Technical Realty SARL

- Kao Data Ltd

- NTT Ltd

- Rackspace Technology Inc.

- Telehouse(KDDI Corporation)

- Vantage Data Centers LLC

- Virtus Data Centres Properties Ltd(STT GDC)

第8章 CEOへの主要戦略的質問

第9章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

The United Kingdom Data Center Market size is estimated at 2.59 thousand MW in 2025, and is expected to reach 4.75 thousand MW by 2030, growing at a CAGR of 12.88%. Further, the market is expected to generate colocation revenue of USD 2,661 Million in 2025 and is projected to reach USD 6,799.5 Million by 2030, growing at a CAGR of 20.64% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, it will continue its dominance during forecast period

- Tier 3 data centers are the most preferred due to features such as onsite assistance, power, and cooling redundancy. The Tier 3 DC market was operating at 1540.98 MW in 2022. The expected capacity during the forecast period is expected to grow from 1813.19 MW in 2023 to 3369.24 MW in 2029 at a CAGR of 10.88%. These data centers are 'concurrently maintainable' with redundant components as a key differentiator.

- SMBs generally prefer to use at least a tier III-rated system for the far superior redundancy protections offered. In the United Kingdom, SMEs account for 99.9% of the business population. At the start of 2022, there were estimated to be 5.5 million businesses in the UK private sector. Major adoption of tier 3 facilities is reflected in BFSI, telecom, and media and entertainment users are majorly adopting wholesale and hyperscale colocation. As of 2022, there are around 148 Tier 3 data centers in the country, and around 28 upcoming data centers are under construction with Tier 3 standards.

- Tier 4 is the next most preferred data centers by large enterprises due to their fault-tolerant functionality, lower downtime, and 99.99% uptime. It is expected that the market will showcase potential growth during the forecast period with the adoption of hyperscale colocation by major end users in the cloud and telecom sectors. The UK government's G-Cloud program is changing the way public sector organizations purchase information and communications technology. In 2022, the country had two Tier 4 data centers owned by Exascale Ltd and ServerMania.

- The Tier 1&2 data centers are the least preferred due to their single path for power and cooling and providing expected uptime of 99.671% (28.8 hours of downtime annually) when compared to Tier 3 and Tier 4 facilities.

United Kingdom Data Center Market Trends

Increase smartphone penetration rate, emergence of 4G and 5G services to boost market growth

- The number of smartphone users in the country was 63.46 million in 2022 and is expected to witness a CAGR of 1.01% during the forecast period to reach a value of 68 million by 2029.

- The smartphone penetration rate in the United Kingdom has increased each year, reaching an overall figure of 93% in 2022. Among the age group of 16-24, the smartphone ownership rate was 99% in 2022. The number of mobile internet users in the United Kingdom reached 62.3 million, a figure which is projected to increase by approximately 2.86 million and amount to over 65 million by 2026 with the emergence of 4G and 5G. Further, since the COVID-19 pandemic hit, people have increased their smartphone usage and spent more time on online gaming or media streaming platforms. As a result, in April 2020, the industry increased the spending limit on individual contactless card payments from GBP 30 to GBP 45 to help with online payments. Such a scenario has increased smartphone penetration and is currently following the same trend.

- The growth of the user base positively boosted the market demand for data centers. The increasing rate has positively upheld its growth in the e-commerce, media and entertainment, and BFSI sectors, where a large chunk of data has been generated. Since smartphones necessitate real-time processing on having a large data chunk, they mostly require a data center for storage. During the historical period, when smartphone usage penetration increased from 72% in 2017 to more than 90% in 2022, the number of racks in the data center increased from around 215k in 2017 to 388k in 2022. This trend is further expected to be witnessed during the forecast period.

Phase out of 2G and 3G and adoption of 4G and 5G network and increase in use of mobile devices to drive market growth

- The United Kingdom's first 5G network was activated in May 2019, and 4G was launched in October 2012. Since being commissioned, both networks have shown an increment in their data speed. 4G speed increased from 12 Mbps in 2012 to 36.40 Mbps in 2022. Similarly, 5G speed increased from 139.5 Mbps in 2019 to 160.15 Mbps in 2022. In May 2022, according to an industry survey, around 67% of respondents in the United Kingdom (UK) had a 4G service on their smartphone, while about 25% had a 5G service.

- The UK will phase out 2G and 3G mobile services by 2033. The major strategy for all the operators is to turn off their 2G and 3G networks, allowing them to focus investments and spectrum resources on further improving the 4G customer experience while rolling out 5G. The UK government has outlined its intentions to invest in driving 5G and 6G development with the support of GBP 110 million (USD 135 million) worth of investment. Moreover, the switch-off date for 2G and 3G has been agreed upon with mobile-network operators Vodafone, EE, Virgin Media, O2, and Three.

- The growth in speed and better overall connectivity is paving the way for other end-user industries. In 2021, users in the United Kingdom spent an average of four hours per day using their mobile devices. This was an increase of 0.3 hours up from 2020. The number of social media users in the United Kingdom at the start of 2022 was equivalent to 84.3% of the total population, and it increased by 4.6 million between 2021 and 2022. Overall, this will increase the mobile data speed, increasing the data traffic, which thereby requires data centers for storing and processing data.

United Kingdom Data Center Industry Overview

The United Kingdom Data Center Market is fragmented, with the top five companies occupying 34.50%. The major players in this market are Digital Realty Trust Inc., Equinix Inc., NTT Ltd, Rackspace Technology Inc. and Virtus Data Centres Properties Ltd (STT GDC) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 United Kingdom

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Hotspot

- 6.1.1 London

- 6.1.2 Rest of United Kingdom

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 Colt Technology Services

- 7.3.2 CyrusOne Inc.

- 7.3.3 Digital Realty Trust Inc.

- 7.3.4 Equinix Inc.

- 7.3.5 Global Switch Holdings Limited

- 7.3.6 Global Technical Realty SARL

- 7.3.7 Kao Data Ltd

- 7.3.8 NTT Ltd

- 7.3.9 Rackspace Technology Inc.

- 7.3.10 Telehouse (KDDI Corporation)

- 7.3.11 Vantage Data Centers LLC

- 7.3.12 Virtus Data Centres Properties Ltd (STT GDC)

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms