|

|

市場調査レポート

商品コード

1690138

アジア太平洋地域のガス検知器:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia Pacific Gas Detector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のガス検知器:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

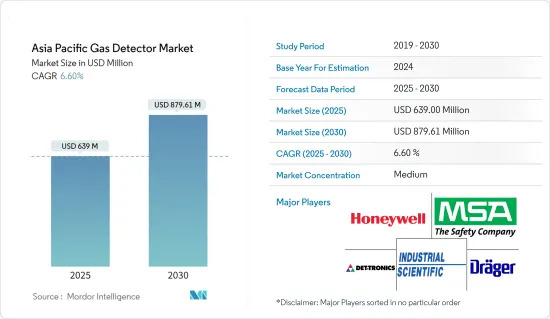

アジア太平洋地域のガス検知器市場規模は2025年に6億3,900万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.6%で、2030年には8億7,961万米ドルに達すると予測されます。

重要な成長指標は、この地域における急速な都市化であり、そのために温室効果ガスの排出量が激増し、ガス検知装置の配備が必要となっています。

主なハイライト

- ハンドヘルド機器の普及がガス検知器分野の開発につながり、複数のエンドユーザー・セグメントで応用範囲が大幅に広がりました。政府の排出規制や労働安全規制はますます厳しくなっており、ガス検知器の需要を牽引しています。

- インドネシアのPertaminaやPTTEPなどの石油会社は国内供給の維持に成功しており、エネルギー会社のポートフォリオを拡大する投資家を引き付けています。こうした取り組みにより、ガス検知器の需要拡大が期待されます。シンガポールは石油化学産業のハブとして脚光を浴びています。その背景には、BASF、ランクセス、三井化学、シェルなど、この業界の世界的大手企業による投資があります。また、二酸化炭素排出量削減への取り組みも推進されています。

- ワイヤレスガス検知は、これまで手が届きにくかったり監視コストが高かったりした場所へのガス検知器の配備を加速しています。このため、新興国市場のベンダーはワイヤレス・ソリューションの開発と提供にますます力を入れています。

- しかし、爆発の危険性がある産業や現場では、有線ガス検知器の需要が突出しています。石油・ガス、化学、石油化学産業で顕著な既存の検知器は、大きな需要が見込まれます。配線ガス検知器は、より高い成長とワイヤレス検知器の必要性により、顕著な市場シェアを占めると予想されます。

- また、検出器の機能開発と小型化は、通信機能の向上と相まって、安全な距離で有毒ガスや可燃性ガスの検出を損なうことなく、様々なデバイスや機械にIoTセンサーを統合することを可能にします。

- ガス検知器の製造コストは、インテリジェント・コンポーネントの使用をもたらす最近の技術的変化により、着実に上昇しています。そのため、鉱業、建設などの主要エンドユーザー産業における顧客の支出がわずかに減少し、市場に悪影響を及ぼすと予想されます。

- COVID-19は市場成長にマイナスの影響を与えています。これは、世界の工場や工業施設の閉鎖により、飲食品セクターを除いてガス検知器の使用量が減少しているためです。この業界では、ガス検知器がより多く使用されています。

アジア太平洋地域のガス検知器市場動向

石油・ガスが著しい成長を記録する

- 石油・ガス市場は、ガス検知器の使用を奨励する政府のイニシアティブにより、この地域で最も急速に成長しています。エネルギー需要の増加に伴い、この地域は、各経済圏の国内要件を満たすエネルギー資源の供給を確保する上で、より大きな課題に直面しています。

- 石油・ガスセクターにおけるアジア太平洋地域のガス検知器市場は、プラントの安全性に対する需要の膨大な増加により、将来的に成長することが期待されています。有害ガスの存在を検知するガスモニタリングアメニティに対する需要の高まりは、特に産業セグメントにおいて一定のガス検知器市場の成長を促進すると予想されます。

- 石油・ガス産業におけるIoTの導入は、優れたフィールド通信、リアルタイムのモニタリング、デジタル油田インフラ、メンテナンスコストの凝縮、電力消費の削減、生産性の向上を実現し、その結果、資産と労働力の安全性とセキュリティが高まっています。例えば、ガスの浪費は、対策が必要な重要な問題です。LPGガスは引火性が高く、生命や財産に危害を及ぼす可能性があります。IoTと組み合わされたガス検知器は、ガス検知において重要な役割を果たし、ガスの浪費を阻止することができるため、市場の成長に拍車をかける。

- さらに、この地域の企業は、市場におけるガス検知製品の差別化を提案するために、先進技術の導入に注力しています。例えば、ファーウェイのeLTEガス検知ソリューションは、IoTシナリオに効率的なパフォーマンスを提供し、必要なデバイスの数を減らし、それに伴って管理やメンテナンスの労力も軽減します。

- さらに、世界のエネルギー需要は2013年から2030年にかけて、特にインドや中国のような発展途上国で約40%増加すると予想されています。IEA(国際エネルギー機関)の報告によると、これらの国々では石油・ガスの需要がそれぞれ50%、20%増加すると予測されています。さらに、インドや中国のような国々(それぞれアラビア海やジュガール盆地)で石油埋蔵量が発見され、探査プロセスへの投資が予定されていることから、ガス検知器のニーズが高まることが予想されます。

- さらに、この地域では安全を確保するためのイニシアチブがいくつか実施されています。APEC石油・ガス安全保障イニシアティブ(OGSI)は、エネルギー供給安全保障の問題に取り組むエコノミーを支援し、潜在的な供給不足と緊急事態に対処するために設立されました。OGSIには、石油・ガス安全保障演習(OGSE)、石油・ガス安全保障研究(OGSS)、石油・ガス安全保障ネットワーク(OGSN)という3つの重要な柱があります。したがって、ガス検知器はこれらの分野で最も重要です。

- さらに、ガス検知器の需要を増大させる地域プロジェクトがいくつか進行中です。その中には、シラチャ製油所の拡張とアップグレード(タイで2024年開始予定)、Pulau Muara Besar Refinery &Petrochemical Complex Phase 2(中国で2022年開始予定)などがあります。

固定式ガス検知器が大きな市場シェアを占める

- 固定式ガス検知器は、24時間体制で監視する必要がある場合に設置されます。有毒ガスへの暴露、酸素不足による窒息、可燃性ガスによる爆発などの潜在的な危険を作業員に知らせるよう設計されています。これらのガス検知器は、危険なガスが蓄積する密閉されたまたは部分的に密閉された空間で使用されます。

- 有毒ガス検知器は、石油・ガス、鉱業、原子力、医療、飲食品、建設、工業などの産業で広く使用されています。金属酸化物ベースのガスセンサーは、有毒ガスの検知に最も一般的に使用される検知器のひとつです。これらのセンサーは、一酸化炭素、水素、メタン、ブタンなどのガスに接触することで電気抵抗が増加します。ほとんどの家庭用煙検知システムは酸化物ベースのセンサーです。

- 固定タイプ別の可燃性ガス検知器は、ガス検知器市場で大きなシェアを占めています。これらのセンサーは可燃性ガスや蒸気を検知・反応させるもので、主に産業プラントでガス漏れや蓄積が爆発レベルに達する前に検知するために使用されます。

- これらの検知器は、赤外線、電気化学、超音波、または半導体などのセンサーを通して、指定された領域内の特定のガスの濃度を測定し、基準点またはスケールと比較します。センサーの反応があらかじめ設定されたレベルを超えると、アラーム、光、または信号の組み合わせによってユーザーに警告が発せられます。

- さらに、企業は固定式ガス検知器に高度な技術を取り入れることで、製品の革新に継続的に投資しています。これらの検知器は現在、複数のガスをモニターするために開発されています。例えば、テレダイン社のOLC 10およびOLCT 10ガスセンサーは、第三次アプリケーション(ボイラー工場、バッテリー充電室、駐車場、病院)用の可燃性ガスまたは有毒ガスを検出するように設計されています。2台のOLC 10を1つの検出チャンネルに接続することで、ジャンクションボックスや配線を追加することなく、同じエリアを監視することができます。

- 例えば、2021年7月、イオンサイエンスはCub 11.7 eVパーソナルデバイスを発売しました。この有毒ガス検知ソリューションは、0 °C~55 °Cの温度で作動し、湿度や水分の影響を受けにくいです。このガス検知器は重さわずか111グラムで、快適に装着でき、そのコンパクトなサイズにより、作業員は煩わしい機器に邪魔されずに動き回ることができ、バッテリー寿命は最大12時間です。

- さらに、アジア太平洋地域には多くの産業が存在し、これらの検出器の需要が増加している重要な市場です。需要の高まりと安定した収益性により、複数のベンダーが市場に参入しています。例えば、2021年2月、ガス検知センサー技術ベンダーのNevadaNano Inc.は、エレマテック株式会社が同社の分子特性分光計を日本全国の顧客ベースに販売すると発表しました。

- さらに、これらの検出器は石油・ガス産業でも使用されています。天然ガスや原油は地下深くにあり、岩石層に隠れていて、アクセスが難しく、極端な気候の場所で発見されます。そのため、センサー機能の進歩と計算能力の向上が、これらの検知器の需要を促進しています。

アジア太平洋地域のガス検知器産業概要

アジア太平洋地域のガス検知器市場の競争は中程度で、複数の大手企業で構成されています。同市場で大きなシェアを持つ大手企業は、アジア太平洋地域の国々にまたがる顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために戦略的な共同イニシアティブを活用しています。

- 2022年4月-MSA Safety Incorporatedは、業界のゲームチェンジャーとなる最新のガス検知ウェアラブル機器ALTAIR io 4の発売を発表しました。これはMSA初のダイレクト・ツー・クラウド型ガス検知器です。同社の新しい安全サブスクリプションサービス「MSA+」と連動するように設計されたALTAIR io 4デバイスは、MSAが「コネクテッド・ワーク・プラットフォーム」と呼ぶクラウド対応技術スイートのハードウェア部分に相当します。

- 2021年10月-ハネウェル・インターナショナルは、2つの先進的なBluetooth接続ガス検知器、サーチライン・エクセル・プラスとサーチライン・エクセル・エッジを発表しました。石油・ガス、化学、石油化学、その他の産業施設向けに設計された同社の最新のガス検知器は、雨、霧、雪、その他の厳しい気象条件下での危険ガスや可燃性ガスの漏れの常時監視を容易にします。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 労働者の安全に対する意識の高まりと厳しい規制

- アジア太平洋の主要新興国における工業セクターの着実な増加と拡張プロジェクト

- 市場の課題

- 最近の業界別COVID-19の発生と主要業種における支出のわずかな減少がメーカーに懸念をもたらす見込み

- 流通チャネル分析

- 主な業界標準と規制

- 使用される通信の種類有線対無線

第6章 市場セグメンテーション

- タイプ別

- 固定式

- 有毒ガス検知器

- 可燃性ガス検知器

- ポータブル

- シングルガス

- マルチガス

- 固定式

- 業界別

- 石油・ガス

- 化学・石油化学

- 上下水道

- 発電

- 金属・鉱業

- 飲食品

- その他業界別(建設、製薬など)

- 国別

- 中国

- 日本

- インド&韓国

- オーストラリア&ニュージーランド

- 東南アジア(シンガポール、マレーシア、タイ、インドネシア、フィリピン、ベトナム)

第7章 競合情勢

- ベンダーランキング分析(主要差別化パラメータに基づくベンダーのランキング)

- 企業プロファイル

- Honeywell Analytics Inc.

- MSA Safety Incorporated

- Draegerwerk AG & Co. KGaA

- Industrial Scientific Corporation

- Det-Tronics(a Carrier Company)

- Teledyne Technologies Incorporated

- Crowncon Detection Instruments Limited

- RKI Instruments Inc.

- GFG Gesellscharft

第8章 投資分析

第9章 市場機会と今後の動向

The Asia Pacific Gas Detector Market size is estimated at USD 639.00 million in 2025, and is expected to reach USD 879.61 million by 2030, at a CAGR of 6.6% during the forecast period (2025-2030).

An important growth indicator is rapid urbanization in the region, due to which greenhouse gas emissions have increased tremendously, necessitating the deployment of gas detecting devices.

Key Highlights

- The proliferation of handheld devices has led to developments in the field of gas detectors, which has considerably widened the scope of application across multiple end-user segments. Government regulations are increasingly becoming stringent in emission control and labor safety, driving the demand for gas detectors.

- Oil companies, such as Indonesia's Pertamina and PTTEP, are successfully maintaining domestic supply, attracting investors to expand the energy company's portfolio. These efforts are expected to increase the demand for gas detectors. Singapore is being highlighted as the hub for the petrochemical industry. This is because of the investments by the major global players in this industry, such as BASF, Lanxess, Mitsui Chemicals, and Shell. It has also been promoting initiatives for the reduction of carbon emissions.

- Wireless gas detection is helping accelerate the sheer number of deployments of gas detectors in previously inaccessible areas, which are too difficult to reach or costly for monitoring. Owing to this, the vendors in the market are increasingly focusing on developing and offering wireless solutions.

- However, wired gas detectors hold prominence in demand in industries and sites that run the risk of explosion. The existing detectors in places pretty evident in the oil and gas, chemicals, and petrochemical industries are expected to command significant demand. Wiring gas detectors are expected to cost a prominent market share, with higher growth and the need for wireless detectors.

- Also, the development of detector capabilities and miniaturization, coupled with improved communication capabilities, enables the integration of IoT sensors into various devices and machines without compromising the detection of toxic or flammable gases at safe distances.

- The cost of production for gas detectors has been steadily rising due to recent technological changes resulting in the use of intelligent components. Thus, this is expected to negatively impact the market due to the Marginal decrease in spending of customers in Key End-User Verticals such as Mining, Construction, and many more.

- COVID-19 has negatively impacted the market growth. This is because of the global lockdown of factories and industrial facilities, which has caused a declining usage of gas detector devices, except in the food and beverage sector. In this industry, gas detectors are being used more since the sector comes under essential services and works round the clock.

APAC Gas Detector Market Trends

Oil & Gas to Register Significant Growth

- The oil and gas market is the fastest in the region due to government initiatives encouraging the use of gas detectors. With the growing energy demand, the region is facing more significant challenges in securing the supply of energy resources to meet the domestic requirements of each economy.

- The Asia Pacific gas detectors market in the oil and gas sector is expected to grow in the future, owing to the enormous rise in demand for plant safety. The growing demand for gas monitoring amenities to detect the presence of harmful gases is expected to drive constant gas detector market growth, particularly in the industrial segment.

- The deployment of IoT in the oil and gas industry has realized superior field communication, real-time monitoring, digital oil field infrastructure, condensed cost of maintenance, reduced power consumption, higher productivity, and, thus, heightened safety and security of assets and workforce. For instance, gas wastage is a crucial issue that needs to be countered. LPG gas is highly flammable and can inflict harm to life and property. Gas detectors, coupled with IoT, can play a substantial role in gas detection and block the wastage of gases, thus fueling the market's growth.

- Furthermore, the businesses in the region are focusing on incorporating advanced technologies for proposing gas detecting product differentiation in the market. For instance, Huawei eLTE Gas Detection Solution provides efficient performance for IoT scenarios, requiring fewer devices, with correspondingly fewer management and maintenance efforts.

- Moreover, global energy needs are anticipated to increase by around 40% between 2013 and 2030, particularly in developing nations like India and China. The IEA (International Energy Agency) reported that the demand for oil and gas is projected to increase by 50% and 20% in those countries, respectively. Moreover, the discovery of oil reserves in countries like India and China (the Arabian Sea and Juggar Basin, respectively) and upcoming investments in exploration processes are expected to drive the need for gas detectors.

- Further, several initiatives are being implemented in the region to ensure safety. The APEC Oil and Gas Security Initiative (OGSI) was established to assist economies in tackling the issue of energy supply security and how to deal with potential supply shortages and emergencies. It has three critical pillars - Oil and Gas Security Exercise (OGSE), Oil and Gas Security Studies (OGSS), and Oil and Gas Security Network (OGSN). Thus, gas detectors are of paramount importance in these areas.

- Additionally, several regional projects are underway, which would increase the demand for gas detectors. Some of these include Sriracha Refinery Expansion & Upgrade (To be started in 2024 in Thailand), Pulau Muara Besar Refinery & Petrochemical Complex Phase 2 (To be started in 2022 in China), etc.

Fixed Gas Detectors to Hold Significant Market Share

- Fixed gas detectors are installed when there is a need for round-the-clock monitoring. They are designed to alert workers of the potential danger of toxic gas exposure, asphyxiation due to lack of oxygen, or explosion caused by combustible gases. These gas detectors are used in an enclosed or partially enclosed space where hazardous gases accumulate.

- Toxic gas detectors are widely used by industries including gas and oil, mining, nuclear, medical, food and beverage, construction, and industrial. A metal oxide-based gas sensor is one of the most commonly used detectors for detecting toxic gases. These sensors increase their electrical resistance by contacting gasses such as carbon monoxide, hydrogen, methane, and butane. Most home-based smoke detection systems are oxide-based sensors.

- Combustible gas detectors by Fixed type hold a significant share in the gas detectors market. These sensors detect and respond to combustible gases or vapors and are primarily used in industrial plants to detect gas leakage or buildup before it can reach an explosive level.

- These detectors measure the concentration of certain gases in a specified area through sensors such as infrared, electrochemical, ultrasonic, or semiconductor and compare that to a reference point or scale. If a sensor's response surpasses the pre-set level, an alarm, light, or combination of signals warns the user.

- Additionally, companies continuously invest in product innovation by incorporating advanced technologies in fixed gas detectors. These detectors are now being developed to monitor multiple gases. For instance, Teledyne's OLC 10 and OLCT 10 gas sensors are designed to detect combustible or toxic gases for tertiary applications (boiler plants, battery charging rooms, car parks, and hospitals). Two OLC 10's can be connected to one detection channel to monitor the same area without an additional junction box or wiring.

- For instance, in July 2021, ION Science launched Cub 11.7 eV personal device. This toxic gas detection solution operates in temperatures between 0 °C to 55 °C and is resistant to the effects of humidity or moisture. This gas detector weighs in at a mere 111 grams, so it is comfortable to wear; its compact size enables workers to move around unfettered by cumbersome equipment and has a battery life of up to 12 hours.

- Moreover, The presence of many industries in the APAC region is a crucial market wherein the demand for these detectors is increasing. The rising demand and stable profitability are attracting several vendors to enter the market. For instance, in February 2021, NevadaNano Inc., a gas detection sensor technology vendor, announced that Elematec Corporation would distribute its Molecular Property Spectrometer to its customer base throughout Japan.

- Furthermore, these detectors are also used in the oil & gas industry. Natural gas and crude oil are located deep underground, concealed in rock layers, are difficult to access, and are found in places with extreme climates. Thus, advancements in sensor capability coupled with increasing computing power are driving the demand for these detectors.

APAC Gas Detector Industry Overview

The Asia Pacific Gas Detectors Market is moderately competitive and consists of several major players. Major players with a prominent share in the market are focusing on expanding their customer base across the countries in the APAC region. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

- April 2022 - MSA Safety Incorporated announced the availability of its latest industry game-changer - the ALTAIR io 4 Gas Detection Wearable device. This is MSA's first direct-to-cloud gas detector to feature. Designed to work in concert with the company's new MSA+ safety subscription service, the ALTAIR io 4 device represents the hardware portion of a cloud-ready suite of technology that MSA calls the Connected Work Platform.

- October 2021 - Honeywell International Inc. introduced two advanced Bluetooth-connected gas detectors - Searchline Excel Plus and Searchline Excel Edge. Designed for oil and gas, chemical, petrochemical, and other industrial facilities, the company's latest gas detectors facilitate constant monitoring of hazardous and flammable gas leaks in the rain, fog, snow, and other severe weather conditions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Assessment of COVID-19 impact on the industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Awareness on Worker Safety and Stringent Regulations

- 5.1.2 Steady Increase in the Industrial Sector in Key Emerging Countries in Asia-Pacific, Coupled with Expansion Projects

- 5.2 Market Challenges

- 5.2.1 Recent Outbreak of COVID-19 and Marginal Decline in Spending in Key Verticals Expected to Pose a Concern to Manufacturers

- 5.3 Distribution Channel Analysis

- 5.4 Key Industry Standards and Regulations

- 5.5 Type of Communications Used Wired Vs. Wireless

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Fixed

- 6.1.1.1 Toxic Gas Detectors

- 6.1.1.2 Combustible Gas Detectors

- 6.1.2 Portable

- 6.1.2.1 Single-gas

- 6.1.2.2 Multi-gas

- 6.1.1 Fixed

- 6.2 By End-user Verticals

- 6.2.1 Oil and Gas

- 6.2.2 Chemical and Petrochemical

- 6.2.3 Water and Wastewater

- 6.2.4 Power Generation

- 6.2.5 Metals and Mining

- 6.2.6 Food and Beverage

- 6.2.7 Other End-user Verticals (Construction, Pharmaceuticals, etc.)

- 6.3 By Country

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 India & South Korea

- 6.3.4 Australia & New Zealand

- 6.3.5 Southeast Asia (Singapore, Malaysia, Thailand, Indonesia, Philippines, and Vietnam)

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Ranking Analysis (Ranking of Vendors based on Key Differentiating Parameters)

- 7.2 Company Profiles

- 7.2.1 Honeywell Analytics Inc.

- 7.2.2 MSA Safety Incorporated

- 7.2.3 Draegerwerk AG & Co. KGaA

- 7.2.4 Industrial Scientific Corporation

- 7.2.5 Det-Tronics (a Carrier Company)

- 7.2.6 Teledyne Technologies Incorporated

- 7.2.7 Crowncon Detection Instruments Limited

- 7.2.8 RKI Instruments Inc.

- 7.2.9 GFG Gesellscharft