|

市場調査レポート

商品コード

1690079

自動3Dプリンティング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Automated 3D Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動3Dプリンティング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

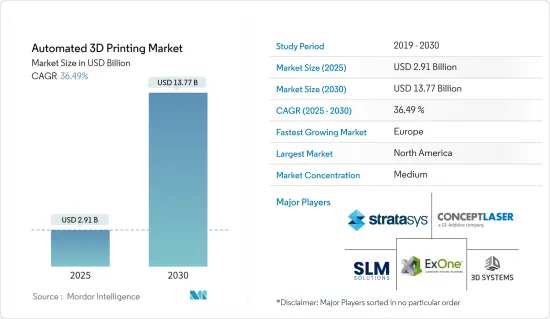

自動3Dプリンティング市場規模は、2025年に29億1,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは36.49%で、2030年には137億7,000万米ドルに達すると予測されています。

研究開発への投資の増加と産業オートメーションへのロボット導入の増加が市場成長を促進すると予測されます。

主なハイライト

- ここ数年、3Dプリンティングは、プロトタイピングや小ロットの段階から大量生産技術へのシフトを絶えず経験しており、産業界や非プリンターベンダーは自動化に重点を移しています。また、アディティブ・マニュファクチャリングの進化傾向に伴い、ハードウェアは、プロトタイピング、ツーリング、単一部品生産に使用されるスタンドアロン・システムから、統合されたデジタル大量生産ライン内のコア・システムとして使用されるように成長しており、新興の消灯工場における機会数を押し上げています。

- 人工知能と機械学習技術は、積層造形業界におけるさまざまな応用を通じてその活路を見いだしつつあります。例えば、マサチューセッツ工科大学(MIT)の研究者は、機械学習のデータ駆動型の性質を応用して、新しい3Dプリント材料を発見するプロセスを自動化しました。機械学習により、靭性や圧縮強度などの材料性能因子がアルゴリズムを用いて最適化され、従来の3Dプリンティング材料配合の方法を素早く凌駕しました。研究開発は、AutoOEDと呼ばれる無料のオープンソース材料最適化プラットフォームを開発し、他の研究者が材料の最適化を実施できるようにしました。

- 同様に、2022年1月には、ドイツとカナダの組織グループが、3DプリンティングとAIを利用して部品の固定プロセスを自動化する新たな共同研究を開始しました。Artificial Intelligence Enhancement of Process Sensing for Adaptive Laser Additive Manufacturing(AI-SLAM)プロジェクトは、指向性エネルギー堆積法(DED)3Dプリンターを自動運転できる強力なAIベースのソフトウェアを作成することを目的としています。損傷した部品の表面の凹凸をよりうまく修復するため、このソフトウェアは印刷プロセスをアルゴリズムで制御します。フラウンホーファー・レーザー技術研究所(ILT)とソフトウェア会社BCTは、ドイツのコンソーシアムの一員です。カナダでは、この研究はカナダ国家研究会議(NRC)が監督します。マギル大学が調査を調整し、機械学習企業のBraintoyがAIモデルのプログラミングを支援します。

- さらに、市場における地位を高めるために、プレーヤーによるさまざまな市場開拓が行われています。例えば、モザイクは2021年4月、自動3Dプリンティング・プラットフォーム「Array」を発表しました。このプラットフォームは、4台のElement HTプリンターに材料をロード・アンロードし、プリントを開始し、プリントを取り除き、次のプリントを開始できるように保管します。Arrayは自動販売機スタイルのロボットアームで最大限の柔軟性を持つように設計されており、プリントを取り外し、横に置き、次のプリントのためにクリーンなベッドをロードすることで、最大限の出力を確保します。

- 2021年10月、バンクーバーを拠点とする3Dプリンティング業界向け自動化技術の開発企業である3DQueは、Creality CR-10およびCR-6 SE用の2つの新しいQuinly自動化キットの発売を発表しました。Quinlyは、Raspberry Piが提供する仮想3Dプリンターオペレーターで、デスクトップ3Dプリンターを単独で稼働させることができるハードウェアとソフトウェアのキットです。この技術は、方程式から手作業を取り除くことによって、3Dプリントをよりスケーラブルにするように設計されています。主に、プリントラボ、オンデマンド製造業者、教育機関、その他自動化された大量部品生産を求めるあらゆる人を対象としています。

- さらに、サプライチェーンの混乱と治療や材料に対する新たな需要により、COVID-19の大流行は、医薬品、医療機器、製造分野の技術進歩を大幅に加速させました。サプライ・チェーンの不足により、医療従事者が必要な物資を入手することが難しくなり、病院ではウイルスを撃退するための個人防護具(PPE)や医療機器が不足しています。このため、付加製造(AM)(自動3Dプリンティング)は、複雑なモノリシック部品や機械システムさえも迅速に製造できるアクセス性と柔軟性から、注目すべき製造プロセスの1つとして浮上しています。

自動3Dプリンティング市場動向

自動車分野が市場の成長を牽引する見込み

- 自動車は、今日の主要な交通手段として、人間の生活に欠かせないものです。現在、世界には13億台以上の自動車が走っており、その数は2035年までに18億台に増加すると予想されています。乗用車はこの統計のおよそ74%を占め、小型商用車と大型トラック、バス、コーチ、ミニバスが残りの26%を占めています。

- 3Dプリンティングは、グリップ、治具、固定具を迅速に製造するための金型や熱成形ツールの製造に使用できます。これにより、自動車メーカーはサンプルや工具を低コストで製造でき、高コストの金型に投資する際の将来の生産ロスをなくすことができます。史上初の3Dプリント電気自動車は、2014年にローカル・モーターズによって発売されました。その後、BMWグループのような他の老舗企業も、自動3Dプリント技術の採用という点で追随しています。米国の大手自動車メーカー数社では、各初期プロトタイプの組み立ての約80%~90%が3Dプリントされており、自動化の傾向はますます強まっています。人気のある部品の中には、排気、吸気、ダクトの部品があります。これらの部品はデジタルで設計され、3Dプリントされ、短時間で自動車に取り付けられ、その後何度も繰り返しテストされます。

- 自動車業界における自動3Dプリントの最も一般的な用途は、治具や冶具のような製造補助具の製作でしょう。従来の方法で製造ツールを作成するのは、かなりコストと時間がかかり、形状の制限により製造プロセスの効率が低下し、最終使用部品の形状に制約が生じます。3Dプリントされた製造ツールは、より軽量で人間工学的であるため、工場の作業員がより簡単かつ安全に作業を行うことができます。

- さらに、自動車製造に関連する生産量は非常に多く、部品ごとに数十万回に及ぶ。これは、ほとんどの3Dプリント技術では(今のところ)追いつくのが難しいと思われます。しかし、多くのハイエンド自動車メーカーは、自動車の生産台数を数千台に制限しているため、自動3Dプリントは現実的な選択肢となっています。

- 世界経済フォーラムによると、2035年には完全自律走行車が前年比1,200万台以上販売され、世界の自動車市場の25%をカバーすると予想されています。また、電気モーターメーカーによるいくつかの取り組みが、市場の成長につながっています。2020年3月、英国のエンジニアリング会社Equipmakeは、パワー密度の高い永久磁石電気モーターを開発しました。このモーターは、3DプリンティングのスペシャリストであるHieta社と共同で設計されました。EquipmakeのAmpereモーターは、重量は10kgに近いが、出力は295bhpを発揮します。

- さらに、ブラケットは小さくてありふれた部品であるため、エンジニアが伝統的な製造方法に制約されていた以前は、最適化することが非常に困難でした。現在では、エンジニアは最適化されたブラケットを設計し、3Dプリントの助けを借りてこれらの設計を実現することができます。ロールスロイスは最近、ブラケット用の3Dプリンティングの能力を披露しました。同社は、DfAMで最適化され、3Dプリントされた大量の自動車用金属部品を披露したが、その多くはブラケットに見えるものでした。自動車業界では、プロトタイピングが3Dプリントの主な用途であることに変わりはないが、この技術を金型に使用する動きが急速に広がっています。フォルクスワーゲンは、数年前から社内で3Dプリンティングを使用しています。同社のバインダージェッティング技術もコンポーネントの構築に使用されています。また、フォルクスワーゲンは2021年7月、シーメンスおよびHPと提携し、構造部品の3Dプリンティングを工業化すると発表しました。

北米が大きな市場シェアを占める見込み

- 北米は、自動3Dプリンティングにとって世界的に重要な市場の1つであり、米国がこの地域で大きなシェアを占めています。同国の需要の高まりは、大小さまざまなベンダーが存在することに起因しています。例えば、カリフォルニア州カールスバッドにあるForecast 3D社は、ヘルスケア、自動車、航空宇宙、消費者製品、デザイン業界向けに様々な素材の3Dプリントサービスを提供しています。

- クローズドループ制御システムは、強力なAIアプリケーションの急速な開発により、積層造形技術者の基本的な目標となって久しいです。例えば、ニューヨーク州にあるGEのニスカユナ積層造形研究所(Niskayuna Additive Research Lab)の調査チームは、高解像度カメラを使って印刷工程をレイヤーごとに監視し、肉眼では通常見えないストリーク、ピット、穴、その他の問題を検出する独自の機械学習プラットフォームを開発しました。さらに、このデータは、コンピューター断層撮影(CT)画像を利用して事前に記録された欠陥データベースとリアルタイムで比較されます。AIシステムは、高解像度の画像とCTスキャンデータを使って、印刷プロセス全体を通して困難を予測し、欠陥を検出するように訓練されます。

- さらに、市場はポリマー3Dプリンティングに関する様々な技術特許を目の当たりにしています。例えば、2020年8月、産業用3Dプリンティングの自動化されたインテリジェントなポストプリンティング・ソリューションのプロバイダーの1つであるPostProcess Technologies Inc.は、ポリマー3Dプリンティングの自動ポストプリンティング技術の特許を取得しました。SVC技術は、PostProcessのアディティブ・マニュファクチャリング・ファミリーである3Dプリントポリマー支持体除去および樹脂除去ソリューションの一部です。この特許取得済みの方法は、特許申請中の洗浄剤と独自のアルゴリズムを使用し、3Dプリントされたコンポーネントがポストプリント中に均一、一貫、確実に洗浄剤とキャビテーションにさらされるようにします。

- また、様々なベンダーが、主にサプライチェーンの課題と様々なエンドユーザー垂直分野での需要拡大に対応するために、この地域に施設を拡大しています。例えば2021年2月、Robozeは米国テキサス州ヒューストンに米国本社を開設し、国内生産のリショアリングを促進してサプライチェーンの問題に対処すると発表しました。Robozeは今後2年間で100人以上の従業員を雇用する計画で、米国でのエンジニアリングと生産能力を増強し、航空宇宙、石油・ガス、モビリティなどの業界における3Dプリンティング技術への需要の高まりに対応できるようになります。

- 同様に、Robozeは2021年4月、スーパーポリマーや複合材を使ったカスタマイズ3Dプリンティングを極端なエンドユーザー用途の生産ワークフローに導入する産業用自動化システム「Roboze Automate」の発売を発表しました。米国は、エネルギーから輸送、製造に至るまで、インフラストラクチャーの推進に着手する中で、各産業分野に影響を及ぼす金属不足に見舞われています。Robozeは、理想的な金属代替技術である斬新なポリマープラットフォーム技術PEEKと、B&Rとの提携により開発されたPLC産業オートメーションシステムを組み合わせました。

自動3Dプリンティング業界の概要

自動3Dプリンティング市場は競争が激しく、より大きなシェアを獲得しようとする複数の主要プレイヤーで構成されているが、主要プレイヤーは消費者の大きな割合を獲得しており、またさらなる開発と革新のために研究開発やハードウェアベンダーとの提携に投資しています。主要企業には、Stratasys Ltd、3D Systems Corporation、The ExOne Companyなどが含まれます。

- 2022年2月-Viaccess-Orca、ShipParts.com、SLM Solutionsは、アディティブマニュファクチャリング(AM)のCloud-to-Printを直接可能にする新技術ソリューションを発表しました。この完全に自動化されたソフトウェア実行は、許容されるプリントの量、期間、パラメーターを制御することで、部品データに関連するメーカーの知的財産(IP)を保護します。VOのSMPソフトウェア・ライブラリとSLMソリューションズのマシン・ファームウェアのネイティブな統合に基づくこのCloud-to-Printソリューションにより、メーカーは、印刷がライセンスされる際に自社のIPが保護されることを十分に確信することができます。

- 2022年1月-積層造形(AM)ソフトウェアとサービスの著名なプロバイダーであるMaterialise NV、品質保証ソフトウェアのプロバイダーであるSigma Labs, Inc.、およびMaterialiseは共同で、金属AMアプリケーションのスケーラビリティを強化する技術を開発しました。この新しいプラットフォームは、Sigma LabsのPrintRite3Dセンサー技術とMaterialise Control Platformを組み合わせ、ユーザーがリアルタイムで金属造形の問題を特定し、修正することを可能にします。

- 2022年1月-PostProcess Technologies社は、自動化されたインテリジェントなポストプリンティング(後加工)ソリューションの新しいラインアップを追加することを発表しました。新しいVORSA 500は、PostProcessの技術を活用し、3DプリントされたFDM部品のサポート構造を一貫してハンズフリーで除去します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3カ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 研究開発投資の増加

- 産業オートメーションへのロボット導入の増加

- 市場の課題

- 運用上の課題

第6章 市場セグメンテーション

- 提供

- ハードウェア

- ソフトウェア

- サービス

- プロセス

- 自動生産

- マテリアルハンドリング

- パーツハンドリング

- 後加工

- マルチプロセシング

- エンドユーザー業界別

- 工業生産

- 自動車

- 航空宇宙・防衛

- 消費者向け製品

- ヘルスケア

- エネルギー

- その他エンドユーザー業界別

- 地域

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Stratasys Ltd

- Concept Laser Inc.(GE Additive)

- The ExOne Company

- SLM Solutions Group AG

- 3D Systems Corporation

- Universal Robots AS

- Formlabs

- PostProcess Technologies Inc.

- Materialise NV

- Authentise Inc.

- DWS Systems

- Coobx AG

- ABB Group

第8章 投資分析

第9章 市場機会と今後の動向

The Automated 3D Printing Market size is estimated at USD 2.91 billion in 2025, and is expected to reach USD 13.77 billion by 2030, at a CAGR of 36.49% during the forecast period (2025-2030).

The increasing investments in R&D and growth in the adoption of robotics for industrial automation are expected to propel market growth.

Key Highlights

- Over the last few years, 3D printing has constantly experienced a shift from the prototyping and small batches phase to mass production technology with a growing adoption rate across the industries, where the industrial and non-printer vendors have shifted their focus toward automation. Also, with the evolutionary trend for additive manufacturing, hardware growing beyond stand-alone systems that are used for prototyping, tooling, and single-part production to be used as core systems within integrated digital mass production lines is driving the number of opportunities in the emerging lights-out factories.

- Artificial Intelligence and machine learning technologies are finding their way through various applications in the additive manufacturing industry. For instance, researchers from MIT have applied the data-driven nature of machine learning to automate the process of discovering new 3D printing materials. With machine learning, material performance factors, such as toughness and compression strength, were optimized using an algorithm that quickly outperformed conventional methods of 3D printing material formulation. The researchers developed a free, open-source materials optimization platform called AutoOED, allowing other researchers to conduct their material optimization.

- Similarly, in January 2022, a group of organizations from Germany and Canada formed a new collaboration to use 3D printing and AI to automate the process of fixing parts. The Artificial Intelligence Enhancement of Process Sensing for Adaptive Laser Additive Manufacturing (AI-SLAM) project aims to create powerful AI-based software that can run directed energy deposition (DED) 3D printers automatically. To more successfully repair uneven surfaces on damaged components, the software will algorithmically regulate the printing process. The Fraunhofer Institute for Laser Technology (ILT) and a software company BCT are part of the German consortium. In Canada, the work will be overseen by the National Research Council of Canada (NRC). McGill University will coordinate the research, and machine learning firm Braintoy will help program the AI models.

- Furthermore, there have been various developments in the market by players to enhance their position in the market. For instance, in April 2021, Mosaic launched Array, an automated 3D printing platform, which loads and unloads materials for its four Element HT printers, starts prints, removes prints, and stores them so that the next prints can begin. The Array is designed for maximum flexibility with its vending machine-style robotic arm that removes prints, places them to the side, and loads a clean bed for the next print, ensuring maximum output.

- In October 2021, 3DQue, a Vancouver-based developer of automation technology for the 3D printing industry, announced the launch of two new Quinly automation kits for the Creality CR-10 and CR-6 SE. Quinly is a virtual 3D printer operator served by a Raspberry Pi, a hardware and software kit capable of running desktop 3D printers on its own. The technology is designed to make 3D printing more scalable by taking manual labor out of the equation. It is primarily aimed at print labs, on-demand manufacturers, educational institutions, and anyone else seeking automated mass part production.

- Additionally, due to the disruption of supply chains and new demands for treatments and materials, the COVID-19 pandemic has significantly accelerated technological advancements in the pharmaceutical, medical device, and manufacturing sectors. The supply chain shortages have made it hard for medical personnel to get the supplies they need, generating a shortage of personal protection equipment (PPE) and medical devices in hospitals for fighting off the virus. Owing to this, additive manufacturing (AM) (automated 3D printing) has emerged as one remarkable fabrication process because of its accessibility and flexibility to produce complex and monolithic parts or even mechanical systems quickly.

Automated 3D Printing Market Trends

The Automotive Segment is Expected to Drive the Market's Growth

- Automobiles are an essential part of human lives as the main mode of transportation today. Currently, there are over 1.3 billion motor vehicles on the road globally, with that number expected to rise to 1.8 billion by the year 2035. Passenger cars comprise roughly 74% of these statistics, while light commercial vehicles and heavy trucks, buses, coaches, and minibusses make up the remaining 26%.

- 3D printing can be used in making molds and thermoforming tools for the rapid manufacturing of grips, jigs, and fixtures. This allows automakers to produce samples and tools at low costs and eliminate future production losses when investing in high-cost tooling. The first-ever 3D-printed electric car was launched in 2014 by Local Motors. Subsequently, other established firms, like the BMW group, have also followed suit in terms of adopting automated 3D printing techniques. In several major US auto manufacturers, around 80%-90% of each initial prototype assembly has been 3D printed, with an increasing trend toward automation. Some of the popular components are parts of the exhaust, air intake, and ducting. These parts are designed digitally, 3D printed, and fitted on a car in short order, then tested through multiple iterations.

- Perhaps the most popular use of automated 3D printing in the automotive space is fabricating manufacturing aids like jigs and fixtures. Making manufacturing tools using traditional means is rather costly and time-consuming, and geometry limitations translate into less efficient manufacturing processes and more constraints on the geometry of end-use parts. Manufacturing tools that are 3D printed are lighter and more ergonomic, making it easier and safer for factory workers to perform their duties.

- Furthermore, the production volumes associated with automotive manufacturing are very high, tallying to hundreds of thousands of runs for every part. That would be difficult for most 3D printing technologies to keep up with (for now). But many high-end automobile manufacturers limit the production runs of their cars to only a few thousand units, which makes automated 3d printing a viable option.

- According to the World Economic Forum, more than 12 million fully autonomous cars are expected to be sold per year-on-year 2035, covering 25% of the global automotive market. Also, several initiatives taken by the electric motor manufacturers are leading to the growth of the market. In March 2020, UK-based engineering company Equipmake developed a power-dense permanent magnet electric motor. The motor was designed in collaboration with Hieta, a 3D printing specialist. Equipmake's Ampere motor will weigh near to 10kg but provide an output of 295bhp.

- Furthermore, Brackets are small and rather mundane parts, which were very difficult to optimize in the past time when engineers were constrained by the traditional manufacturing methods. Currently, engineers can design optimized brackets and bring these designs to life with the help of 3D printing. Rolls Royce recently showcased the capabilities of 3D printing for brackets. The company showed off a large batch of DfAM-optimized and 3D-printed automotive metal parts, many of which look to be bracketed. While prototyping remains the primary application of 3D printing within the automotive industry, using the technology for tooling is rapidly catching on. One major example of this is Volkswagen, which has been using 3D printing in-house for a number of years. Their binder jetting technology is also in use to construct the component. Also, in July 2021, Volkswagen stated that it is partnering with Siemens and HP to industrialize 3D printing of structural parts, which can be significantly lighter than equivalent components made of sheet steel.

North America is Expected to Hold a Major Market Share

- North America is one of the significant markets for Automated 3D printing globally, with the United States accounting for a significant share in the region. The country's rising demand can be attributed to the vast presence of small and big vendors. For instance, Forecast 3D in Carlsbad, CA, offers 3D printing services in a variety of materials to the healthcare, automotive, aerospace, consumer products, and design industries.

- Closed-loop control systems have long been a fundamental aim for additive manufacturing engineers due to the rapid development of powerful AI applications. For instance, Researchers at GE's Niskayuna Additive Research Lab, New York, created a proprietary machine-learning platform that uses high-resolution cameras to monitor the printing process layer by layer and detect streaks, pits, holes, and other problems that are typically invisible to the naked eye. Further, The data is compared in real-time to a pre-recorded flaws database utilizing computer tomography (CT) imaging. The AI system will be trained to forecast difficulties and detect flaws throughout the printing process using the high-resolution image and CT scan data.

- Furthermore, the market is witnessed with various technology patents for polymer 3D printing. For instance, in August 2020, PostProcess Technologies Inc., one of the providers of automated and intelligent post-printing solutions for industrial 3D printing, received a patent for automated post-printing technology for polymer 3D printing. The SVC technology is part of PostProcess's additive manufacturing family of 3D printed polymer support removal and resin removal solutions. This patented method uses patent-pending detergents and proprietary algorithms to ensure that 3D printed components are exposed to detergent and cavitation uniformly, consistently, and reliably during post-printing.

- Also, various vendors are expanding facilities into the region, primarily to address the supply chain challenges and growing demand in various end-user verticals. For instance, in February 2021, Roboze announced the opening of its US headquarters in Houston, Texas, to facilitate the reshoring of domestic production and address supply chain issues. Roboze will be able to increase its engineering and production capacity in the United States with plans to hire over 100 employees in the next two years and address a growing demand for 3D printing technology in industries such as aerospace, oil and gas, and mobility.

- Similarly, in April 2021, Roboze announced the launch of Roboze Automate, the industrial automation system to bring customized 3D printing with super polymers and composites into the production workflow for extreme end-user applications. The United States is experiencing a metals deficit that is affecting each of the industry areas as it begins an infrastructure push that spans from energy to transportation to manufacturing. Roboze combined its novel polymer platform technology, PEEK, an ideal metals replacement technology, with a PLC industrial automation system developed in partnership with B&R.

Automated 3D Printing Industry Overview

The automated 3D printing market is competitive and consists of several major players who are trying to gain a larger share, but top players have gained a major proportion of consumers and also investing in R&D and partnerships with hardware vendors for more developments and innovations. Some of the key players include Stratasys Ltd, 3D Systems Corporation, and The ExOne Company, among others.

- February 2022 - Viaccess-Orca, ShipParts.com, along with SLM Solutions, announced a new technology solution that enables direct Cloud-to-Print for additive manufacturing (AM). This fully automated software execution protects the manufacturer's intellectual property (IP) associated with part data by controlling the quantity, duration, and parameters of acceptable prints. Based on the native integration of VO's SMP software library and SLM Solutions machine firmware, this Cloud-to-Print solution allows manufacturers to be fully confident that their IP will be protected when printing is licensed.

- January 2022 - Materialise NV, a renowned provider of additive manufacturing (AM) software and services, Sigma Labs, Inc., a provider of quality assurance software, and Materialise, together have developed a technology to enhance the scalability of metal AM applications. The new platform combines Sigma Labs' PrintRite3D sensor technology to Materialise Control Platform to enable the users to identify and correct metal build issues in real-time.

- January 2022 - PostProcess Technologies announced the addition of a new solution lineup of automated, intelligent post-printing solutions for additive manufacturing (AM) to its portfolio. The new VORSA 500 leverages PostProcess technology for consistent, hands-free support structure removal on 3D printed FDM parts.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assestment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Investments in R&D

- 5.1.2 Growth in Adoption of Robotics for Industrial Automation

- 5.2 Market Challenges

- 5.2.1 Operational Challenges

6 MARKET SEGMENTATION

- 6.1 Offering

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Services

- 6.2 Process

- 6.2.1 Automated Production

- 6.2.2 Material Handling

- 6.2.3 Part Handling

- 6.2.4 Post-Processing

- 6.2.5 Multiprocessing

- 6.3 End-user Vertical

- 6.3.1 Industrial Manufacturing

- 6.3.2 Automotive

- 6.3.3 Aerospace and Defense

- 6.3.4 Consumer Products

- 6.3.5 Healthcare

- 6.3.6 Energy

- 6.3.7 Other End-user Verticals

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Stratasys Ltd

- 7.1.2 Concept Laser Inc. (GE Additive)

- 7.1.3 The ExOne Company

- 7.1.4 SLM Solutions Group AG

- 7.1.5 3D Systems Corporation

- 7.1.6 Universal Robots AS

- 7.1.7 Formlabs

- 7.1.8 PostProcess Technologies Inc.

- 7.1.9 Materialise NV

- 7.1.10 Authentise Inc.

- 7.1.11 DWS Systems

- 7.1.12 Coobx AG

- 7.1.13 ABB Group