|

|

市場調査レポート

商品コード

1676820

タイヤモールド3Dプリンタ市場:プリンタ技術タイプ、用途、エンドユーザー、用途別-2025-2030年世界予測Tire Mold 3D Printer Market by Printer Technology Type, Application, End-User, Usage - Global Forecast 2025-2030 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイヤモールド3Dプリンタ市場:プリンタ技術タイプ、用途、エンドユーザー、用途別-2025-2030年世界予測 |

|

出版日: 2025年03月09日

発行: 360iResearch

ページ情報: 英文 180 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 図表

- 目次

タイヤモールド3Dプリンタ市場は、2024年には6億1,951万米ドルとなり、2025年には7億3,709万米ドル、CAGR20.23%で成長し、2030年には18億7,163万米ドルに達すると予測されています。

| 主な市場の統計 | |

|---|---|

| 基準年 2024 | 6億1,951万米ドル |

| 推定年 2025 | 7億3,709万米ドル |

| 予測年 2030 | 18億7,163万米ドル |

| CAGR(%) | 20.23% |

近年、アディティブ・マニュファクチャリングの進化は産業用途に新時代をもたらし、タイヤ金型3Dプリンティングはこの変革の最前線に立っています。このイントロダクションでは、現在の技術的進歩、市場力学、そして革新的な製造プロセスに投資する企業にとって前途有望な未来を探ることで、その舞台を整えます。先進的な3Dプリンティング手法によって生産能力が再定義され、従来の製造技術に比べて納期が短縮され、カスタマイズ性が向上し、効率が改善されました。

タイヤ金型3Dプリンティング市場は、技術的な洗練と戦略的な進化が複雑に絡み合っています。最先端のデジタル技術と試行錯誤の工業的手法を融合させることで、プロトタイピングと生産製造という2つのニーズに対応しています。技術革新がより深い洞察と多様な応用への道を開く中、この分野は次世代の製造プロセスを形成する上で不可欠な要素であることが証明されつつあります。そこで、市場全体の可能性、生産手法に革命をもたらし続ける画期的な動向、そしてこの急成長分野で成功するために必要な戦略的必須事項を理解することに焦点を移します。

市場進化の原動力となる変革的変化

タイヤモールド3Dプリンター市場の進化は、画期的なイノベーションと、製造業の展望を再構築する新たな動向によって推進されています。従来の金型製造技術からデジタル主導のプロセスへの移行には、大きな変革が見られます。この変化は技術的なものだけでなく文化的なものでもあり、業界が長年の慣習を見直し、デジタル統合を急速に受け入れる環境を醸成しています。

この分野におけるデジタルトランスフォーメーションは、デジタル・ライト・プロセッシング(DLP)、溶融積層造形(FDM)、選択的レーザー焼結(SLS)、ステレオリソグラフィ(SLA)などの高度な印刷技術の採用によって強調されています。これらの技術は、より時間のかかる旧来のプロトタイピングや生産方法に取って代わりつつあり、精度の向上、無駄の削減、納期の短縮を実現しています。

同時に、持続可能性とコスト効率を重視する傾向が強まり、俊敏な製造プロセスの採用が加速しています。先進的な市場プレーヤーは、新たな生産動向から得た知見を活用して業務の効率化を推進し、革新的なタイヤ金型に対する世界の需要の増加に対応しています。その結果、業界は市場競争力の強化を目の当たりにすることになり、より迅速な設計の繰り返しが高品質な製品に直結し、混戦のマーケットプレースにおける競争力が向上しています。市場の進化は、技術革新と実用化の両立の必要性を明確にし、工業生産と設計の多様性の両方における進歩のための肥沃な情勢を作り出しています。

戦略的優位性のための業界セグメンテーション洞察の活用

タイヤモールド3Dプリンター市場の多様なセグメンテーションを理解することは、現在のビジネスチャンスと将来の可能性の両方を捉える上で極めて重要です。セグメンテーションのさまざまな側面から市場行動のさまざまな側面に光を当て、最終的にはより良い戦略的意思決定を導きます。市場はプリンタ技術のタイプ別に調査され、デジタル光造形(DLP)、溶融積層造形(FDM)、選択的レーザー焼結(SLS)、ステレオリソグラフィ(SLA)などの方式が、それぞれ製品出力と設計精度に独自に貢献しています。これらの技術は、詳細なプロトタイプの作成や、最終的な工業用部品の製造における特定の利点に基づいて慎重に選択されます。

さらに、市場は、生産製造とプロトタイピングの両方を包含するアプリケーションコンテキストによって定義されます。大量生産では、精度と一貫性を維持する能力が、ラピッドプロトタイピングに必要な合理化されたワークフローと同様に重要です。セグメンテーションはさらにエンドユーザー層にまで及び、航空宇宙分野と自動車分野の両方が含まれます。自動車分野では、大型商用車と小型商用車の両方を含む商用車と、コンバーチブル、ハッチバック、セダン、SUV、バンなどのカテゴリーにまたがる乗用車に細分化され、さらに複雑なレイヤーが存在します。自動車セグメンテーションの各層は、カスタマイズ、材料の互換性、生産速度などの要因に影響を与え、明確な課題と機会を提示します。

アフターマーケットと相手先ブランド製造業者(OEメーカー)を区別して使用状況を見ると、セグメンテーションの新たな側面が浮かび上がってくる。この二分化は、市場アプローチを決定するだけでなく、製品ライフサイクルの様々な段階におけるイノベーション戦略と顧客エンゲージメントにも影響を与えます。多様なセグメンテーションモデルから得られるこれらの微妙な洞察を統合することで、業界関係者は、ニッチ市場をターゲットとし、技術展開を最適化し、製品提供を的確な市場ニーズに合わせるための包括的なロードマップを得ることができます。

目次

第1章 序文

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の概要

第5章 市場洞察

- 市場力学

- 促進要因

- 環境への懸念の高まりにより、環境に優しく効率的な生産方法の採用が進む

- 自動車生産の増加により、コスト効率の高いタイヤ金型製造の需要が高まっている

- カスタマイズされた複雑なタイヤ設計の需要増加

- 抑制要因

- タイヤ金型3Dプリントセットアップには高額の初期資本投資が必要

- 機会

- 3Dプリント技術の継続的な進歩

- 3Dプリントの導入を促進する政府の支援策と資金提供

- 課題

- タイヤ金型の3Dプリントに関連する技術的制限と規制上の問題を乗り越える

- 促進要因

- 市場セグメンテーション分析

- プリンター技術の種類:コスト効率と材料の汎用性から、熱溶解積層法の採用が増加

- アプリケーション:タイヤモールド3Dプリンタのプロトタイプ作成における重要性が高まり、新しいタイヤ金型設計の市場投入までの時間が短縮されます。

- ポーターのファイブフォース分析

- PESTEL分析

- 政治的

- 経済

- 社会

- 技術的

- 法律上

- 環境

第6章 タイヤモールド3Dプリンタ市場プリンター技術タイプ別

- デジタル光処理(DLP)

- 熱溶解積層法(FDM)

- 選択的レーザー焼結(SLS)

- ステレオリソグラフィー(SLA)

第7章 タイヤモールド3Dプリンタ市場:用途別

- 生産製造

- プロトタイピング

第8章 タイヤモールド3Dプリンタ市場:エンドユーザー別

- 航空宇宙

- 自動車

- 商用車

- 大型商用車

- 小型商用車

- 乗用車

- コンバーチブル

- ハッチバック

- セダン

- SUV

- バン

- 商用車

第9章 タイヤモールド3Dプリンタ市場用途別

- アフターマーケット

- オリジナル機器メーカー

第10章 南北アメリカのタイヤモールド3Dプリンタ市場

- アルゼンチン

- ブラジル

- カナダ

- メキシコ

- 米国

第11章 アジア太平洋地域のタイヤモールド3Dプリンタ市場

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- フィリピン

- シンガポール

- 韓国

- 台湾

- タイ

- ベトナム

第12章 欧州・中東・アフリカのタイヤモールド3Dプリンタ市場

- デンマーク

- エジプト

- フィンランド

- フランス

- ドイツ

- イスラエル

- イタリア

- オランダ

- ナイジェリア

- ノルウェー

- ポーランド

- カタール

- ロシア

- サウジアラビア

- 南アフリカ

- スペイン

- スウェーデン

- スイス

- トルコ

- アラブ首長国連邦

- 英国

第13章 競合情勢

- 市場シェア分析, 2024

- FPNVポジショニングマトリックス, 2024

- 競合シナリオ分析

- 戦略分析と提言

企業一覧

- 3D Systems Corp.

- AddUp Group

- BigRep GmbH

- Desktop Metal, Inc.

- EOS GmbH Electro Optical Systems

- Eplus3D

- MATERIALISE NV

- Proto Labs, Inc.

- SLM So-lu-tions Group AG

- Stratasys Ltd.

- UnionTech

- Voxeljet AG

LIST OF FIGURES

- FIGURE 1. TIRE MOLD 3D PRINTER MARKET MULTI-CURRENCY

- FIGURE 2. TIRE MOLD 3D PRINTER MARKET MULTI-LANGUAGE

- FIGURE 3. TIRE MOLD 3D PRINTER MARKET RESEARCH PROCESS

- FIGURE 4. TIRE MOLD 3D PRINTER MARKET SIZE, 2024 VS 2030

- FIGURE 5. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, 2018-2030 (USD MILLION)

- FIGURE 6. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY REGION, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 7. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 8. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2024 VS 2030 (%)

- FIGURE 9. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 10. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2024 VS 2030 (%)

- FIGURE 11. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 12. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2024 VS 2030 (%)

- FIGURE 13. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 14. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2024 VS 2030 (%)

- FIGURE 15. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 16. AMERICAS TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 17. AMERICAS TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 18. UNITED STATES TIRE MOLD 3D PRINTER MARKET SIZE, BY STATE, 2024 VS 2030 (%)

- FIGURE 19. UNITED STATES TIRE MOLD 3D PRINTER MARKET SIZE, BY STATE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 20. ASIA-PACIFIC TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 21. ASIA-PACIFIC TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 22. EUROPE, MIDDLE EAST & AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 23. EUROPE, MIDDLE EAST & AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 24. TIRE MOLD 3D PRINTER MARKET SHARE, BY KEY PLAYER, 2024

- FIGURE 25. TIRE MOLD 3D PRINTER MARKET, FPNV POSITIONING MATRIX, 2024

LIST OF TABLES

- TABLE 1. TIRE MOLD 3D PRINTER MARKET SEGMENTATION & COVERAGE

- TABLE 2. UNITED STATES DOLLAR EXCHANGE RATE, 2018-2024

- TABLE 3. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, 2018-2030 (USD MILLION)

- TABLE 4. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 5. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 6. TIRE MOLD 3D PRINTER MARKET DYNAMICS

- TABLE 7. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 8. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY DIGITAL LIGHT PROCESSING (DLP), BY REGION, 2018-2030 (USD MILLION)

- TABLE 9. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY FUSED DEPOSITION MODELING (FDM), BY REGION, 2018-2030 (USD MILLION)

- TABLE 10. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY SELECTIVE LASER SINTERING (SLS), BY REGION, 2018-2030 (USD MILLION)

- TABLE 11. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY STEREOLITHOGRAPHY (SLA), BY REGION, 2018-2030 (USD MILLION)

- TABLE 12. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 13. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY PRODUCTION MANUFACTURING, BY REGION, 2018-2030 (USD MILLION)

- TABLE 14. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY PROTOTYPING, BY REGION, 2018-2030 (USD MILLION)

- TABLE 15. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 16. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY AEROSPACE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 17. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 18. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 19. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY HEAVY COMMERCIAL VEHICLES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 20. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY LIGHT COMMERCIAL VEHICLES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 21. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 22. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 23. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY CONVERTIBLE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 24. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY HATCHBACK, BY REGION, 2018-2030 (USD MILLION)

- TABLE 25. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY SEDAN, BY REGION, 2018-2030 (USD MILLION)

- TABLE 26. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY SUV, BY REGION, 2018-2030 (USD MILLION)

- TABLE 27. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY VAN, BY REGION, 2018-2030 (USD MILLION)

- TABLE 28. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 29. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 30. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 31. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY AFTERMARKET, BY REGION, 2018-2030 (USD MILLION)

- TABLE 32. GLOBAL TIRE MOLD 3D PRINTER MARKET SIZE, BY ORIGINAL EQUIPMENT MANUFACTURERS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 33. AMERICAS TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 34. AMERICAS TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 35. AMERICAS TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 36. AMERICAS TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 37. AMERICAS TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 38. AMERICAS TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 39. AMERICAS TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 40. AMERICAS TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 41. ARGENTINA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 42. ARGENTINA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 43. ARGENTINA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 44. ARGENTINA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 45. ARGENTINA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 46. ARGENTINA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 47. ARGENTINA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 48. BRAZIL TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 49. BRAZIL TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 50. BRAZIL TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 51. BRAZIL TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 52. BRAZIL TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 53. BRAZIL TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 54. BRAZIL TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 55. CANADA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 56. CANADA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 57. CANADA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 58. CANADA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 59. CANADA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 60. CANADA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 61. CANADA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 62. MEXICO TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 63. MEXICO TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 64. MEXICO TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 65. MEXICO TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 66. MEXICO TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 67. MEXICO TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 68. MEXICO TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 69. UNITED STATES TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 70. UNITED STATES TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 71. UNITED STATES TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 72. UNITED STATES TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 73. UNITED STATES TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 74. UNITED STATES TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 75. UNITED STATES TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 76. UNITED STATES TIRE MOLD 3D PRINTER MARKET SIZE, BY STATE, 2018-2030 (USD MILLION)

- TABLE 77. ASIA-PACIFIC TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 78. ASIA-PACIFIC TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 79. ASIA-PACIFIC TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 80. ASIA-PACIFIC TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 81. ASIA-PACIFIC TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 82. ASIA-PACIFIC TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 83. ASIA-PACIFIC TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 84. ASIA-PACIFIC TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 85. AUSTRALIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 86. AUSTRALIA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 87. AUSTRALIA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 88. AUSTRALIA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 89. AUSTRALIA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 90. AUSTRALIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 91. AUSTRALIA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 92. CHINA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 93. CHINA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 94. CHINA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 95. CHINA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 96. CHINA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 97. CHINA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 98. CHINA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 99. INDIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 100. INDIA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 101. INDIA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 102. INDIA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 103. INDIA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 104. INDIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 105. INDIA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 106. INDONESIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 107. INDONESIA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 108. INDONESIA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 109. INDONESIA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 110. INDONESIA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 111. INDONESIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 112. INDONESIA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 113. JAPAN TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 114. JAPAN TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 115. JAPAN TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 116. JAPAN TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 117. JAPAN TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 118. JAPAN TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 119. JAPAN TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 120. MALAYSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 121. MALAYSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 122. MALAYSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 123. MALAYSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 124. MALAYSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 125. MALAYSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 126. MALAYSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 127. PHILIPPINES TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 128. PHILIPPINES TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 129. PHILIPPINES TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 130. PHILIPPINES TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 131. PHILIPPINES TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 132. PHILIPPINES TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 133. PHILIPPINES TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 134. SINGAPORE TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 135. SINGAPORE TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 136. SINGAPORE TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 137. SINGAPORE TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 138. SINGAPORE TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 139. SINGAPORE TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 140. SINGAPORE TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 141. SOUTH KOREA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 142. SOUTH KOREA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 143. SOUTH KOREA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 144. SOUTH KOREA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 145. SOUTH KOREA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 146. SOUTH KOREA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 147. SOUTH KOREA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 148. TAIWAN TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 149. TAIWAN TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 150. TAIWAN TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 151. TAIWAN TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 152. TAIWAN TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 153. TAIWAN TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 154. TAIWAN TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 155. THAILAND TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 156. THAILAND TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 157. THAILAND TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 158. THAILAND TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 159. THAILAND TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 160. THAILAND TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 161. THAILAND TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 162. VIETNAM TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 163. VIETNAM TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 164. VIETNAM TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 165. VIETNAM TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 166. VIETNAM TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 167. VIETNAM TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 168. VIETNAM TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 169. EUROPE, MIDDLE EAST & AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 170. EUROPE, MIDDLE EAST & AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 171. EUROPE, MIDDLE EAST & AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 172. EUROPE, MIDDLE EAST & AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 173. EUROPE, MIDDLE EAST & AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 174. EUROPE, MIDDLE EAST & AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 175. EUROPE, MIDDLE EAST & AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 176. EUROPE, MIDDLE EAST & AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 177. DENMARK TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 178. DENMARK TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 179. DENMARK TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 180. DENMARK TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 181. DENMARK TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 182. DENMARK TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 183. DENMARK TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 184. EGYPT TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 185. EGYPT TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 186. EGYPT TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 187. EGYPT TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 188. EGYPT TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 189. EGYPT TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 190. EGYPT TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 191. FINLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 192. FINLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 193. FINLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 194. FINLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 195. FINLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 196. FINLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 197. FINLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 198. FRANCE TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 199. FRANCE TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 200. FRANCE TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 201. FRANCE TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 202. FRANCE TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 203. FRANCE TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 204. FRANCE TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 205. GERMANY TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 206. GERMANY TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 207. GERMANY TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 208. GERMANY TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 209. GERMANY TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 210. GERMANY TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 211. GERMANY TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 212. ISRAEL TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 213. ISRAEL TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 214. ISRAEL TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 215. ISRAEL TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 216. ISRAEL TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 217. ISRAEL TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 218. ISRAEL TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 219. ITALY TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 220. ITALY TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 221. ITALY TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 222. ITALY TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 223. ITALY TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 224. ITALY TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 225. ITALY TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 226. NETHERLANDS TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 227. NETHERLANDS TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 228. NETHERLANDS TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 229. NETHERLANDS TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 230. NETHERLANDS TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 231. NETHERLANDS TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 232. NETHERLANDS TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 233. NIGERIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 234. NIGERIA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 235. NIGERIA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 236. NIGERIA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 237. NIGERIA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 238. NIGERIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 239. NIGERIA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 240. NORWAY TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 241. NORWAY TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 242. NORWAY TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 243. NORWAY TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 244. NORWAY TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 245. NORWAY TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 246. NORWAY TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 247. POLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 248. POLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 249. POLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 250. POLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 251. POLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 252. POLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 253. POLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 254. QATAR TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 255. QATAR TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 256. QATAR TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 257. QATAR TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 258. QATAR TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 259. QATAR TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 260. QATAR TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 261. RUSSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 262. RUSSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 263. RUSSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 264. RUSSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 265. RUSSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 266. RUSSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 267. RUSSIA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 268. SAUDI ARABIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 269. SAUDI ARABIA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 270. SAUDI ARABIA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 271. SAUDI ARABIA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 272. SAUDI ARABIA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 273. SAUDI ARABIA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 274. SAUDI ARABIA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 275. SOUTH AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 276. SOUTH AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 277. SOUTH AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 278. SOUTH AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 279. SOUTH AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 280. SOUTH AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 281. SOUTH AFRICA TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 282. SPAIN TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 283. SPAIN TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 284. SPAIN TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 285. SPAIN TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 286. SPAIN TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 287. SPAIN TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 288. SPAIN TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 289. SWEDEN TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 290. SWEDEN TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 291. SWEDEN TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 292. SWEDEN TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 293. SWEDEN TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 294. SWEDEN TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 295. SWEDEN TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 296. SWITZERLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 297. SWITZERLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 298. SWITZERLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 299. SWITZERLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 300. SWITZERLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 301. SWITZERLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 302. SWITZERLAND TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 303. TURKEY TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 304. TURKEY TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 305. TURKEY TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 306. TURKEY TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 307. TURKEY TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 308. TURKEY TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 309. TURKEY TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 310. UNITED ARAB EMIRATES TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 311. UNITED ARAB EMIRATES TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 312. UNITED ARAB EMIRATES TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 313. UNITED ARAB EMIRATES TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 314. UNITED ARAB EMIRATES TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 315. UNITED ARAB EMIRATES TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 316. UNITED ARAB EMIRATES TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 317. UNITED KINGDOM TIRE MOLD 3D PRINTER MARKET SIZE, BY PRINTER TECHNOLOGY TYPE, 2018-2030 (USD MILLION)

- TABLE 318. UNITED KINGDOM TIRE MOLD 3D PRINTER MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 319. UNITED KINGDOM TIRE MOLD 3D PRINTER MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 320. UNITED KINGDOM TIRE MOLD 3D PRINTER MARKET SIZE, BY AUTOMOTIVE, 2018-2030 (USD MILLION)

- TABLE 321. UNITED KINGDOM TIRE MOLD 3D PRINTER MARKET SIZE, BY COMMERCIAL VEHICLES, 2018-2030 (USD MILLION)

- TABLE 322. UNITED KINGDOM TIRE MOLD 3D PRINTER MARKET SIZE, BY PASSENGER VEHICLES, 2018-2030 (USD MILLION)

- TABLE 323. UNITED KINGDOM TIRE MOLD 3D PRINTER MARKET SIZE, BY USAGE, 2018-2030 (USD MILLION)

- TABLE 324. TIRE MOLD 3D PRINTER MARKET SHARE, BY KEY PLAYER, 2024

- TABLE 325. TIRE MOLD 3D PRINTER MARKET, FPNV POSITIONING MATRIX, 2024

The Tire Mold 3D Printer Market was valued at USD 619.51 million in 2024 and is projected to grow to USD 737.09 million in 2025, with a CAGR of 20.23%, reaching USD 1,871.63 million by 2030.

| KEY MARKET STATISTICS | |

|---|---|

| Base Year [2024] | USD 619.51 million |

| Estimated Year [2025] | USD 737.09 million |

| Forecast Year [2030] | USD 1,871.63 million |

| CAGR (%) | 20.23% |

In recent years, the evolution of additive manufacturing has ushered in a new era for industrial applications, and tire mold 3D printing stands at the forefront of this transformation. This introduction sets the stage by exploring the current technological progress, market dynamics, and the promising future that lies ahead for those invested in innovative manufacturing processes. Advanced 3D printing methods have redefined production capabilities, offering faster turnaround times, increased customization, and improved efficiencies compared to traditional manufacturing techniques.

The tire mold 3D printing market presents an intricate blend of technical sophistication and strategic evolution. It addresses the dual needs of prototyping and production manufacturing by marrying state-of-the-art digital techniques with tried and tested industrial practices. As technological innovations pave the way for deeper insights and diversified applications, this field is proving to be an essential component in shaping the next-generation manufacturing processes. In this context, the focus shifts to comprehending the market's overall potential, the breakthrough trends that continue to revolutionize production practices, and the strategic imperatives needed to succeed in this rapidly growing sector.

Transformative Shifts Driving Market Evolution

The evolution within the tire mold 3D printer market is being driven by groundbreaking innovations and emerging trends that are reshaping the manufacturing landscape. A significant transformative shift is evident in the shift from conventional mold-making techniques to digitally driven processes. This change is not just technological but cultural, fostering an environment where industries are rethinking long-held practices and rapidly embracing digital integration.

Digital transformation in this sector is highlighted by the adoption of advanced printing technologies such as Digital Light Processing (DLP), Fused Deposition Modeling (FDM), Selective Laser Sintering (SLS), and Stereolithography (SLA). These technologies are progressively replacing older, more time-consuming methods of prototyping and production, thereby improving accuracy, reducing waste, and accelerating turnaround times.

At the same time, an increased emphasis on sustainability and cost efficiency has accelerated the adoption of agile manufacturing processes. Progressive market players are using insights from emerging production trends to drive operational efficiencies and meet the increasing global demand for innovative tire molds. The industry, in turn, is witnessing enhanced market responsiveness, where faster design iterations lead directly to higher quality products and improved competitive positioning in a crowded marketplace. The market's evolution underlines the necessity of balancing innovation with practical implementation, creating a fertile landscape for advancement in both industrial production and design versatility.

Navigating Industry Segmentation Insights for Strategic Advantage

Understanding the diverse segmentation within the tire mold 3D printer market is crucial to capturing both current opportunities and future potential. Different aspects of segmentation shed light on various dimensions of market behavior, ultimately guiding better strategic decisions. The market is examined according to printer technology type, where methods such as Digital Light Processing (DLP), Fused Deposition Modeling (FDM), Selective Laser Sintering (SLS), and Stereolithography (SLA) each contribute uniquely to product output and design precision. These technologies are carefully selected based on their specific advantages for either creating detailed prototypes or producing final industrial parts.

Furthermore, the market is defined by the application context, which encompasses both production manufacturing and prototyping. In high-volume production, the ability to maintain precision and consistency is as critical as the streamlined workflow required for rapid prototyping. The segmentation further extends to end-user demographics, incorporating both Aerospace and Automotive sectors. The automotive segment experiences an additional layer of complexity with subdivisions into Commercial Vehicles, which include both heavy commercial vehicles and light commercial vehicles, and Passenger Vehicles that span categories such as convertible, hatchback, sedan, SUV, and van. Each tier of automotive segmentation presents distinct challenges and opportunities, influencing factors such as customization, material compatibility, and speed of production.

An additional dimension of segmentation emerges when looking at usage, distinguishing between the aftermarket and Original Equipment Manufacturers. This bifurcation not only determines the market approach but also influences innovation strategies and customer engagement across various stages of the product lifecycle. Integrating these nuanced insights from diverse segmentation models provides industry players with a comprehensive roadmap to target niche markets, optimize technological deployment, and align product offerings with precise market needs.

Based on Printer Technology Type, market is studied across Digital Light Processing (DLP), Fused Deposition Modeling (FDM), Selective Laser Sintering (SLS), and Stereolithography (SLA).

Based on Application, market is studied across Production Manufacturing and Prototyping.

Based on End-User, market is studied across Aerospace and Automotive. The Automotive is further studied across Commercial Vehicles and Passenger Vehicles. The Commercial Vehicles is further studied across Heavy Commercial Vehicles and Light Commercial Vehicles. The Passenger Vehicles is further studied across Convertible, Hatchback, Sedan, SUV, and Van.

Based on Usage, market is studied across Aftermarket and Original Equipment Manufacturers.

Key Regional Insights Shaping Global Market Opportunities

The global scenario for tire mold 3D printing spans several critical regions, each characterized by distinct market dynamics and regional idiosyncrasies. The Americas have emerged as a powerhouse, propelled by robust manufacturing sectors, substantial industrial investments, and a progressive approach to technology adoption. Driven by consistent innovation and strategic governmental policies, the American market continues to serve as a vital hub for both production manufacturing and advanced prototyping initiatives in the tire mold industry.

Europe, Middle East & Africa collectively represent a dynamic region where a rich confluence of regulatory support and industrial expertise converges with innovative production techniques. European markets benefit not only from advanced technological capabilities but also from stringent quality standards and strong emphasis on sustainability. In the Middle East & Africa, growing industrialization and substantial investments in infrastructure have led to an uptick in the deployment of 3D printing solutions in manufacturing processes, fostering a competitive environment and potentially capturing untapped market segments.

The Asia-Pacific region stands out with its rapid industrialization, high economic growth, and increasingly tech-savvy manufacturing base. Countries in this region are rapidly modernizing their manufacturing methodologies and are keen adopters of emerging technologies such as 3D printing for tire molds. This vibrant ecosystem is supported by a robust supply chain network, innovative research and development, and governmental support, making it a fertile ground for sustained market expansion and competitive advancement in both low-cost and high-performance segments.

Based on Region, market is studied across Americas, Asia-Pacific, and Europe, Middle East & Africa. The Americas is further studied across Argentina, Brazil, Canada, Mexico, and United States. The United States is further studied across California, Florida, Illinois, New York, Ohio, Pennsylvania, and Texas. The Asia-Pacific is further studied across Australia, China, India, Indonesia, Japan, Malaysia, Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam. The Europe, Middle East & Africa is further studied across Denmark, Egypt, Finland, France, Germany, Israel, Italy, Netherlands, Nigeria, Norway, Poland, Qatar, Russia, Saudi Arabia, South Africa, Spain, Sweden, Switzerland, Turkey, United Arab Emirates, and United Kingdom.

Deep Dive into Company-Level Innovations and Market Strategies

The tire mold 3D printer market is notably influenced by a range of pioneering companies that are continually redefining the boundaries of innovation and operational efficiency. These industry leaders have established themselves by offering a diverse portfolio of technologies and solutions that effectively address both large-scale manufacturing requirements and niche market needs. Significant players in the domain include organizations renowned for their commitment to advancing 3D printing capabilities. For instance, companies such as 3D Systems Corp. and Stratasys Ltd. have driven substantial technological breakthroughs, enabling more intricate and efficient print processes. Similarly, Desktop Metal, Inc. and EOS GmbH Electro Optical Systems have been instrumental in integrating metal printing and composite materials into mainstream manufacturing practices.

Other innovators, including BigRep GmbH, Proto Labs, Inc., and Voxeljet AG, have carved out significant market shares by focusing on delivering high-performance solutions that meet the evolving demands of both production manufacturing and prototyping. Similarly, AddUp Group and Eplus3D are broadening the horizon by leveraging their expertise to integrate emerging technologies into traditional systems, while MATERIALISE NV and UnionTech are noted for their specialized solutions that cater to a variety of industries spanning from aerospace to automotive. The SLM So-lu-tions Group AG has also been at the forefront, championing the adoption of metal-based additive manufacturing methodologies that are particularly well-suited to complex industrial applications. These organizational insights provide a valuable context for understanding competitive dynamics and identifying future growth areas within the market.

The report delves into recent significant developments in the Tire Mold 3D Printer Market, highlighting leading vendors and their innovative profiles. These include 3D Systems Corp., AddUp Group, BigRep GmbH, Desktop Metal, Inc., EOS GmbH Electro Optical Systems, Eplus3D, MATERIALISE NV, Proto Labs, Inc., SLM So-lu-tions Group AG, Stratasys Ltd., UnionTech, and Voxeljet AG. Strategic, Actionable Recommendations for Industry Leaders

For decision-makers aiming to secure a competitive edge in the evolving field of tire mold 3D printing, actionable insights translated into strategic initiatives are paramount. Industry leaders should invest in R&D efforts to enhance the precision and speed of advanced printing technologies, ensuring that they not only meet current manufacturing demands but are also prepared for future market disruptions. Leveraging strategic partnerships and collaborations can accelerate technological adoption by integrating complementary expertise, thereby reducing time-to-market and fostering innovation.

A key recommendation is to diversify investment across multiple printer technology types such as Digital Light Processing, Fused Deposition Modeling, Selective Laser Sintering, and Stereolithography. This diversification both hedges risk and allows businesses to tap into the unique benefits offered by each technology. Additionally, companies should adopt a dual-strategy approach by strengthening capabilities in both production manufacturing and prototyping. This ensures that the organization is well-positioned to address varied market demands and is agile enough to pivot based on evolving industry trends.

Moreover, exploring further segmentation across end-user demographics can yield significant benefits. By tailoring solutions to specific market segments such as the Aerospace and Automotive sectors, businesses can offer more targeted products that resonate with customer-specific needs. In the automotive domain, a focused strategy that addresses the nuanced differences within the Commercial and Passenger vehicle segments-ranging from heavy commercial vehicles to convertible and SUV categories-can drive market differentiation.

Finally, companies should be proactive in exploring new geographical markets by leveraging regional strengths. Prioritizing innovation investments in regions characterized by growing industrial bases-such as the Americas, Europe, Middle East & Africa, and Asia-Pacific-will secure long-term sustainability and scalability. Overall, the creation of an agile, innovation-driven organizational structure will not only foster technological leadership but also enhance competitive resilience in a rapidly changing market landscape.

Conclusive Analysis and Future Outlook

The tire mold 3D printer market is positioned at a pivotal juncture, reflecting a confluence of technological advancements, dynamic regional influences, and deep-rooted industry segmentation. In summary, the critical analysis of market trends reveals a scenario where innovative 3D printing technologies are reshaping the way tire molds are designed, produced, and utilized across industries.

The transformation witnessed in this sector is underpinned by a shift towards digitally controlled production, where traditional manufacturing processes are continuously being replaced by more agile, efficient, and cost-effective methods. The segmentation insights provided earlier highlight the diversity within the market, showing that customized technology adoption based on printer type, application context, end-user demographics, and usage patterns is essential for sustainable growth. This multi-layered segmentation model not only reflects the complex interplay between varying production needs but also serves as a strategic guide for companies looking to carve a niche in the competitive landscape.

From a regional perspective, the market's global reach is fostered by economic prowess and industrial readiness in key regions including the Americas, Europe, Middle East & Africa, and Asia-Pacific. Further, the involvement of a multitude of influential companies underlines the robust competitive dynamics and highlights the importance of cross-industry collaboration in driving innovation. Looking ahead, the prospects remain optimistic, with constant technological improvements promising a future where tire mold manufacturing is more accessible, customizable, and aligned with sustainable practices.

Thus, as the industry prepares for continued evolution, the importance of strategic foresight, robust technological infrastructure, and agile market strategies cannot be overstated. The future of tire mold 3D printing will undoubtedly be shaped by those who invest wisely in innovation, foster meaningful partnerships, and maintain a clear strategic focus on the evolving demands and opportunities intrinsic to this dynamic market.

Table of Contents

1. Preface

- 1.1. Objectives of the Study

- 1.2. Market Segmentation & Coverage

- 1.3. Years Considered for the Study

- 1.4. Currency & Pricing

- 1.5. Language

- 1.6. Stakeholders

2. Research Methodology

- 2.1. Define: Research Objective

- 2.2. Determine: Research Design

- 2.3. Prepare: Research Instrument

- 2.4. Collect: Data Source

- 2.5. Analyze: Data Interpretation

- 2.6. Formulate: Data Verification

- 2.7. Publish: Research Report

- 2.8. Repeat: Report Update

3. Executive Summary

4. Market Overview

5. Market Insights

- 5.1. Market Dynamics

- 5.1.1. Drivers

- 5.1.1.1. Growing environmental concerns leading to the adoption of eco-friendly and efficient production methods

- 5.1.1.2. Rising automotive production stimulating the demand for cost-effective tire mold manufacturing

- 5.1.1.3. Increased demand for customized and complex tire designs

- 5.1.2. Restraints

- 5.1.2.1. High initial capital investment requirements for tire mold 3D printing setup

- 5.1.3. Opportunities

- 5.1.3.1. Ongoing advancements in 3D printing technology

- 5.1.3.2. Supportive government initiatives and funding fostering adoption of 3D printing

- 5.1.4. Challenges

- 5.1.4.1. Navigating technical limitations and regulatory issues associated with tire mold 3D printing

- 5.1.1. Drivers

- 5.2. Market Segmentation Analysis

- 5.2.1. Printer Technology Type: Higher adoption of fused deposition modeling for its cost efficiency and material versatility

- 5.2.2. Application: Growing significance of tire mold 3D printer in prototyping innovation and accelerates the time-to-market for new tire mold designs

- 5.3. Porter's Five Forces Analysis

- 5.3.1. Threat of New Entrants

- 5.3.2. Threat of Substitutes

- 5.3.3. Bargaining Power of Customers

- 5.3.4. Bargaining Power of Suppliers

- 5.3.5. Industry Rivalry

- 5.4. PESTLE Analysis

- 5.4.1. Political

- 5.4.2. Economic

- 5.4.3. Social

- 5.4.4. Technological

- 5.4.5. Legal

- 5.4.6. Environmental

6. Tire Mold 3D Printer Market, by Printer Technology Type

- 6.1. Introduction

- 6.2. Digital Light Processing (DLP)

- 6.3. Fused Deposition Modeling (FDM)

- 6.4. Selective Laser Sintering (SLS)

- 6.5. Stereolithography (SLA)

7. Tire Mold 3D Printer Market, by Application

- 7.1. Introduction

- 7.2. Production Manufacturing

- 7.3. Prototyping

8. Tire Mold 3D Printer Market, by End-User

- 8.1. Introduction

- 8.2. Aerospace

- 8.3. Automotive

- 8.3.1. Commercial Vehicles

- 8.3.1.1. Heavy Commercial Vehicles

- 8.3.1.2. Light Commercial Vehicles

- 8.3.2. Passenger Vehicles

- 8.3.2.1. Convertible

- 8.3.2.2. Hatchback

- 8.3.2.3. Sedan

- 8.3.2.4. SUV

- 8.3.2.5. Van

- 8.3.1. Commercial Vehicles

9. Tire Mold 3D Printer Market, by Usage

- 9.1. Introduction

- 9.2. Aftermarket

- 9.3. Original Equipment Manufacturers

10. Americas Tire Mold 3D Printer Market

- 10.1. Introduction

- 10.2. Argentina

- 10.3. Brazil

- 10.4. Canada

- 10.5. Mexico

- 10.6. United States

11. Asia-Pacific Tire Mold 3D Printer Market

- 11.1. Introduction

- 11.2. Australia

- 11.3. China

- 11.4. India

- 11.5. Indonesia

- 11.6. Japan

- 11.7. Malaysia

- 11.8. Philippines

- 11.9. Singapore

- 11.10. South Korea

- 11.11. Taiwan

- 11.12. Thailand

- 11.13. Vietnam

12. Europe, Middle East & Africa Tire Mold 3D Printer Market

- 12.1. Introduction

- 12.2. Denmark

- 12.3. Egypt

- 12.4. Finland

- 12.5. France

- 12.6. Germany

- 12.7. Israel

- 12.8. Italy

- 12.9. Netherlands

- 12.10. Nigeria

- 12.11. Norway

- 12.12. Poland

- 12.13. Qatar

- 12.14. Russia

- 12.15. Saudi Arabia

- 12.16. South Africa

- 12.17. Spain

- 12.18. Sweden

- 12.19. Switzerland

- 12.20. Turkey

- 12.21. United Arab Emirates

- 12.22. United Kingdom

13. Competitive Landscape

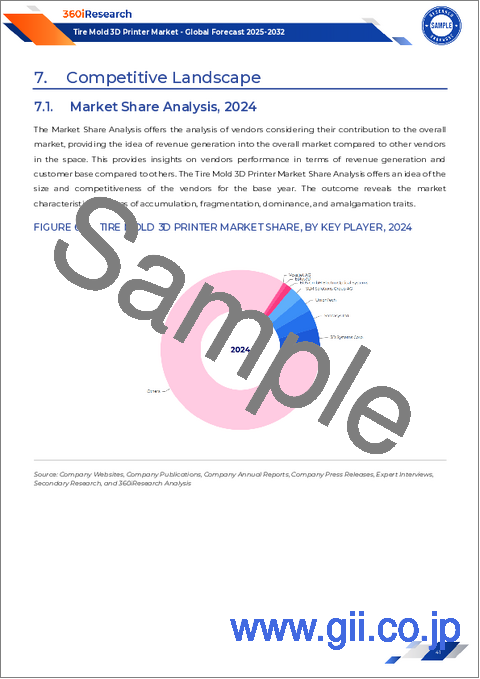

- 13.1. Market Share Analysis, 2024

- 13.2. FPNV Positioning Matrix, 2024

- 13.3. Competitive Scenario Analysis

- 13.3.1. Nexen Tire's 3D printing and XAI integration disrupts traditional mold creation for competitive advantage and sustainability

- 13.3.2. King Machine's adoption of AddUp FormUp 350 transforms tire mold manufacturing with efficiency, and domestic production emphasis

- 13.3.3. TP Tools OY acquires FormUp 350 3D printer for efficiency and design in tire mold manufacturing

- 13.4. Strategy Analysis & Recommendation

Companies Mentioned

- 1. 3D Systems Corp.

- 2. AddUp Group

- 3. BigRep GmbH

- 4. Desktop Metal, Inc.

- 5. EOS GmbH Electro Optical Systems

- 6. Eplus3D

- 7. MATERIALISE NV

- 8. Proto Labs, Inc.

- 9. SLM So-lu-tions Group AG

- 10. Stratasys Ltd.

- 11. UnionTech

- 12. Voxeljet AG