自動車用ルームミラー(IRVM):市場シェア分析、産業動向、成長予測(2025~2030年)

Automotive Inside Rearview Mirrors (IRVM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 80 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690067

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

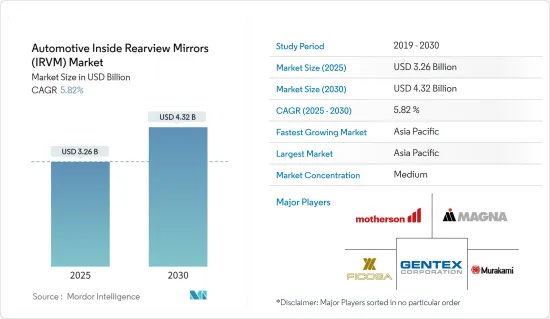

自動車用ルームミラー市場規模は、2025年に32億6,000万米ドルと推定・予測され、予測期間中(2025~2030年)のCAGRは5.82%で、2030年には43億2,000万米ドルに達すると予測されます。

自動車用ルームミラーは、パンデミックの影響を受け、OEMや自動車部品サプライヤーの大半が政府の封鎖措置により生産拠点を閉鎖せざるを得なくなりました。このため、IRVMに対するOEMの需要は低く、メーカーの生産量は減少しました。2021年以降、世界の自動車販売台数の増加と世界のサプライチェーン網の改善により、IRVMの需要は安定し始めました。

さらに、中期的には、乗員の快適性と安全性に対する意識の高まりと、安全機能を義務付ける政府規制を背景に、ADAS機能を統合した自動車の生産台数が増加し、市場の需要を促進すると予想されます。例えば、米国道路安全保険協会(Insurance Institute for Highway Safety)によると、年間1万5,000人が背中越しの事故で負傷しており、幼児や高齢者が最も犠牲になっています。また、米国道路交通安全局(National Highway Traffic Safety Administration)の報告によると、米国では毎年84万件近くの死角事故が発生しています。このため、ドライバーの快適性と安全性を維持するために、車両用IRVMが大いに活用されています。

カメラとセンサは、さまざまな目的を果たすため、新車には欠かせない部品です。OEMがより安全で、より快適な運転ができ、より燃費の良い車を製造するのに役立っています。リアビューカメラやその他の自動車用カメラシステムは、一般に、道路を走る自動車の安全性を向上させる有用なツールとみなされてきました。しかし、ドライバーの視界を広げるはずの複雑なカメラやモニターシステムが、混乱や注意散漫を招くケースもあります。

アジア太平洋は、インド、日本、中国での自動車生産台数の増加により、世界の自動車用ルームミラー市場を独占する可能性が高いです。また、欧州は、Porsche、AUDI、Volkswagen、BMWのような地域の著名な参入企業の存在により、2番目に大きな市場を登録する可能性があります。これらの地域における技術開発は、予測期間中に自動車用ミラー市場に大きな機会を創出すると期待されています。

自動車用ルームミラー市場の動向

乗用車セグメントが市場で大きなシェアを占める見込み

予測期間中、乗用車セグメントは、自動車生産台数の増加や、世界の主要地域における自動車販売台数の増加に伴い、幅広い消費者を魅了する革新的な製品の投入に注力する大手OEMの増加により、より速いペースで成長します。例えば、2021年の世界の自動車販売台数は約6,670万台であり、2020年には6,380万台でした。世界のパンデミックは、自動車販売を含む世界中の経済活動に影響を与え、ウイルスの蔓延を抑えるためにいくつかの国で厳格な封鎖が実施されました。このため、2020年の自動車販売台数は2019年と比較して14.8%減少しました。しかし、生活が正常に戻ったことで、自動車販売台数は世界的に増加しており、自動車用IRVM市場は予測期間中に成長すると考えられます。

乗用車需要の増加と電動モビリティに対する意識の高まりにより、主要企業は現在の保有車両の電動化に期待を寄せています。

- 2022年3月、Ford Motorsは、2024年末までに欧州で全電気乗用車を3車種投入すると発表し、2026年までに欧州で年間60万台以上の電気自動車を販売する目標を設定しました。

- 2022年1月、General Motorsは、電気自動車生産能力を増強するため、ミシガン州の2工場に40億米ドル以上を投資することを検討していると発表しました。GMとLG Energy Solutionは、ランシングに25億米ドルのバッテリー施設を建設することを提案しています。

乗用車セグメントの販売台数の増加に伴い、IRVMの需要は有望な成長を遂げています。現在では、Idセグメントや高級乗用車はすべて先進的なIRVMを搭載しており、市場を技術的に支配しています。例えば

- 2022年8月、Audi Indiaは、いくつかの新技術を採用した新型Q3を発表しました。Audiは、フレームレス自動調光IRVMとリアビューカメラ付きパーキングエイドプラスを追加しました。

- 2022年8月、Tata Punchの印象的な売上を確認した後、Tata Groupは、来年、追加機能を包含するブラックバードと名付けられたクレタセグメントのミッドサイズSUVを発売すると発表しました。この車には、先進的なデジタル計器コンソール、自動調光IRVM、自動空調、電動ORVMなどが装備されます。

自動車用ルームミラー市場は、乗用車セグメントで登場しつつある新しいカメラ技術との厳しい競争に直面しています。主要な自動車メーカーやルームミラーメーカーは、ドライバーの視界を確保するため、従来のミラーにカメラを統合しています。特定の状況では、ミラーを通した車両の後方視界が遮られ、ドライバーの視界に支障をきたします。

そのため、ルームミラーシステムにカメラを統合することが、自動車産業ではこれまでのところ最良の解決策となっています。このような開発と乗用車販売台数増加の要因を考慮すると、IRVMの需要は予測期間中に高い成長率を記録すると予想されます。

予測期間中、アジア太平洋は大幅な成長が見込まれる

アジア太平洋は、低コスト原料の入手可能性、安価な労働力、現地生産に向けた政府の取り組みの増加により、市場で最大のシェアを占めています。同地域では、中国が電気自動車の最大の生産国と消費国のひとつであり、インド、日本、韓国などの国々で乗用車の販売需要が増加していることも、自動車産業におけるルームミラー需要を押し上げる要因となっています。

世界最大の電気自動車市場である中国は、政府からの手厚い支援によって支えられています。中国は、新エネルギー自動車(NEV)購入に関する優遇措置を2022年まで延長しました。アジア太平洋は、電気自動車の導入を積極的に支援しています。例えば

- 2020年1月、Tesla Motorsは上海に20億米ドルの施設を完成させ、2020年3月には、電気自動車大手の他のすべての世界施設がCOVID-19パンデミックのために閉鎖されたときに、週3,000台近くの自動車を組み立てていました。

- 21年度末、Hyundaiは3月に世界で31万3,926台を販売しました。販売統計は前年比17%減となりました。販売台数は2021年第1四半期よりさらに少なかりました。さらに、現代自動車の自動車部門は、電気自動車の販売台数がほぼ倍増し、急成長を遂げました。その結果、BEVの販売台数は105%増の1万1,447台となりました。また、プラグイン電気自動車は1万4,693台となり、前年比58%の伸びとなりました。

市場や未開拓市場の政府・行政は、その富の大部分を交通とその安全性の向上に費やしています。その結果、自動車の販売台数が伸びるとともに、自動車の安全性のニーズに合った追加機能が求められています。IRVMは自動車の販売に大きく依存しているため、アジア太平洋はIRVM採用の中心地となっており、世界中で自動車の販売をリードしています。こうした点を考慮すると、IRVMの需要は予測期間中に高い成長率を示すと予想されます。

自動車用ルームミラー産業概要

自動車市場は、Gentex Corporation、Magna International Inc.、Samvardhana Motherson Reflectecのような多くのローカルと世界参入企業が存在するため、適度にセグメント化されています。

各社は、従来のミラーを交換することなく、自動車所有者により便利で安全な体験を提供するため、研究開発プロジェクトへの投資を増やしています。技術的優位性の高まりとIRVM機能の改善により、市場は大きな成長を遂げています。例えば

- 2022年8月、Mahindra and Mahindraは、上昇中のユーザーの安全性と快適性を向上させるため、自動調光IRVMを搭載した新型Scorpio Nガソリン車を発表しました。

- 2022年7月、SemiDriveはCheryのOMODA 5 SUVがセミドライブのX9シリーズ自動車SoC(システムオンチップ)を採用したと発表しました。X9シリーズは、インストルメントパネル、コンソールコントロール、ルームミラー、後列乗員のエンターテインメントなど、最大10個のHDスクリーンを1チップで出力することができます。マルチスクリーンの共有とインタラクションをサポートします。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場の促進要因

- 市場抑制要因

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 車種別

- 乗用車

- 商用車

- パワートレイン別

- 内燃機関

- 電気

- 機能タイプ別

- 自動調光

- プリズム

- ブラインドスポットインジケーター

- 流通チャネル別

- OEM

- アフターマーケット

- 地域別

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- その他

- ブラジル

- アラブ首長国連邦

- その他の国

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Gentex Corporation

- Samvardhana Motherson Reflectec

- Magna International, Inc.

- Ficosa International SA

- Continental AG

- Murakami Corporation

- Tokai Rika Co., Ltd.

- Mitsuba Corporation

- SL Corporation

- Flabeg Automotive Holding GmbH

第7章 市場機会と今後の動向

目次

The Automotive Inside Rearview Mirrors Market size is estimated at USD 3.26 billion in 2025, and is expected to reach USD 4.32 billion by 2030, at a CAGR of 5.82% during the forecast period (2025-2030).

The Automotive inside rearview mirrors was negatively affected by the pandemic, as majority of OEM and auto component suppliers had to close down their production sites with ongoing government lockdown measures. This held the market with low demand from OEMs for IRVM and reduces production volumes from manufacturers. After 2021, market started witnessing a steady demand for the IRVM with rising auto sales across the globe coupled with an improved supply chain network worldwide.

Moreover, over the medium term, growing production of vehicles with integrated ADAS features in wake of rising awareness toward comfort and safety of passengers and government regulations mandating safety features expected to drive demand in the market. For instance, According to Insurance Institute for Highway Safety says 15,000 people are injured annually in back over accidents, with children and elders having been the most victims. Additionally, the National Highway Traffic Safety Administration report says that nearly 840,000 blind-spot accidents occur every year in the United States. This makes its prime utilization for vehicle IRVM to maintain driver comfort and safety.

Cameras and sensors are a vital part of any new vehicle, as they serve many different purposes. They help OEMs to manufacture cars that are safer, more comfortable to drive, and more fuel-efficient. Rear-view cameras and other camera systems for vehicles have generally been seen as useful tools for improving the safety of vehicles on the road. But in some cases, the complex camera and monitor systems that are supposed to increase the driver's visibility become confusing and distracting.

Asia-Pacific region is likely to dominate global automotive rear view mirror market owing to rising production of vehicle in the India, Japan and China. In addition, this is Europe are likely to register second largest market due to the presence of prominent players in the region for instance, Porsche, AUDI, Volkswagen, and BMW. The technological development in these regions is expected to create significant opportunities in automotive mirror market over the forecast period.

Automotive Rear View Mirror Market Trends

Passenger Car Segment Likely to Hold Significant Share in the Market

The Passenger car segment of the market during the forecast period to grow at faster pace owing to rising vehicle production and growing focus of jey OEMs on launching innovative products to attract wide range of consumers in wake of rising vehicle sales across major regions in the world. For instance, In 2021, the global car sales were around 66.7 Million, which in 2020 were 63.8 Million. The global pandemic impacted economic activities all around the world including car sales the globe, and strict lockdowns were enforced in several countries to contain the spread of the virus. Owing to this the number of cars sold in 2020 was 14.8% lower than compared in 2019. But with life returning to normalcy, the number of cars sold globally has increased which will aid the automotive IRVM market to grow in the forecast period.

Owing to the increase in the demand for passenger cars and the growing awareness of electric mobility, major players are looking forward to electrifying their present fleet. For instance,

- In March 2022, Ford Motors announced to include three all-electric passenger vehicles in Europe by the end of 2024 and set a target to sell more than 600,000 electric vehicles annually by 2026 in the Europe region.

- In January 2022, General Motors announced considering investing more than USD 4 billion in two Michigan factories to increase its electric car manufacturing capacity. GM and LG Energy Solution have proposed constructing a USD 2.5 billion battery facility in Lansing.

With rising sales of the passenger car segment, demand for IRVM is witnessing promising growth. Nowadays, all the id-segment and luxury passenger cars are equipped with advanced IRVM which has posed technological dominance over the market. For instance,

- In August 2022, Audi India has introduced its new Q3 which has adopted several new technologies to look at. Audi has added frameless auto dimming IRVM and parking aid plus with rear view camera, which shall improve the driver safety and comfort apart from other added features in complete Q3.

- In August 2022, after witnessing impressive sales on Tata Punch, Tata Group is announced that ist going to launch a Creta segment mid-size SUV named Blackbird next year which shall encompass added features. The car shall be equipped with advance digital instrument console, auto-dimming IRVM, automatic climate control, electrically operated ORVMs and may more other features.

The automotive inside rear-view mirror market is facing tough competition from new camera technologies with are coming in the passenger car segment. Leading automotive OEMs and interior rear-view manufacturers are integrating cameras with conventional mirrors to provide a better view of the drivers. In certain situations, the rear view of the vehicle through a mirror is blocked and causes hindrance to the driver's view.

Thus, camera integration with the rear-view mirror system has been the best solution so far in the automotive industry. Considering these developments and factors with rising passenger car sales, demand for IRVM is expected to witness a high growth rate in the forecast period.

Asia-Pacific Region Anticipated to Grow at Significant Level During the Forecast Period

The Asia-Pacific region accounts for the largest share in the market owing to the availability of low-cost raw materials, cheap labour, and increasing government initiatives toward local manufacturing. In the region, China is one of the largest producers and consumers of electric vehicles as well as increasing demand for passenger car sales in the countries like India, Japan, South Korea, etc., are likely to boost the demand for inside rear-view mirrors in the automotive industry.

China, which is the largest electric vehicle market in the world, has been backed up by generous support from the government. China has extended the incentives related to the purchase of new energy vehicles (NEVs) till 2022. Asia-Pacific region is aggressively supporting the electrical vehicle adoption. For instance,

- In January 2020, Tesla Motors inaugurated a USD 2 billion facility in Shanghai that was assembling nearly 3000 cars per week in March 2020, when all the other global facilities of the electric vehicle giant were shut down due to the COVID-19 pandemic.

- During the end of FY21, Hyundai sold 313, 926 cars globally in March. The sales statistics stood at a drop of 17% compared to previous years. The sales were even less than Q1 2021. Moreover, Hyundai observed that its automotive segment witnessed a sharp rise with almost doubled sales figures for its all-electric cars. This in turn makes the sales figure for its BEV to stood at 11,447 units with a rise of 105%. In addition, the plug-in electric cars increased to 14,693 units to 58% year and year growth.

Governments and administrations in developing and untapped markets are spending a major portion of their wealth on improving transportation and its safety. This will result in the sales growth of vehicles and also calls for additional features to suit the needs of vehicle safety. With IRVM being highly dependent of sales of the vehicles, Asia-pacific has been leading the vehicles sales across the globe making its epicentre for IRVM adoption. Considering these aspects demand for IRVM is expected to witness high growth rate during the forecast period.

Automotive Rear View Mirror Industry Overview

The automotive market is moderately fragmented due to the presence of many local and global players such as Gentex Corporation, Magna International Inc., and Samvardhana Motherson Reflectec amongst others. The market is transforming but the new technologies are right now available mostly in luxury vehicles and in a selected market and near future, it will not replace the conventional mirrors. As the laws are still with conventional mirrors.

Although companies are increasing investment in R&D projects to provide more convenient and safer experience to the car owner without replacing the conventional mirrors. With rising technological dominance and improved IRVM features market has witnessed immense growth. For instance,

- In August 2022, the Mahindra and Mahindra introduced the new Scorpio N petrol variant with the auto dimming IRVM in order to improve user safety and comfort during the rises.

- In July 2022, SemiDrive announced that Chery's OMODA 5 SUV has adopted SemiDrive's X9 series automotive SoC (system-on-a-chip). The X9 series can provide outputs of up to 10 HD screens, such as instrument panels, console control, rearview mirrors, and entertainment for back row passengers, through a single chip. It supports multi-screen sharing and interaction.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value in USD Million)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Car

- 5.1.2 Commercial Vehicle

- 5.2 By Powertrain Type

- 5.2.1 ICE

- 5.2.2 Electric

- 5.3 By Feature Type

- 5.3.1 Auto-Dimming

- 5.3.2 Prismatic

- 5.3.3 Blind spot indicator

- 5.4 By Sales Channel Type

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 Brazil

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Other Countries

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Gentex Corporation

- 6.2.2 Samvardhana Motherson Reflectec

- 6.2.3 Magna International, Inc.

- 6.2.4 Ficosa International SA

- 6.2.5 Continental AG

- 6.2.6 Murakami Corporation

- 6.2.7 Tokai Rika Co., Ltd.

- 6.2.8 Mitsuba Corporation

- 6.2.9 SL Corporation

- 6.2.10 Flabeg Automotive Holding GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 80 Pages

- 納期

- 2~3営業日