電流センサ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Current Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689937

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

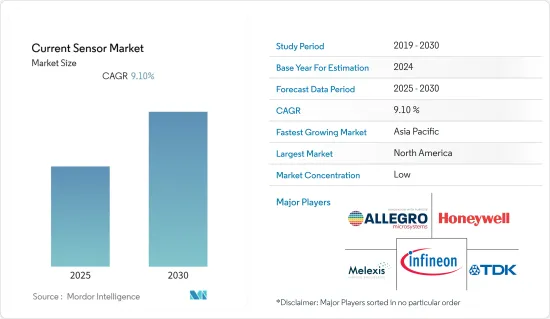

電流センサ市場は予測期間中にCAGR 9.1%を記録する見込みです。

主なハイライト

- 近年、低コスト、高精度、小型の電流センサ・ソリューションに対する需要が、産業、自動車、商業、通信システムなどの分野で高まっています。新しい設計コンセプトと先端技術の体系的な利用により、IC性能のさらなる向上が期待されています。また、電力保護などの追加機能を同じ電流センサICに統合することで、新たな製品アプローチへの道も開かれました。

- 例えば、コンチネンタルAGは2022年5月、高電圧電流センサモジュール(CSM)と、EVバッテリーを安全にするバッテリー衝撃検出(BID)システムを発表しました。厳しい機能安全要件をサポートするため、CSMは2チャンネル・センサとして利用可能で、シャント技術とホール技術をコンパクトな単一ユニットに統合することで電流を独立して測定します。

- スマートフォンの普及が進むことで、予測期間中、電流センサの需要が高まることが予想されます。例えば、エリクソンによると、スマートフォンの契約数は2026年までに12億を突破すると予想されています。5Gは、2026年までにモバイル契約数の26%を占め、重要な促進要因になると予想されています。

- さらに、機械がよりインテリジェントで直感的になるインダストリー4.0革命により、センサの産業用途へのニーズが高まっています。新しいデバイスは、より効率的で安全かつ柔軟に設計され、その性能、使用状況、故障を自律的に監視する機能を備えています。そのため、これらの用途は電流センサの需要に拍車をかけています。IFRの予測によると、国際的な採用は大幅に増加し、2024年までに世界中の工場で51万8,000台の産業用ロボットが稼働すると予想されています。産業用ロボットの需要が良好な成長軌道をたどっていることから、同期間中にセンサの市場が牽引されると予想されます。

- さらに、世界のエネルギー需要に対する懸念の高まりと、環境意識の全体的な高まりに伴い、パワーエレクトロニクス・アプリケーションの設計者は、効率改善を常に迫られています。スマートグリッド、系統連系太陽光発電(PV)、その他の系統連系再生可能エネルギーシステムの出現により、高効率パワーインバータの成長が求められています。国際エネルギー機関の「2050年までのネット・ゼロ・エミッション・シナリオ」によると、2030年までに3億台の電気自動車が普及し、新車販売台数の60%以上を占めることになります。EVやHEVでは電流センサが広く使用されているため、自動車エンドユーザーは今後も電流センサ市場の成長要因の1つになると予測されます。

- IoTとIIoTの大規模な商用化が市場を強化しています。エリクソンによると、セルラーIoTリンクの数は2023年に35億に達すると予測されています。従来の製造業がデジタルトランスフォーメーションを遂げる中、IoTはインテリジェント・コネクティビティの次なる産業革命に拍車をかけています。これは、効率を高め、ダウンタイムを削減するために、ますます複雑化するシステムや機械に対する企業の取り組み方を変革し、電流センサ市場の成長にとって良いシナリオを作り出しています。

- しかし、高電圧スパイク、高温、電流状態の場合の電流センサの規則とともに、製品開拓と電流センサの統合に関連する高コストと技術的限界が、調査した市場の成長を阻む主な課題のいくつかです。

- しかし、ロシアとウクライナの戦争は、半導体を生産する天然ガスと原材料の主要な供給元である半導体のサプライチェーンに影響を与えています。さらに、半導体不足は電流センサ市場にいくつかの影響を与えています。半導体の供給不足は、センサ部品の生産遅延につながる可能性があり、電流センサメーカーにとっては、供給可能な半導体の限られた供給量に対して、より高い価格を支払う必要があるため、コスト増につながる可能性があります。

- さらに、2023年4月、マルチ・スズキ・インディアは、電子部品供給の不確実性が24年度の生産に影響を与える可能性があると述べた。電子部品の供給不足は、2023年度の同社の生産に何らかの影響を与えました。こうした事例は今後も市場の成長を妨げると思われます。

電流センサ市場動向

自動車産業が大きな市場シェアを占める

- 自動車技術の進歩に伴い、各国で電気自動車生産の動向が強く推奨されています。電気自動車の複雑なアーキテクチャ図には、一般的に複数の電流センサが組み込まれています。これに加えて、ブラシレス(BLDC)電気モーターの制御にも電流センサが必要です。BMW、フォルクスワーゲンなどのEV(電気自動車)は、このモーター制御-電流デバイスを使用しています。

- 通常、電流センサは、バッテリー電流監視、太陽光発電インバーター、ミッドハイブリッドおよびフルハイブリッド電気自動車のトラクション・モーターを駆動するパワー・インバーターに見られます。CMOSホール効果ベースの磁気センサは、高度な機能を統合し、高レベルの出力信号機能を提供します。洗練された磁気センサは、プログラマブル・メモリーを保持し、さらにマイクロコントローラー・ロジックにより、完全にカスタム化された出力を可能にします。さらに、EVの他の回路との通信を簡素化する標準インターフェースを実装することも可能です。

- さらに、ハイブリッド電気自動車(HEV)は、急速に最も人気のあるグリーン・カーになりつつあり、車両内の電気エネルギーの流れを制御するために複雑な電子回路を採用しています。単一モーターのHEVでは、モーターは内燃エンジンと並行して駆動モーターとして、あるいは回生ブレーキ時にバッテリーを充電する発電機として機能します。典型的なHEVには、ACモーターやDC-DCコンバーター・アプリケーションなど、最大限の効率で動作させるために電流検出器を必要とする複数のシステムが含まれています。欧州代替燃料観測所(EAFO)によると、ドイツでは2022年に乗用車セグメントでプラグイン電気自動車の新規登録台数が82万3,900台を記録し、バッテリー電気自動車(BEV)の販売台数が約56.36%を占めました。

- アレグロ・マイクロシステムズ(Allegro MicroSystems)のような開発企業は、ハイブリッド電気自動車(HEV)アプリケーションに最適な電流センサ集積回路(IC)ファミリーを幅広く開発しています。その特徴は、120kHzの出力帯域幅、高電流分解能、低ノイズスペクトル密度、電力損失の低減スルーホールコンプライアンス、低抵抗導体集積パッケージを可能にする信号処理とパッケージ設計の革新です。TLE4971は、車載充電器、高電圧補助ドライブ、充電アプリケーション向けです。さらにこのセンサは、電気自動車用DC充電器、産業用ドライブ、サーボドライブ、太陽光発電インバーターなどの産業用アプリケーションにも適しています。

- 有利な政府規制もEV産業の成長に不可欠な役割を果たしており、EV産業は電流センサの主要な消費者として台頭しています。例えば、欧州連合(EU)は2022年初頭に独自の7,500億ユーロ(7,705億米ドル)の景気刺激策を発表したが、その中にはクリーンカーの販売を促進し、2025年までに電気自動車と水素自動車の充電ステーションを約100万基設置するための200億ユーロ(205億米ドル)が含まれています。

- 中国の自動車産業の成長を刺激するために、政府もいくつかのイニシアチブをとっています。例えば、2022年9月、国家税務総局(STA)、財務省(MOF)、工業情報化部(MIIT)は共同で、新エネルギー車の購入に対する免税措置の継続を発表しました。したがって、EVの販売も同様の成長パターンを維持すると予想されるため、予測期間中、国内の自動車業界全体で電流センサの需要もさらに拡大すると見込まれます。

- さらに、2022年10月、BMWグループは、電気自動車とバッテリーを生産するためのアメリカの施設に17億米ドルを投資することを決定しました。このプロジェクトは、隣接するウッドラフに計画されている高電圧バッテリー組立工場への7億米ドルと、サウスカロライナ州にある現在のスパータンバーグ工場をEV製造用に設備するための10億米ドルで構成されます。ドイツの自動車メーカーは、2030年までに米国で少なくとも6台の電気自動車を製造する計画です。

アジア太平洋が大きな成長を遂げる見込み

- アジア太平洋は大きな成長を遂げると予想されています。インド、中国、日本などの新興経済諸国における人口増加と急速な都市化が、この地域の急速な拡大を開始し、エネルギー、自動車、テレコムとネットワーキング、産業、ヘルスケアなどのエンドユーザーからの電流センサに対するニーズを増加させています。IEAによると、2040年までにインドの都市人口が2億7,000万人増加すると推定されています。都市化によって家電製品の所有率が高まるため、エネルギー需要に占める電力の割合はさらに高まると予想されます。

- 家電製品製造者協会によると、インドの家電・民生用電子機器産業は、2024~25年までに1兆4,800億インドルピー(179億米ドル)に倍増すると予測されています。BiCMOSやCMOS技術をベースとした完全集積型でプログラマブルな電流センサの製造が各社で進んでおり、家電製品の生産増加に伴い、これらの電流センサの需要も効果的に増加すると思われます。

- 日本政府は、再生可能産業のインフラ開発にも多額の投資を行っています。2050年までのネット・ゼロ計画を達成するため、政府は数十億米ドル相当のイニシアチブをいくつか打ち出しています。したがって、再生可能エネルギー・インフラへの投資の拡大は、予測期間中、同国における電流センサの需要を促進すると思われます。

- さらに、世界の自動車消費の大部分を占める中国は、2030年までに二酸化炭素排出量を抑制することを約束しました。排出量目標を達成するため、化石燃料で走る自動車の生産削減と販売の合理化を進めています。これにより、電気自動車の需要が増加し、市場の成長が促進されると予想されます。国際クリーン交通評議会(ICCT)によると、2022年上半期を通じて、中国の電気自動車は乗用車登録台数のほぼ4分の1を占め、BEVが19%、PHEVがさらに5%を占めました。

- オーストラリア政府は、国内で再生可能エネルギーの生産を拡大するために、いくつかのイニシアチブを取り始めています。政府は、2050年までに炭素排出量ゼロを達成することを目指しており、これは研究市場ベンダーに大きなビジネスチャンスをもたらすと期待されています。例えば、2022年10月、オーストラリア政府はクリーンエネルギー支出と再生可能エネルギープロジェクトに250億豪ドル(167億米ドル)の予算を割り当てた。さらに、同国政府は200億豪ドル(134億米ドル)を投じ、国の電力網を近代化するための再配線計画を開始しました。

- さらに近年、台湾は半導体チップのトップメーカーとして頭角を現し、カテゴリーによっては中国をしのぐまでになりました。半導体産業の成長に牽引され、台湾の家電産業も牽引力を持ち始めており、AsusやHTCのような企業が世界の家電産業で地位を築いています。

電流センサ産業の概要

電流センサ市場は断片化されており、複数の企業がこの分野で事業を展開しています。主要企業は現在、競争企業間の激しい敵対関係に対応し、コスト競争力のある製品を顧客に提供することに注力しています。主な企業は、Allegro MicroSystems, LLC、TDK Corporation、Infineon Technologies AGなどです。

2023年8月、テキサス・インスツルメンツは、設計を簡素化しながら高精度と高集積化を実現するホール効果電流センサや、シャント抵抗を内蔵した新しい電流シャントモニタなど、新しい電流センシング・ソリューションを発表しました。

2023年 7月、リテルヒューズは新しい電流検出抵抗(CSR)ファミリーの発売を発表しました。このファミリーは、回路内の電流を測定するためのコスト効率の高いソリューションを提供し、バッテリー充電やモーター速度などの機能の電圧監視、制御、電源管理を可能にするとともに、過電流保護も提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- マクロ経済動向の市場への影響評価

第5章 市場力学

- 市場促進要因

- バッテリー駆動および再生可能エネルギーアプリケーションの利用の増加

- IoTとIIoTの大規模商用化

- 市場抑制要因

- センサ部品の平均販売価格下落による新規参入への影響

第6章 市場セグメンテーション

- タイプ別

- ホール効果センサ

- オープンループ

- クローズドループ

- その他のタイプ(スプリットコアホール効果電流センサ)

- 光ファイバ式電流センサ

- 誘導型電流センサ

- ホール効果センサ

- エンドユーザー別

- 自動車

- 民生用電子機器

- テレコムとネットワーキング

- 医療

- エネルギー・電力

- 産業

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- その他のアジア太平洋

- 世界のその他の地域

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Allegro MicroSystems LLC

- TDK Corporation(TDK-Micronas GmbH)

- Infineon Technologies AG

- Melexis NV

- Honeywell International Inc.

- Asahi Kasei Microdevices Corporation

- ABB Group

- NK Technologies

- Tamura Corporation

- Vacuumschmelze GmbH & Co KG

第8章 投資分析

第9章 市場の将来

目次

The Current Sensor Market is expected to register a CAGR of 9.1% during the forecast period.

Key Highlights

- In recent years, the demand for low-cost, accurate, and small-size current sensor solutions has increased across the industrial, automotive, commercial, and communications systems. New design concepts and the systematic utilization of advanced technology have entitled further improvements in IC performance. It has also opened the path to new product approaches by supporting integrating additional functions, such as power protection, in the same current sensor IC.

- For instance, in May 2022, Continental AG launched its high-voltage Current Sensor Module (CSM) and the Battery Impact Detection (BID) system to make EV batteries safe. To support strict functional safety requirements, the CSM is available as a two-channel sensor, measuring current independently by integrating shunt technology and hall technology in a compact, single unit.

- The increasing smartphone penetration is expected to drive the demand for current sensors over the forecast period. For instance, according to Ericsson, smartphone subscriptions are expected to surpass 1.2 billion by 2026. 5G is expected to become a key driving factor, with 26 percent of mobile subscriptions by 2026.

- Further, the Industry 4.0 revolution, in which machines are becoming more intelligent and intuitive, is increasing the need for the industrial applications of sensors. The new devices are designed to be more efficient, safe, and flexible, with the ability to monitor their performance, usage, and failure autonomously. Therefore, these applications spur the demand for current sensors. According to the IFR forecasts, international adoption is anticipated to increase significantly to 518,000 industrial robots operating across plants all around the globe by 2024. The favorable growth trajectory of the industrial robots demand is expected to drive the market for sensors during the same period.

- Furthermore, with the growing concerns about the global demand for energy and the overall augmentation of environmental awareness, designers for power electronics applications are under constant pressure to improve efficiency. The advent of the smart grid, grid-tied photovoltaic (PV), and some other grid-tied renewable energy systems require the growth of high-efficiency power inverters. According to the International Energy Agency's Net Zero Emissions by 2050 Scenario, 300 million electric automobiles will be on the road by 2030, accounting for more than 60 percent of new automobile sales. Because of the widespread usage of current sensors in EVs and HEVs, the automotive end-user is projected to continue to be one of the significator factors for the growth of the current sensor market.

- Large-scale commercialization of IoT and IIoT is bolstering the market. According to Ericsson, the number of cellular IoT links is predicted to reach 3.5 billion in 2023. With the traditional manufacturing sector witnessing a digital transformation, IoT is fueling intelligent connectivity's next industrial revolution. This is transforming the way enterprises approach increasingly complicated systems and machines to enhance efficiency and reduce downtime, creating a good scenario for the growth of the current sensor market.

- However, high cost and technical limitations associated with product development and integration of current sensors integration, along with the rules of current sensors in case of high voltage spikes, high temperature, and current conditions, are some of the major factors challenging the growth of the studied market.

- However, the Russia-Ukraine war is impacting the supply chain of semiconductors, being a major supplier of natural gas and raw materials in producing semiconductors. Additionally, the semiconductor shortage had several impacts on the current sensors market. The shortage of semiconductors could result in delayed production of sensor components, leading to increased costs for current sensor manufacturers, as they may need to pay more increased prices for the limited supply of semiconductors available.

- Moreover, in April 2023, Maruti Suzuki India said that the uncertainties in the electronic component supplies might affect production in FY 24. The shortage of electronic components had some impact on the company's production in FY 2023. Such instances will continue to hamper the growth of the market.

Current Sensor Market Trends

Automotive Industry to Hold Considerable Market Share

- With increased automotive technology advancements, the trends toward electric vehicle production are highly recommended in various countries. A complex architectural diagram of an electric car generally incorporates multiple current sensors. Besides this, current sensors are also needed for brushless (BLDC) electric motor control. The EVs (electronic vehicles) of companies like BMW, Volkswagen, etc. use this motor-control-current device.

- Typically, current sensors are found in battery current monitoring, solar power inverters, and power inverters that drive traction motors in mid and full hybrid electric vehicles. CMOS Hall-effect-based magnetic sensors integrate advanced features and provide high-level output signal functionality. Sophisticated magnetic sensors hold programmable memory, and even microcontroller logic allows for a fully custom-calibrated output. Additionally, it is possible to implement standard interfaces that simplify communication with other circuits in EVs.

- Furthermore, the hybrid electric vehicle (HEV) is quickly becoming the most popular green car and employs complex electronic circuitry to control the flow of electric energy through the vehicle. In a single-motor HEV, the motor acts as a drive motor in parallel with the internal combustion engine or as a generator to charge the battery during regenerative braking. A typical HEV includes multiple systems that require electrical current detectors for maximally efficient operation, including AC motor and DC-DC converter applications. According to the European Alternative Fuels Observatory (EAFO), Germany recorded 823,900 new registrations of plug-in electric cars in the passenger car segment in 2022, with battery electric vehicle (BEV) sales accounting for about 56.36 percent.

- Players like Allegro MicroSystems have developed a broad family of current sensor integrated circuits (ICs) that are ideally suited for hybrid electric vehicles (HEV) applications. The features include signal processing and package design innovations enabling 120 kHz output bandwidth, high current resolution, low noise spectral density, reduced power loss through-hole compliance, and low-resistance integrated conductor packages. Further, in November 2022, Infineon launched an automotive current sensor IC (TLE4971), available in four pre-programmed current ranges: 25, 50, 75, or 120 A. The TLE4971 is intended for onboard chargers, high-voltage auxiliary drives, and charging applications. Moreover, the sensor is also suitable for industrial applications like DC chargers for electric vehicles, industrial drives, servo drives, and photovoltaic inverters.

- Favorable government regulations are also playing an integral role in the growth of the EV industry, which has emerged as a leading consumer of current sensors. For instance, in early 2022, the European Union announced a unique EUR 750 billion (USD 770.5 billion) stimulus package, which includes EUR 20 billion (USD 20.5 billion) to boost the sales of clean vehicles and to install about 1 million electric and hydrogen cars charging stations by 2025.

- To stimulate the growth of the Chinese automotive industry, several initiatives are also being taken by the government. For instance, in September 2022, the State Taxation Administration (STA), the Ministry of Finance (MOF), and the Ministry of Industry and Information Technology (MIIT) jointly announced the continuation of tax exemptions on purchases of new energy vehicles. Hence, with the sales of EVs expected to sustain a similar growth pattern, the demand for current sensors across the country's automotive industry is also expected to grow further during the forecast period.

- Additionally, in October 2022, The BMW Group confirmed the investment of USD 1.7 billion in its American facilities to produce electric automobiles and batteries. The project will consist of USD 700 million for a planned high-voltage battery-assembly plant in the neighboring Woodruff and USD 1 billion to equip the automaker's current Spartanburg manufacturing in South Carolina for the manufacturing of EVs. By 2030, the German manufacturer plans to manufacture at least six all-electric vehicles in the United States.

Asia-Pacific is Expected to Register Significant Growth

- Asia-Pacific is anticipated to account for significant growth. The population growth and rapid urbanization in developing economies, such as India, China, and Japan, have initiated the speedy expansion in the region, which will increase the need for the current sensor from end-users such as energy, automotive, telecom and networking, industrial, and healthcare. According to IEA, an estimated 270 million people will likely be added to India's urban population by 2040. As urbanization leads to a rise in the ownership of consumer appliances, the share of energy demand taken by electricity is expected to grow further.

- According to the Consumer Electronics and Appliances Manufacturers Association, India's appliances and consumer electronics industry is projected to double by INR 1.48 lakh crore (USD 17.9 Billion) by 2024 - 25. As players are manufacturing fully integrated and programmable current sensors based on BiCMOS or CMOS technology, the demand for these current sensors will increase effectively with the increasing production of consumer electronics.

- The Japanese government is also investing significantly in developing renewable industry infrastructure. To achieve its net zero by 2050 plans, the government has launched several initiatives worth multiple billions. Hence, the growing investment in renewable energy infrastructure will drive the demand for current sensors in the country during the forecast period.

- Furthermore, China, responsible for a large portion of global car consumption, pledged to control its carbon emissions by 2030. It has been streamlining the production cuts and sale of cars that run on fossil fuels to meet the emission goals. This is anticipated to increase the demand for electric vehicles, thereby driving market growth. According to the International Council on Clean Transportation (ICCT), throughout the first six months of 2022, electric vehicles in China constituted almost one-fourth of all unique passenger car registrations, with BEVs accounting for 19 percent and PHEVs an additional 5 percent.

- The Australian government has started taking several initiatives to expand the production of renewable power in the country. The government seeks to achieve net zero carbon emissions by 2050, which is expected to create significant opportunities for the studied market vendors. For instance, in October 2022, the Australian government allocated a budget of AUD 25 billion (USD 16.7 billion) for cleaning energy spending and renewable energy projects. Furthermore, the government also launched an AUD 20 billion (USD 13.4 billion), rewiring the Nation's plan to modernize the country's electricity grids.

- Furthermore, in recent years, Taiwan has emerged as the leading semiconductor chip manufacturer and has even outpaced China in some categories. Driven by the semiconductor industry's growth, the consumer electronics industry of the country has also started to gain traction, with companies like Asus and HTC making their place in the global consumer electronics industry.

Current Sensor Industry Overview

The current sensor market is fragmented, with several companies operating in the segment. Significant players are currently focusing on providing customers with cost-competitive products, catering to an intense rivalry in the Market. Key players are Allegro MicroSystems, LLC, TDK Corporation, Infineon Technologies AG, etc.

In August 2023, Texas Instruments introduced new current sensing solutions designed to offer more accuracy and higher integration while simplifying designs, which includes a Hall-effect current sensor that offers the lowest drift in TI's portfolio and new current shunt monitors with a built-in shunt resistor.

In July 2023, Littelfuse Inc. announced the launch of its new Current Sensing Resistor (CSR) family that offers a more cost-effective solution for measuring current within circuits, enabling voltage monitoring, control, and power management of functions such as battery charging and motor speed, while also providing overcurrent protection.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Use of Battery-Powered and Renewable Energy Applications

- 5.1.2 Large Scale Commercialization of IoT and IIoT

- 5.2 Market Restraints

- 5.2.1 Falling Average Selling Prices of Sensor Components Affecting New Market Entrants

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Hall Effect Sensors

- 6.1.1.1 Open Loop

- 6.1.1.2 Closed Loop

- 6.1.1.3 Other Types(Split Core Hall Effect Current Sensor)

- 6.1.2 Fiber Optic Current Sensors

- 6.1.3 Inductive Current Sensors

- 6.1.1 Hall Effect Sensors

- 6.2 By End User

- 6.2.1 Automotive

- 6.2.2 Consumer Electronics

- 6.2.3 Telecom and Networking,

- 6.2.4 Medical

- 6.2.5 Energy and Power

- 6.2.6 Industrial

- 6.2.7 Other End Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Rest of the Asia Pacific

- 6.3.4 Rest of the World

- 6.3.4.1 Latin America

- 6.3.4.2 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Allegro MicroSystems LLC

- 7.1.2 TDK Corporation (TDK-Micronas GmbH)

- 7.1.3 Infineon Technologies AG

- 7.1.4 Melexis NV

- 7.1.5 Honeywell International Inc.

- 7.1.6 Asahi Kasei Microdevices Corporation

- 7.1.7 ABB Group

- 7.1.8 NK Technologies

- 7.1.9 Tamura Corporation

- 7.1.10 Vacuumschmelze GmbH & Co KG

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日