ポリエチレンイミン:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Polyethyleneimine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689934

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

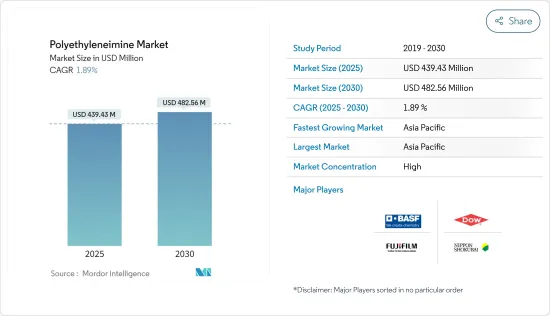

ポリエチレンイミンの市場規模は2025年に4億3,943万米ドルと推定され、予測期間(2025~2030年)のCAGRは1.89%で、2030年には4億8,256万米ドルに達すると予測されます。

COVID-19が市場に与えた影響はマイナスでした。しかし、市場は流行前の水準に達しており、予測期間中は安定した成長が見込まれます。

主なハイライト

- 市場を牽引する主な要因は、洗剤や水処理薬品用途での需要の増加と、接着剤やシーラントでの使用量の増加です。

- 反面、厳しい環境規制が市場の成長を妨げています。

- ポリエチレンイミン-ナノシリカ複合材料の開発や、パーソナルケアおよび化粧品業界の急拡大といった要因は、市場に様々な成長機会をもたらすと予想されます。

- アジア太平洋地域が世界市場を独占しており、中国とインドによる消費が最も大きいです。

ポリエチレンイミン市場の動向

接着剤・シーラント部門が市場を独占

- ポリエチレンイミン(PEI)は、幅広い接着剤・シーラント用途に使用されています。接着剤業界では、接着促進剤としてラミネートに使用されます。また、包装フィルム用の水性プライマーにも使用されています。

- ポリエチレンイミンは、包装業界では押出コーティング用プライマーとして以前から使用されています。特に、ポリエチレンを紙などのセルロース系基材に接着する際に使用されています。実際には、希釈した水または水とアルコールの溶液を塗布します。

- 包装業界は、世界的に接着剤の最大の消費者です。この動向は予測期間中も続くと予測されますが、その主な理由は、飲食品分野における包装用途の旺盛な需要です。

- 接着剤は、包装業界で使用される最も一般的な接着機構のひとつです。ポリエチレンイミンベースの接着剤は、冷凍食品の包装に主に使用されています。このことが包装業界における接着剤需要を押し上げ、市場を後押ししています。

- S&P Globalによると、2021年度のインド国内の接着剤・シーラント市場は1,340億~1,360億インドルピー(18億1,000万~18億3,000万米ドル)です。インドの接着剤・シーラント市場は2つのセグメントに分けられます。工業用セグメントは、包装、履物、塗料、自動車などのB2B産業に対応しています。小売セグメントは、家具/木工、ビル建設、美術工芸、電気継手などの産業に対応しています。

- エレクトロニクス産業は、コンフォーマルコーティング、端子電極の保護、表面実装デバイスの接着など、様々な用途に接着剤を使用しています。エレクトロニクス産業はインドで最も急成長している産業のひとつであり、エレクトロニクス・IT省によると、2021年度の市場規模は4兆9,500億~5兆インドルピー(669億5,000万~676億2,000万米ドル)です。

- 上記の要因から、予測期間中は接着剤・シーラント部門が市場を独占する可能性が高いです。

アジア太平洋地域が市場を独占

- アジア太平洋地域では、ポリエチレンイミンが洗剤、接着剤、水処理薬品、化粧品、製紙などの用途で強く使用されていることから、予測期間中、ポリエチレンイミン市場が支配的となることが予想されます。

- ポリエチレンイミンはパルプ・紙製造の湿潤強化剤として使用されます。中国、インド、東南アジアにおける紙・パルプ産業の成長は、今後も市場の促進要因として作用する可能性があります。

- 中国は、インキ生産において最も急速に成長している国のひとつです。同国のインキ業界は、国際的なインキメーカーと、T&K Tokaとの合弁会社であるHangzhou TOKA InkやToyo Inkとの合弁会社であるTianjin Toyo Inkなどの国内プレーヤーが混在しており、これらは中国における主要な多国籍インキサプライヤーです。また、DIC、Sakata INX、Siegwerk、Flint Group、Hubergroupなどの大手インキメーカーも中国に製造工場を持っています。Yip's Chemicalの子会社であるBauhinia Variegata Ink & Chemicalsは、国内最大のインキメーカーです。

- 洗剤と工業用洗浄剤は、消費者の習慣の変化と家庭での衛生への関心の高まりにより、中国で需要が高まっています。COVID-19の大流行により、中国市場では洗剤と工業用洗浄剤の需要が大幅に増加しました。洗剤と洗浄剤の売上高は2020年に10倍の成長を示しました。2021年には、売上高は400~500%成長しました。

- 石けん製造は、インドのFMCG部門で最も古い産業のひとつであり、消費財部門の50%以上を占めています。最近のデータでは、国内には石鹸を販売する小売店が約500万店あり、そのうち375万店は農村部で営業しています。

- インドとデンマークは、コペンハーゲンで開催された2022年世界水会議・展示会において、「インドの都市廃水シナリオ」に関するホワイトペーパーを発表しました。2021年、インドの都市部における下水発生量は72,368MLDでしたが、下水処理能力は31,841MLDに過ぎませんでした。政府は、昨年発表した「スワチ・バーラト・ミッション2.0(SBM2.0)」の下、下水処理能力の向上を図っています。これにより、水処理におけるポリエチレンイミンの莫大な需要が見込まれます。

- インドの接着剤業界は、その成長性からメーカー各社が投資を行っています。そのため、パイプラインにある新工場や能力拡張は、同国におけるポリエチレンイミンの需要を増加させると予測されます。例えば、2021年12月、Sikaはインドのプネーに新しい技術センターと高品質の接着剤とシーラントの製造工場を開設する計画を発表しました。

- このように、このような要因によってアジア太平洋地域が市場全体を支配することが期待されています。

ポリエチレンイミン産業の概要

ポリエチレンイミン市場は、国際的・国内的企業の存在によって高度に統合されています。主要企業(順不同)には、BASF SE、Nippon Shokubai、Dow、FUJIFILM Wako Pure Chemical Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 洗剤および水処理薬品用途での需要増加

- 接着剤・シーラント用途での用途拡大

- 抑制要因

- 厳しい環境規制

- その他

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ別

- 線形

- 分岐型

- 用途別

- 洗剤

- 接着剤・シーラント

- 水処理薬品

- 化粧品

- 紙

- 塗料、インク、染料

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- Dow

- FUJIFILM Wako Pure Chemical Corporation

- Gongbike New Material Technology(Shanghai)Co. Ltd

- NIPPON SHOKUBAI Co. Ltd

- Polysciences, Inc.

- SERVA Electrophoresis GmbH

- Shanghai Holdenchem Co.

- WUHAN BRIGHT CHEMICAL Co. Ltd

第7章 市場機会と今後の動向

- ポリエチレンイミン・ナノシリカ複合材料の開発

- パーソナルケアと化粧品産業の急拡大

目次

The Polyethyleneimine Market size is estimated at USD 439.43 million in 2025, and is expected to reach USD 482.56 million by 2030, at a CAGR of 1.89% during the forecast period (2025-2030).

The impact of COVID-19 on the market was negative. However, the market has reached pre-pandemic levels and is expected to grow steadily during the forecast period.

Key Highlights

- The major factors driving the market are the increasing demand from applications in detergents and water treatment chemicals and the growing usage in adhesives and sealants.

- On the flip side, stringent environmental regulations are hindering the growth of the market.

- Factors such as the development of polyethyleneimine-nano silica composites and the rapidly expanding personal care and cosmetics industry are expected to offer various growth opportunities for the market.

- Asia-Pacific dominates the market worldwide, with the largest consumption coming from China and India.

Polyethyleneimine Market Trends

Adhesives and Sealants Segment to Dominate the Market

- Polyethyleneimine (PEI) is used for a wide range of adhesive and sealant applications. It is used for laminations in the adhesives industry as an adhesion promoter. It is also used in water-based primers for packaging films.

- Polyethyleneimine has been used for some time as an extrusion coating primer in the packaging industry. It has particularly found use in bonding polyethylene to paper and other cellulosic substrates. In practice, it is applied with diluted water or water-alcohol solutions.

- The packaging industry is the largest consumer of adhesives globally. This trend is estimated to continue during the forecast period, primarily due to the robust demand for packaging applications in the food and beverage sector.

- Adhesives are one of the most common bonding mechanisms used in the packaging industry. Polyethyleneimine-based adhesives are used majorly in the packaging of frozen food products. This factor boosts the demand for adhesives in the packaging industry, thus driving the market studied.

- According to S&P Global, India's domestic adhesives and sealants market is INR 134-136 billion (~USD 1.81-1.83 billion) in fiscal year 2021. Indian adhesives and sealant market is divided into two segment. The industrial segment caters to B2B industries such as packaging, footwear, paints, automotive, etc. The retail segment caters to industries such as furniture/woodwork, building construction, arts and craft, electrical fittings, etc.

- The electronics industry uses adhesives for various applications, including conformal coatings, protecting terminal electrodes, bonding of surface mount devices, among many others. The electronics industry is one of the fastest-growing industries in India and, as per the Ministry of Electronics and IT, the market size of the industry is INR 4,950-5,000 billion (~ USD 66.95-67.62 billion) as of fiscal 2021.

- Based on the above-mentioned factors, the adhesive and sealants segment is likely to dominate the market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the market for polyethyleneimine during the forecast period, as polyethyleneimine is strongly used in applications, such as detergents, adhesives, water treatment chemicals, cosmetics, and paper, in the region.

- Polyethyleneimine is used as a wet strengthening agent in pulp and paper manufacturing. The growing paper and pulp industry in China, India, and Southeast Asia may continue to act as a driver for the market studied.

- China is one of the fastest-growing countries in terms of ink production. The country's ink industry is a mix of international ink manufacturers and domestic players, including Hangzhou TOKA Ink, a JV with T&K Toka, and Tianjin Toyo Ink Co. Ltd, a JV with Toyo Ink, which are the leading multi-national ink suppliers in China. DIC, Sakata INX, Siegwerk, Flint Group, Hubergroup, and other major ink companies also have manufacturing plants in China. The Bauhinia Variegata Ink & Chemicals, a subsidiary of Yip's Chemical, is the largest domestic ink producer in the country.

- The detergents and industrial cleaning agents are gaining demand in China due to changing consumer habits and growing attention toward hygiene at home. Due to the COVID-19 pandemic, the Chinese market witnessed a huge rise in demand for detergent and industrial cleaning agents. The sales revenue for detergents and cleaning agents witnessed a ten-fold growth in 2020. In 2021, the sales grew by 400-500%.

- Soap manufacturing is one of the oldest industries operating in the FMCG sector in India, accounting for more than 50% of the consumer goods sector. As per recent data, there are approximately five million retail outlets selling soaps in the country, of which 3.75 million operate in rural areas.

- India and Denmark together launched a whitepaper recently on 'Urban Wastewater Scenario in India' at World Water Congress and Exhibition 2022 in Copenhagen. In 2021 India's sewage generation was 72,368 MLD in urban centres, whereas the installed sewage treatment capacity was only 31,841 MLD. The government is trying to increase the sewage treatment capacity under the government Swachh Bharat Mission 2.0 (SBM 2.0), which was announced last year. This is expected to create a huge demand for polyethyleneimine in water treatment.

- The manufacturers have been investing in the Indian adhesives industry due to its growth potential. Thus, new plants and capacity expansions in the pipeline are projected to increase the demand for polyethyleneimine in the country. For instance, in December 2021, Sika announced its plans to open a new technology center and manufacturing plant for high-quality adhesives and sealants in Pune, India.

- Thus, such factors are expected to help the Asia-Pacific region dominate the overall market.

Polyethyleneimine Industry Overview

The polyethyleneimine market is highly consolidated with the presence of international and domestic players. The major companies (in no particular order) include BASF SE, Nippon Shokubai Co. Ltd, Dow, and FUJIFILM Wako Pure Chemical Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand from Applications in Detergents and Water Treatment Chemicals

- 4.1.2 Growing Usage in Adhesive and Sealant Applications

- 4.2 Restraints

- 4.2.1 Stringent Environment Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 Market Segmentation (Market Size in Revenue)

- 5.1 Type

- 5.1.1 Linear

- 5.1.2 Branched

- 5.2 Application

- 5.2.1 Detergents

- 5.2.2 Adhesives and Sealants

- 5.2.3 Water Treatment Chemicals

- 5.2.4 Cosmetics

- 5.2.5 Paper

- 5.2.6 Coatings, Inks, and Dyes

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Ranking Analysis

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Dow

- 6.3.3 FUJIFILM Wako Pure Chemical Corporation

- 6.3.4 Gongbike New Material Technology (Shanghai) Co. Ltd

- 6.3.5 NIPPON SHOKUBAI Co. Ltd

- 6.3.6 Polysciences, Inc.

- 6.3.7 SERVA Electrophoresis GmbH

- 6.3.8 Shanghai Holdenchem Co.

- 6.3.9 WUHAN BRIGHT CHEMICAL Co. Ltd

7 Market Opportunities and Future Trends

- 7.1 Development of Polyethyleneimine-nano Silica Composites

- 7.2 Rapidly Expanding Personal Care and Cosmetics Industry

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日