|

市場調査レポート

商品コード

1689928

英国の建設:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)UK Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の建設:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

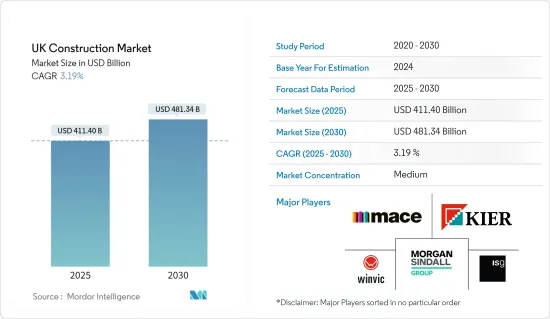

英国の建設市場規模は2025年に4,114億米ドルと推定され、予測期間(2025年~2030年)のCAGRは3.19%で、2030年には4,813億4,000万米ドルに達すると予測されています。

英国全土における建築活動の活発化が市場を牽引しています。さらに、商業活動の活発化も市場を後押ししています。全般的な動向が大幅な拡大を示しているとはいえ、英国の建設業界は最近、数々の困難に直面しています。インフレとロシアのウクライナ侵攻はサプライチェーンを混乱させ、建築資材の価格を押し上げました。

英国の建設生産高が良好な伸びを示すなど、大幅な回復を見せています。英国国家統計局によると、2022年の英国の新規建設工事(現行価格)は過去最高の1,329億8,900万ポンド(1,680億2,700万米ドル)に達し、その主な要因は、国内工事が140億9,300万ポンド、公共工事が40億6,800万ポンド(51億3,800万米ドル)に上ったことです。

また、2022年の新規建設受注額は11.4%増の808億3,700万ポンド(1,021億1,600万米ドル)となり、民間インフラ、民間企業、その他公共非住宅部門が牽引しました。

英国では、2022年の建設関連従業員(自営業を除く)は140万人で、2021年比で3.3%増加しました。イングランドが3.5%増と最も大きく、次いでウェールズとスコットランドがそれぞれ2.0%増となりました。

英国の建設市場の動向

建設業のGVAの増加が市場を牽引

英国は建設市場において確固たる競争力を有しています。英国は建築、設計、エンジニアリングの分野で世界トップクラスの専門知識を有し、英国企業は建築物の持続可能性ソリューションで業界をリードしています。

世界経済の変化は、英国に新たなチャンスをもたらしています。政府は、英国企業の成長と、復興促進のための世界規模での競争への意欲、信頼、推進力を支援します。このアジェンダには、計画制度の改革、重要なインフラ・プロジェクトの資金調達の確保、Funding for Lending SchemeやHelp-to-Buy Equity Loan Schemeのような重要なイニシアティブを通じた住宅市場の支援が含まれます。

英国国家統計局によると、2023年第1四半期における英国の建設部門の粗付加価値額(GVA)は376億3,000万ポンド(475億5,000万米ドル)でした。この部門のGVAは、COVID-19の大流行により2020年第2四半期には200億GBP(256億米ドル)まで落ち込み、この10年間で最低を記録しました。英国の建設セクターの全産業の中で、民間住宅が最も収益を上げています。

民間住宅が英国の建設市場で最大のシェアを占める

民間住宅は、英国の建設市場で最も大きなシェアを占めている分野です。とはいえ、英国国家統計局のデータによれば、住宅と非住宅の修繕・メンテナンスを合わせた2022年の建設生産高は、ほぼ39%に達しました。過去数年間、インフラの生産量は増加し、商業ビルの建設を上回りました。

イングランドでは、民間賃貸住宅の世帯数が徐々に増加しています。業界の専門家によると、2023年の民間賃貸世帯の割合は18.8%で、約460万世帯が民間賃貸であると推定されています。また、英国では住宅の平均価格が著しく上昇しています。

英国国家統計局によると、2023年1月までの12ヵ月間の民間賃貸価格は4.4%上昇し、2022年12月までの12ヵ月間の4.2%から上昇しました。2023年1月までの12ヵ月間、年間民間賃貸価格はウェールズで3.9%、イングランドで4.3%、スコットランドで4.5%上昇しました。イングランドでは、2023年1月までの12ヶ月間で民間賃貸価格の年間変動率が最も高かったのはイースト・ミッドランズで5.0%、最も低かったのはウエスト・ミッドランズで3.9%でした。また、2023年1月までの12ヵ月間におけるロンドンの民間賃貸価格の年間変動率は4.3%でした。

英国の建設業界の概要

英国の建設市場は部分的に断片化されており、多くの地域・地元企業と少数の世界企業が存在します。また、予測期間中、住宅建設と運輸建設分野には大きな成長の可能性があり、市場企業のビジネスチャンスを刺激しています。主な企業は、Kier Group PLC、Morgan Sindall Group PLC、Mace Limited、Winvic Ltd、ISG PLCです。また、英国では建設への投資が増加しており、今後の大型プロジェクトも予定されていることから、予測期間中に市場は成長すると予測されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 促進要因

- 交通インフラへの投資

- 抑制要因

- 熟練労働者の不足

- 機会

- バーミンガム・ビッグシティ計画

- バリューチェーン/サプライチェーン分析

- 産業の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場の洞察

- 現在の経済と建設市場のシナリオ

- 建設分野における技術革新

- 政府の規制と取り組みが業界に与える影響

- 英国における今後のインフラプロジェクトと進行中のプロジェクトに関する洞察

- COVID-19が市場に与える影響

第6章 市場セグメンテーション

- セクター別

- 住宅市場

- 商業用

- 工業用

- インフラ

- エネルギー・公益事業

- 主要地域別

- イングランド

- 北アイルランド

- スコットランド

- ウェールズ

第7章 競合情勢

- 企業プロファイル

- Kier Group PLC

- Morgan Sindall Group PLC

- Mace Ltd

- Winvic Group

- ISG PLC

- Bouygues UK

- Balfour Beatty PLC

- Galliford Try PLC

- Keller Group PLC

- Laing O'Rourke PLC*

- その他の企業

第8章 市場の将来

第9章 付録

The UK Construction Market size is estimated at USD 411.40 billion in 2025, and is expected to reach USD 481.34 billion by 2030, at a CAGR of 3.19% during the forecast period (2025-2030).

The increasing building activities across the United Kingdom are driving the market. Furthermore, the market is being propelled by growing commercial activities. Even though the general trends point to significant expansion, the UK construction industry has recently faced numerous difficulties. Inflation and Russia's invasion of Ukraine have disrupted the supply chain and pushed up the price of building materials.

There has been a significant recovery, with favorable growth rates in the United Kingdom's construction output. According to the Office for National Statistics UK, the value of new construction works in current prices in Great Britain reached a record high of GBP 132,989 million (USD 168,027 million) in 2022, which was mainly due to an increase in both domestic and public sector work amounting to GBP 14,093 million and GBP 4,068 million (USD 5,138 million), respectively.

In addition, new construction orders increased by 11.4% to GBP 80,837 million (USD 102,116 million) in 2022, driven by private infrastructure, private businesses, and other public non-housing, with industrial being the only sector that registered a decline.

In Great Britain, construction-related employees (excluding self-employment) totaled 1.4 million in 2022, an increase of 3.3% compared to 2021. England had the most significant increase in construction-related employees, amounting to 3.5%, followed by Wales and Scotland registering a 2.0% increase each.

UK Construction Market Trends

Increase in GVA of Construction Industry Driving the Market

The United Kingdom has a solid competitive edge in the construction market. The United Kingdom has world-class expertise in architecture, design, and engineering, and British companies lead the way in sustainability solutions for buildings.

The changes in the global economy create new opportunities for Britain. The government supports the growth of British companies and their aspirations, trust, and drive to compete on a global scale to promote recovery. This agenda includes reforming the planning system, ensuring that vital infrastructure projects are financed, and supporting the housing market through critical initiatives like the Funding for Lending Scheme and the Help-to-Buy Equity Loan Scheme.

The gross value added (GVA) by the construction sector in the United Kingdom in the first quarter of 2023 was GBP 37.63 billion (USD 47.55 billion), according to its Office for National Statistics. The GVA of this sector dropped to GBP 20 billion (USD 25.6 billion) in Q2 of 2020 due to the COVID-19 pandemic, marking the sector's lowest point in a decade. Out of all the industries in the UK construction sector, private housing was the one that made the most money.

Private Housing Holds the Largest Share in the UK Construction Market

Private housing was the segment that held the most significant share of the UK construction market. Nevertheless, housing and non-housing repair and maintenance together amounted to almost 39% of the construction output in 2022, according to data from the UK Office for National Statistics. The output volume of infrastructure grew during the past years, surpassing the construction of commercial buildings.

There has been a gradual increase in the number of households occupied by private renters in England. According to industry experts, the share of households occupied by private renters in 2023 was estimated to be 18.8%, with around 4.6 million households being privately rented. There has also been a marked increase in the average price of homes in the United Kingdom.

In the United Kingdom, private rental prices increased in the 12 months to January 2023 by 4.4%, up from 4.2% in the 12 months to December 2022, according to the Office of National Statistics. From 12 months to January 2023, the annual private rental price increased by 3.9% in Wales, 4.3% in England, and 4.5% in Scotland. In England, the East Midlands had the highest annual percentage change over 12 months to January 2023 in private rental prices of 5.0%, while the West Midlands recorded the lowest change at 3.9%. Also, in the 12 months until January 2023, London's yearly percentage change in private renting prices was 4.3%.

UK Construction Industry Overview

The UK construction market is partially fragmented, with the presence of many regional and local players and a few global companies. In addition, there is a vast potential for growth in the residential and transport construction segments during the forecast period, stimulating opportunities for market players. Key players are Kier Group PLC, Morgan Sindall Group PLC, Mace Limited, Winvic Ltd, and ISG PLC. In addition, due to the increasing investments in construction and future large projects in the United Kingdom, the market is projected to grow during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Drivers

- 4.2.1 Investments in Transport Infrastructure

- 4.3 Restraints

- 4.3.1 Shortage of Skilled Labor

- 4.4 Opportunities

- 4.4.1 The Birmingham Big City Plan

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET INSIGHTS

- 5.1 Current Economic and Construction Market Scenario

- 5.2 Technological Innovations in the Construction Sector

- 5.3 Impact of Government Regulations and Initiatives on the Industry

- 5.4 Insights into Upcoming and Ongoing Infrastructure Projects in the United Kingdom

- 5.5 Impact of COVID-19 on the Market

6 MARKET SEGMENTATION

- 6.1 By Sector

- 6.1.1 Residential

- 6.1.2 Commercial

- 6.1.3 Industrial

- 6.1.4 Infrastructure

- 6.1.5 Energy and Utilities

- 6.2 By Key Regions

- 6.2.1 England

- 6.2.2 Northern Ireland

- 6.2.3 Scotland

- 6.2.4 Wales

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Kier Group PLC

- 7.1.2 Morgan Sindall Group PLC

- 7.1.3 Mace Ltd

- 7.1.4 Winvic Group

- 7.1.5 ISG PLC

- 7.1.6 Bouygues UK

- 7.1.7 Balfour Beatty PLC

- 7.1.8 Galliford Try PLC

- 7.1.9 Keller Group PLC

- 7.1.10 Laing O'Rourke PLC*

- 7.2 Other Companies