|

市場調査レポート

商品コード

1910723

ヨウ素:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Iodine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヨウ素:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

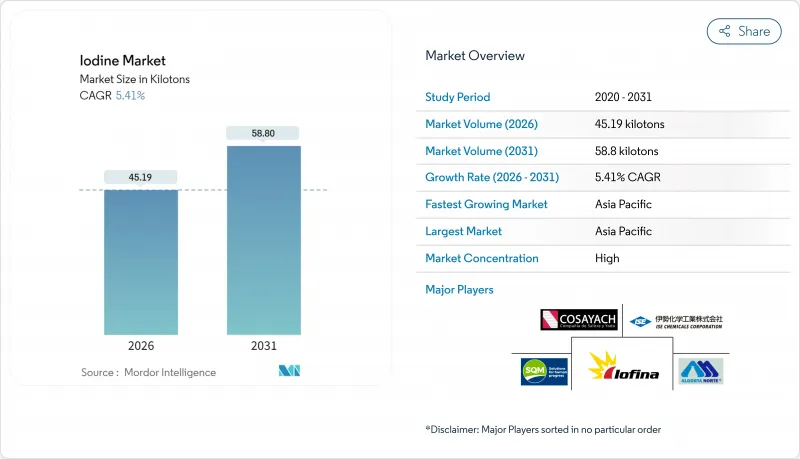

2026年のヨウ素市場規模は45.19キロトンと推定され、2025年の42.87キロトンから成長が見込まれます。

2031年の予測値は58.8キロトンで、2026年から2031年にかけてCAGR5.41%で拡大する見通しです。

この数量増加は、X線/CT画像診断、液晶・有機EL用偏光板、畜産衛生製品、特殊化学品など、いずれも費用対効果の高い代替品が存在しない分野におけるヨウ素の代替不可能な役割を反映しています。医療画像診断が依然として需要の基幹を支える一方、WET IOsorbなどの地下塩水抽出技術は生産コストを引き下げ続け、チリ産カリチェ鉱資源の優位性を薄れさせています。アジア太平洋地域は、中国の電子機器製造とインドの診断能力拡大を背景に消費を牽引していますが、同地域の輸入依存度の高さが供給混乱への脆弱性を増幅させています。2022-2023年の供給不足に続く世界の在庫逼迫を受け、下流ユーザーは長期契約の締結、スポット価格の安定化、リサイクル推進により、予測可能性は高まったもの依然として脆弱な需給バランスを形成しています。

世界のヨウ素市場の動向と展望

X線/CT造影剤の需要増加

世界の診断業務量は増加を続けており、2023年だけで1,000万件を超えるメディケア造影CT検査が実施されたことは、供給ショックがもたらすコストを如実に示しています。契約造影剤メーカーは、アイルランド拠点の生産能力拡大や、プレミアム価格であってもヨウ素供給を確保する複数年原料契約の締結により対応しています。個別投与量や多回投与バイアルを重視する持続可能性への取り組みにより、成長は「検査件数当たり」の強度モデルから「検査件数」ベースのモデルへと移行しつつあり、これが長期的な需要を安定化させています。病院側は、2011年に1kgあたり100米ドル超まで価格を押し上げたスポット市場の急騰から身を守るため、供給先の多様化を同時に進めています。インドや東南アジア全域で放射線科が近代化されるにつれ、ヨウ素市場は成熟経済圏の飽和状態を相殺する追加的な構造的追い風を得ています。

増加するヨウ素欠乏症

最新の調査では、インドの全世帯における食塩ヨウ素添加率(ユニバーサルソルトヨウ素化)は92.4%に達しましたが、妊婦や授乳婦における軽度の欠乏症は依然として存在しており、強化措置だけでは十分な摂取量を保証できないことが明らかになりました。中国の2025年版食事摂取基準改訂は、残存する栄養格差を埋めるため、徐放性肥料やバイオ強化作物への依存度を高める地域特化型栄養戦略の有効性をさらに裏付けるものです。米国食品医薬品局(FDA)から香港食品安全センターに至る規制当局は、単回摂取量で400マイクログラムを超えるヨウ素を含む海藻スナックによる偶発的な過剰摂取を防ぐため、同時に表示規則を強化しています。こうした並行する動向は、食品加工用医薬品グレードヨウ素酸塩の着実な数量成長を支えると同時に、非医療需要を生み出す徐放性肥料コーティング技術の開発を促進しています。

毒性懸念と処理コスト

米国労働安全衛生局(OSHA)は職場のヨウ素蒸気濃度を0.1ppmに制限し、米国産業衛生専門家会議(ACGIH)はさらに厳しい0.01ppmを推奨しているため、加工業者はスクラバー、隔離ブース、継続的モニタリングへの投資が求められます。同時に、米国環境保護庁(EPA)によるヨウ素系抗菌剤の再登録判断は継続的に進展しており、配合業者にはより環境に優しい溶剤への移行と追加の毒性学資料提出が要求されています。医療用同位体は少量であるにもかかわらず、追加の放射線安全プロトコルを必要とし、統合生産者の間接費を増加させます。これらの規制対応要件が相まって、新規参入者のコスト下限を引き上げ、規制インフラが限られた地域ではプロジェクト認可の遅延要因となり得ます。

セグメント分析

2025年時点でカリチェ鉱石は世界供給量の50.72%を占め、ヨウ素市場の過半数を占めておりますが、ブラインプロジェクトの普及に伴い相対的なシェアは低下傾向にあります。同セグメントの鉱石2,500kg当たり1kgの生産比率に加え、チリにおける水使用量の監視強化が、より簡便な酸化・抽出工程を提供する地下ブラインに対する競争力を損なう要因となっております。地下塩水抽出はCAGR5.55%で拡大しており、既存の石油・ガスインフラを活用することで設備コストを最小限に抑えつつ単位エネルギー消費量を削減。これにより最速成長供給ルートとしての地位を強化しています。電子部品用偏光フィルムのリサイクルは生産量こそ未成熟ながら技術的には実現可能であり、回収コストの低下に伴い再生ヨウ素がニッチな高純度需要を賄うことで、初使用時の消費急増を緩和する可能性があります。海藻ベースの抽出は現在、特殊なニッチ市場であり、「生物由来」の認証を重視する健康食品・栄養補助食品メーカー向けに供給されていますが、主要な工業用供給源と比較すると生産量は依然として小規模です。

ヨウ素レポートは、供給源別(地下塩水、カリチェ鉱石、海藻、リサイクル)、形態別(元素及び同位体、無機塩及び錯体、有機化合物)、エンドユーザー産業(飼料、医療、殺菌剤、光学偏光フィルムなど)、地域(北米、南米、欧州、アジア太平洋、中東・アフリカ)ごとに分析されています。市場予測は数量(キロトン)単位で提供されます。

地域別分析

アジア太平洋地域は2025年にヨウ素市場の34.27%を占め、6.82%のCAGRで成長しています。これは中国の電子機器エコシステム、堅調な造影剤需要、公衆衛生強化プログラムに支えられています。中国の最新五カ年計画では診断能力の拡充が目標とされており、国内の鉱石・塩水プロジェクトが頭打ちとなる中でも原料需要は持続すると見込まれます。インドではCT検査件数の高い伸びと規制されたヨウ素添加塩プログラムにより需要が維持され、医薬品グレードヨウ素酸塩の主要な新規消費国としての地位を確立しています。

北米市場は成熟しつつも堅調な推移を示しており、オクラホマ州とユタ州における米国塩水事業が基盤となっています。同地域では安定した垂直統合戦略により輸入リスクが軽減されています。モジュール式抽出装置への最近の投資は、重要鉱物サプライチェーンの現地化を推進する政策を反映しており、この動向は2024年のIO#10施設稼働開始によりさらに強化される見込みです。

欧州では厳格な食品安全基準と職業曝露規制が維持され、乳児栄養食品や医薬品向け高純度ヨウ素酸塩の需要を牽引しています。ドイツ、フランス、英国が地域消費を支える一方、乳製品分野の残留基準値が成長に自然な抑制要因となっています。抗菌薬耐性対策に向けた規制強化の動きにより、クロルヘキシジン代替品の審査が進む中、病院用消毒剤におけるヨウ素使用がさらに増加する可能性があります。

南米はチリの輸出に依存しており、消費量よりも供給量を支配しています。ブラジルとアルゼンチンでは医療支出や農薬需要の増加に伴い国内消費が伸びていますが、地域の純輸出は依然として堅調にプラスを維持しています。中東・アフリカ地域は絶対トン数では最小規模ながら、湾岸諸国の病院では二桁の手術件数増加を記録し、地域の栄養不足を補うためのヨウ素肥料の初期試験が実施されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- X線・CT造影剤の需要増加

- ヨウ素欠乏症の増加

- LCDおよびOLED用偏光板の生産拡大

- 家畜用消毒剤の使用増加

- 直接塩水抽出によるコスト優位性

- 市場抑制要因

- 毒性に関する懸念と取り扱いコスト

- カリチェ由来ヨウ素の価格変動性

- 乳製品中の残留ヨウ素に対する規制上の制約

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- ソース別

- 地下塩水

- カリチェ鉱石

- 海藻

- リサイクル

- 形態別

- 元素及び同位体

- 無機塩及び錯体

- 有機化合物

- 最終用途産業別

- 動物飼料

- 医療(X線造影剤、医薬品、ヨードフォア及びポビドンヨード)

- 殺菌剤

- 光学偏光フィルム

- フッ素化学品

- ナイロン

- その他のエンドユーザー産業

- 地域別

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)**/順位分析

- 企業プロファイル

- Algorta Norte

- Calibre Chemicals Pvt. Ltd.

- Cosayach

- Deep Water Chemicals

- Eskay Iodine

- Glide Chem Private Limited

- Godo Shigen Co. Ltd

- Infinium Pharmachem Limited

- Iochem Corporation

- Iofina plc

- ISE CHEMICALS CORPORATION

- K&O Energy Group Inc.

- Nippoh Chemicals Co. Ltd

- Parad Corporation Pvt Ltd

- Proto Chemical Industries

- Salvi Chemical Industries Ltd

- Samrat Pharmachem Limited

- SQM

- TOHO EARTHTECH,INC

- Woodward Iodine LLC