亜鉛化合物:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Zinc Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689904

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

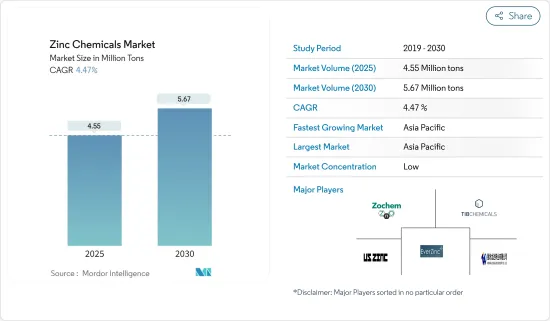

亜鉛化合物の市場規模は2025年に455万トンと推計され、予測期間(2025-2030年)のCAGRは4.47%で、2030年には567万トンに達すると予測されます。

COVID-19の発生は、建設、石油化学、その他の産業に短期的・長期的な影響をもたらし、世界中の亜鉛化合物市場に影響を与えました。しかし現在、市場は大流行前の水準に戻っています。

主なハイライト

- 短期的には、自動車産業における利用率の上昇とゴムタイヤ産業からの需要増加が亜鉛化合物市場の成長を牽引すると思われます。

- その反面、亜鉛ベースの化学薬品に関連する健康被害などの要因が市場の成長を妨げると予想されます。

- がんの診断、画像化、治療に使用される亜鉛ナノ粒子の分野における新たな調査と技術の進歩は、今後数年間、亜鉛市場に大きな機会を提供すると予想されます。

- アジア太平洋地域が市場を独占しており、予測期間中も支配し続けると予想されます。

亜鉛化合物市場の動向

市場を独占するゴム加工セグメント

- 亜鉛めっきとタイヤ製造における亜鉛化合物の大量消費により、ゴム加工セグメントが市場を独占しています。

- 亜鉛化学薬品は、自動車で一般的に使用されるタイヤやチューブの製造に広く使用されています。成長する自動車産業は、まもなく亜鉛化合物の全体的な需要を増大させると予想されます。

- 国際ゴム研究グループ(IRSG)によると、天然ゴムの世界生産量は2023年上半期に約650万トンに達し、約680万トンだった2000年に比べて大幅に増加しました。

- 天然ゴム生産国協会(ANRPC)によると、2023年3月の天然ゴムの世界需要は、同時期に7.9%増の130万6,000トンに達しました。

- 電気自動車の普及が自動車用タイヤの需要を押し上げ、自動車産業におけるタイヤの消費を促進し、それが亜鉛化合物市場を牽引すると予想されます。

- また、酸化亜鉛の配合量を多くすることで熱風・熱老化特性を改善することができ、酸化亜鉛の濃度が低すぎると焦げ付きの問題を引き起こす可能性があります。さらに、タイヤの熱蓄積と摩耗を低減するため、ゴムタイヤ業界では重要なセグメントとなっています。このように、タイヤ産業の成長に伴い、酸化亜鉛の消費量も同時に増加しています。

- 中国、インド、日本、韓国、タイなどのアジア太平洋諸国は自動車の主要生産国です。従って、この市場は予測期間中に成長を記録すると予想されます。

アジア太平洋地域が市場を独占する

- ゴム加工、化学加工、農業など様々な用途で亜鉛化学誘導体が広く使用されているため、アジア太平洋地域が市場を独占することになるでしょう。

- 中国は化学加工の中心地であり、世界中で生産される化学品の大半を占めています。奨励的な政府の取り組みと広大な消費者基盤のおかげで、中国の化学品製造セクターは予測期間中一貫した速度で増加すると予想されます。化学製品の生産量の増加は、近い将来、同国市場の成長機会を生み出すと予想されます。

- インドでは、40社のタイヤメーカーと約6,000社の非タイヤメーカーが、自動車、鉄道、防衛、航空宇宙、その他の用途向けに、シール、コンベヤベルト、押出成型ゴムプロファイルを生産しています。

- さらに、インドには2,500社を超える装飾用メーカーと800社を超える工業用コーティングメーカーがあります。このようなコーティング需要の増加により、各社は生産と生産能力の増強を図っています。このため、同国では液状合成ゴム市場の需要が伸びると予想され、今後数年間は亜鉛化合物の需要をさらに押し上げる可能性があります。

- 中国とインドでは、農薬産業と経済の成長により、亜鉛化合物の需要が増加すると予想されます。化学肥料が安価で入手しやすいことが、市場成長の主な要因となっています。硫酸亜鉛は化学肥料の肥料添加物として使用され、亜鉛化合物市場を刺激しています。

- IRSG(国際ゴム研究グループ)の調査によると、アジアとオセアニアが世界のゴム消費量の70%以上を占めており、中国が40%、日本が6%を占めています。

- 日本はタイヤ生産の主要拠点であり、世界最大級のゴム産業を有しています。

- さらに、ゴムの総消費量では中国、米国に次いで世界第3位です。東ソー株式会社、日本ゼオン株式会社、東洋ゴム工業株式会社など、日本最大のタイヤメーカーが生産能力増強を進めており、予測期間中、ゴム加工産業からの亜鉛ケミカルにとってエキサイティングな市場環境がもたらされると予想されます。

- したがって、このような市場動向はすべて、予測期間中にこの地域の亜鉛化合物市場の需要を促進すると予想されます。

亜鉛化合物産業の概要

亜鉛化合物市場は断片化されており、大きなシェアを獲得している企業はないです。同市場の主要企業(順不同)には、米国Zinc、Zochem Inc.、EverZinc、TIB Chemicals AG、Weifang Longda Zinc Industryなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 自動車産業における利用の高まり

- ゴムタイヤ産業からの需要増加

- 抑制要因

- 亜鉛化学物質による健康被害

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- 酸化亜鉛

- 硫酸亜鉛

- 炭酸亜鉛

- 塩化亜鉛

- その他のタイプ

- エンドユーザー産業

- 農業

- 化学・石油化学

- セラミック

- 製薬

- 塗料・コーティング

- ゴム加工

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- トルコ

- ロシア

- 北欧諸国

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- American Chemet Corporation

- Changsha Lantian Chemical Co. Ltd

- EverZinc

- Flaurea Chemicals

- Global Chemical Co. Ltd

- Hakusui Tech

- Intermediate Chemicals Company

- L. Brugge-mann GmbH & Co. KG

- Nexa

- Old Bridge Chemicals Inc.

- Pan-Continental Chemical Co. Ltd

- Rech Chemical Co. Ltd

- Rubamin

- Seyang Zinc Technology(Huai An)Co. Ltd

- Silox India Pvt. Ltd

- TIB Chemicals AG

- US Zinc

- Weifang Longda Zinc Industry Co. Ltd

- Zochem LLC

第7章 市場機会と今後の動向

- 医療産業における亜鉛ナノ粒子の応用研究開発

- エレクトロニクス・半導体産業における用途の拡大

目次

The Zinc Chemicals Market size is estimated at 4.55 million tons in 2025, and is expected to reach 5.67 million tons by 2030, at a CAGR of 4.47% during the forecast period (2025-2030).

The outbreak of COVID-19 brought several short-term and long-term consequences in the construction, petrochemical, and other industries, which affected the zinc chemicals market across the world. However, presently, the market has returned to the pre-pandemic level.

Key Highlights

- Over the short term, the rising utilization in the automotive industry and increasing demand from the rubber tire industry are likely to drive the growth of the zinc chemicals market.

- On the flip side, factors such as health hazards related to zinc-based chemicals are expected to hinder the growth of the market.

- The emerging research and technological advancements in the field of zinc nanoparticles employed for diagnosis, imaging, and treatment of cancer are expected to offer great opportunities for the zinc market over the upcoming years.

- Asia-Pacific has dominated the market and is expected to continue dominating it during the forecast period.

Zinc Chemicals Market Trends

The Rubber Processing Segment to Dominate the Market

- The rubber processing segment is the dominating segment due to the large-scale consumption of zinc chemicals in galvanizing and manufacturing tires.

- Zinc chemicals are widely used in manufacturing tires and tubes commonly used in automobiles. The growing automobile industry is expected to augment the overall demand for zinc chemicals shortly.

- According to the International Rubber Study Group (IRSG), the global output of natural rubber reached nearly 6.5 million metric tons during the first six months of 2023, a significant rise compared to 2000, when it stood at approximately 6.8 million metric tons.

- As per the Association of Natural Rubber Producing Countries (ANRPC), in March 2023, worldwide demand for natural rubber increased by 7.9% to 1.306 million tons over the same timeframe.

- The growing popularity of electric vehicles is expected to drive the demand for automotive tires, thereby propelling the consumption of tires in the automotive industry, which, in turn, drives the zinc chemical market.

- Also, higher loadings of zinc oxide can improve hot air/heat aging properties, and too low a concentration of zinc oxide can lead to scorching problems. Furthermore, it reduces heat buildup and wear in tires, thus making it an important segment in the rubber tire industry. Thus, with the growth in the tire industry, the consumption of zinc oxide is also increasing concurrently.

- Asia-Pacific countries like China, India, Japan, South Korea, and Thailand are the primary producers of automobiles. Hence, the market studied is expected to register growth during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific stands to be the dominant region in the market studied owing to the extensive application of zinc chemical derivatives in various applications, including rubber processing, chemical processing, and agriculture.

- China is a hub for chemical processing, accounting for most chemicals produced worldwide. Owing to the encouraging government initiatives and a vast consumer base, the chemical manufacturing sector in China is expected to increase at a consistent rate during the forecast period. The increasing production of chemicals is expected to create an opportunity for the growth of the market in the country in the near future.

- In India, 40 tire manufacturers and around 6,000 non-tire manufacturers produce seals, conveyor belts, and extruded and molded rubber profiles for automotive, railway, defense, aerospace, and other applications.

- Furthermore, India is home to over 2,500 decorative and 800 industrial coating manufacturers. This increasing demand for coatings has prompted the companies to increase their production and production capacities. This is expected to drive the demand for the liquid synthetic rubber market in the country, which may further boost the demand for zinc chemicals in the coming years.

- In China and India, the demand for zinc chemicals is expected to increase due to the growing agrochemical industry and economy. The low cost and easy availability of chemical fertilizers act as key factors in the growth of the market. Zinc sulfate is used as a fertilizer additive in chemical fertilizers, stimulating the zinc chemicals market.

- According to the IRSG (International Rubber Study Group) research, Asia and Oceania account for more than 70% of the world's rubber consumption, with China and Japan accounting for 40% and 6%, respectively.

- Japan possesses one of the world's largest rubber industries, as it is a major hub for tire production.

- Furthermore, the country is ranked third globally, only behind China and the United States, in terms of the total amount of rubber consumed. The largest producers of tires in Japan, like Tosoh Corporation, Zeon Corp., and Toyo Tire & Rubber Co. Ltd, are undergoing capacity additions, which is expected to present an exciting market arena for zinc chemicals from the rubber processing industry over the forecast period.

- Hence, all such market trends are expected to drive the demand for the zinc chemicals market in the region during the forecast period.

Zinc Chemicals Industry Overview

The zinc chemicals market is fragmented, with no player capturing a significant share. Some of the key companies in the market (not in any particular order) include US Zinc, Zochem Inc., EverZinc, TIB Chemicals AG, and Weifang Longda Zinc Industry Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Utilization in Automotive Industry

- 4.1.2 Increasing Demand from the Rubber Tires Industry

- 4.2 Restraints

- 4.2.1 Health Hazard Related to Zinc Chemical

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Volume)

- 5.1 Type

- 5.1.1 Zinc Oxide

- 5.1.2 Zinc Sulfate

- 5.1.3 Zinc Carbonate

- 5.1.4 Zinc Chloride

- 5.1.5 Other Types

- 5.2 End-user Industry

- 5.2.1 Agriculture

- 5.2.2 Chemicals and Petrochemicals

- 5.2.3 Ceramic

- 5.2.4 Pharmaceutical

- 5.2.5 Paints and Coatings

- 5.2.6 Rubber Processing

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 American Chemet Corporation

- 6.4.2 Changsha Lantian Chemical Co. Ltd

- 6.4.3 EverZinc

- 6.4.4 Flaurea Chemicals

- 6.4.5 Global Chemical Co. Ltd

- 6.4.6 Hakusui Tech

- 6.4.7 Intermediate Chemicals Company

- 6.4.8 L. Brugge-mann GmbH & Co. KG

- 6.4.9 Nexa

- 6.4.10 Old Bridge Chemicals Inc.

- 6.4.11 Pan-Continental Chemical Co. Ltd

- 6.4.12 Rech Chemical Co. Ltd

- 6.4.13 Rubamin

- 6.4.14 Seyang Zinc Technology (Huai An) Co. Ltd

- 6.4.15 Silox India Pvt. Ltd

- 6.4.16 TIB Chemicals AG

- 6.4.17 US Zinc

- 6.4.18 Weifang Longda Zinc Industry Co. Ltd

- 6.4.19 Zochem LLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 R&D in Application of Zinc Nanoparticle in Medical Industry

- 7.2 Growing Use in Electronics and Semiconductor Industry

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日