|

|

市場調査レポート

商品コード

1689896

アルミニウム- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Aluminum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アルミニウム- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

アルミニウム市場は予測期間中に3.5%以上のCAGRで推移する見込みです。

主なハイライト

- COVID-19は2020年の市場にマイナスの影響を与えました。アルミニウムの主要なシンクである建築・建設は大きな打撃を受け、特に住宅用不動産が抑制された結果、住宅登録が停止され、住宅ローンの実行が遅れました。しかし、規制が解除されて以来、このセクターは順調に回復しています。アルミニウム市場は、建築・建設、包装などの様々なエンドユーザー産業からの消費増加により、2021-22年に大幅に回復しました。

- 市場調査の主な促進要因は、アジア太平洋における建設活動の増加です。食品、包装、製薬業界からのアルミニウム需要の増加は、市場の成長に有利に働く可能性が高いです。

- しかし、アルミニウム加工に関する厳しい規制や環境への懸念は、市場の成長を妨げる可能性が高いです。

- 電気自動車市場の成長が新たな成長機会をもたらす可能性が高いです。

- アジア太平洋が最も高い市場シェアを占めており、予測期間中、市場を独占すると予想されます。

アルミニウム市場の動向

建築・建設業界からの需要増加

- 建築・建設業界では、アルミニウムは2番目に広く使用されている金属です。窓、カーテンウォール、屋根、クラッディング、ソーラーシェーディング、ソーラーパネル、手すり、棚、その他の仮設構造物に幅広く使用されています。

- 世界の建設業界の収益は、今後数年間安定的に成長すると予想されています。2022年末には、約8兆2,000億米ドルになると予測されています。

- 中国は世界最大の建設市場であり、世界全体の建設投資の20%を占めています。中国は、2030年までに約13兆米ドルを建築物に投じると予想されています。中国国家統計局によると、2022年第4四半期の中国における建設業の総生産額は約2,760億人民元(~400億米ドル)で、前期(~276億米ドル)と比べて約50%の伸びを示しました。

- 米国国勢調査局と米国住宅都市開発省が発表した数字によると、2021年12月に建築許可された民間の住宅戸数は、季節調整済み年率で187万3,000戸でした。一戸建て許可件数は毎年合計112.8万件でした。5戸以上の構造における戸数認可の年間率は675,000でした。2021年には、1,724,700戸の住宅が建築許可によって許可される予定でした。この数字は、2020年に予測された1,471,100戸よりも17.2%多いです。

- インドでは、今後7年間で約1兆3,000億米ドルが住宅に投資され、その間に6,000万戸の住宅が新たに建設される見込みです。2024年には、手ごろな価格の住宅の供給率が約70%上昇すると予想されています。インド政府の「2022年までにすべての人に住宅を」も、業界にとって大きな変革です。

- 英国の2021年の新築工事額(現行価格)は、2020年に15.9%減の1,001億9,900万ポンド(~1,286億2,212万米ドル)であった後、15.3%増の1,155億7,900万ポンド(~1,590億877万米ドル)と大幅な伸びを示しました。

- 全体として、世界の建設活動の回復が、予測期間中の建築・建設業界のアルミニウム需要を牽引すると予想されます。

アジア太平洋が市場を独占する見込み

- 予測期間中、アジア太平洋がアルミニウムの最大市場になると予想されます。中国、インド、日本などの国々では、エレクトロニクス、建築・建設、航空宇宙などの産業が成長しています。

- 中国の自動車製造業は世界最大です。中国汽車工業協会によると、2022年の自動車生産台数は2,702万台に達し、2021年の2,608万台に比べて約3.4%増加しました。

- インドでは、今後7年間で住宅に約1兆3,000億米ドルが投資され、その間に6,000万戸の住宅が新たに建設される見込みです。インド連邦内閣は、国内の主要都市で約1,600の行き詰まった住宅プロジェクトを復活させるため、35億8,000万米ドルの代替投資ファンド(AIF)を設立することを承認しました。

- インドのエレクトロニクス市場は、2025年までに4,000億米ドルに達すると予想されています。さらに、インドは2025年までに世界第5位の家電・エレクトロニクス産業になると予想されています。

- インド包装産業協会(PIAI)によると、インドの包装産業は予測期間中に22%の成長が見込まれています。さらに、インドの包装市場は、2020年から2025年にかけてCAGR26.7%を記録し、2025年には2,048億1,000万米ドルに達すると予想されています。

- 日本では、2025年までに包装食品市場の小売売上高は2,045億米ドルに達すると推定され、3.6%、70億米ドルの成長が見込まれます。このような包装業界の成長予測は、予測期間中、箔として使用されるアルミニウムの需要を促進すると思われます。

- したがって、アジア太平洋の国々でエンドユーザー産業が急成長していることから、この地域が予測期間中に世界市場を独占すると予想されます。

アルミニウム産業の概要

アルミニウム市場は、その性質上、部分的に断片化されています。主要企業には、中国アルミニウム集団有限公司(CHINALCO)、中国虹橋集団有限公司(China Hongqiao Group Limited)、ルサール(RusAL)、シンファグループ(Xinfa Group)、リオ・ティント(Rio Tinto)などが含まれる(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- アジア太平洋における建設活動の増加

- その他の促進要因

- 抑制要因

- アルミニウム加工に関する厳しい規制と環境問題

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

- 輸出入動向

- 価格分析

第5章 市場セグメンテーション

- 加工タイプ

- 鋳物

- 押出

- 鍛造品

- 圧延品

- 顔料および粉末

- エンドユーザー産業

- 自動車

- 航空宇宙・防衛

- 建築・建設

- 電気・電子

- 包装

- 工業

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)分析

- 主要企業の戦略

- 企業プロファイル

- Alcoa Corporation

- Aluminum Bahrain B.S.C.(Alba)

- Aluminum Corporation of China Limited(CHINALCO)

- China Hongqiao Group Limited

- East Hope Group

- Emirates Global Aluminum PJSC

- Novelis Inc.

- Norsk Hydro ASA

- Rio Tinto

- RusAL

- State Power Investment Corporation(SPIC)

- Xinfa Group Co. Ltd

第7章 市場機会と今後の動向

- 電気自動車市場の成長

- その他の機会

目次

Product Code: 69206

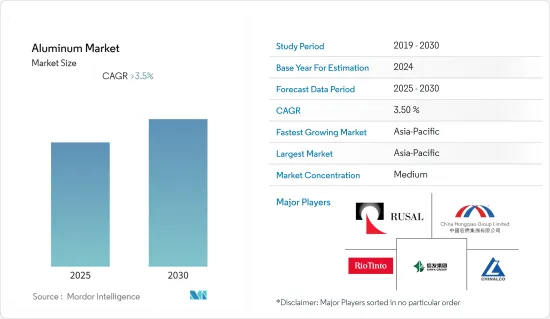

The Aluminum Market is expected to register a CAGR of greater than 3.5% during the forecast period.

Key Highlights

- COVID-19 negatively impacted the market in 2020. Building and construction, a major sink for aluminum, was badly hit, especially due to curtailment in residential real estate resulting in the suspension of home registrations and slow home loan disbursements. However, the sector is recovering well since restrictions were lifted. The aluminum market recovered significantly in 2021-22, owing to rising consumption from various end-user industries such as building and construction, packaging, and others.

- A major factor driving the market studied is the increasing construction activities in the Asia-Pacific region. The rising demand for aluminum from the food, packaging, and pharmaceutical industries will likely favor the market's growth.

- However, strict regulations and environmental concerns about aluminum processing will likely hamper the market's growth.

- Growth in the electric vehicles market will likely provide new growth opportunities.

- The Asia-Pacific accounts for the highest market share and is expected to dominate the market during the forecast period.

Aluminum Market Trends

Increasing Demand from the Building and Construction Industry

- In the building and construction industry, aluminum is the second most widely used metal. It is extensively used in windows, curtain walls, roofing and cladding, solar shading, solar panels, railings, shelves, and other temporary structures.

- The revenue of the global construction industry is expected to grow steadily over the next few years. At the end of 2022, it is projected to be around USD 8.2 trillion.

- China includes the largest construction market in the world, encompassing 20% of all construction investments globally. China is expected to spend nearly USD 13 trillion on buildings by 2030. According to the National Bureau of Statistics of China, the total output value of construction businesses in China in the fourth quarter of 2022 was approximately CNY 276 billion (~USD 40 billion), a growth of approximately 50% when compared with the previous quarter (~USD 27.6 billion).

- The privately-owned residential units permitted by building permits were at a seasonally adjusted annual rate of 1,873,000 in December 2021, according to figures published by the US Census Bureau and the US Department of Housing and Urban Development. A total of 1,128,000 single-family permits were issued each year. The yearly rate of unit authorizations in structures with five or more units was 675,000. In 2021, 1,724,700 housing units were scheduled to be granted through building permits. This figure was 17.2% more than the 1,471,100 predicted for 2020.

- India will likely witness an investment of around USD 1.3 trillion in housing over the next seven years, during which it will likely witness the construction of 60 million new homes. The availability rate of affordable housing is expected to rise by around 70% in 2024. The Indian government's 'Housing for All by 2022' is also a major game-changer for the industry.

- The value of construction new work in current prices in Great Britain in 2021 experienced strong growth (15.3%) to GBP 115,579 million (~USD 1,59,008.77 million) after a 15.9% fall to GBP 100,199 million (~ USD 1,28,622.12 million) in 2020.

- Overall, the recovering construction activities worldwide are expected to drive the demand for aluminum from the building and construction industry during the forecast period.

Asia-Pacific Region Expected to Dominate the Market

- The Asia-Pacific region is expected to be the largest market for aluminum during the forecast period. Industries such as electronics, building and construction, aerospace, etc., are growing in countries such as China, India, and Japan.

- The Chinese automotive manufacturing industry is the largest in the world. According to the China Association of Automobile Manufacturers, in 2022, automotive production in the country reached 27.02 million units, which increased by about 3.4%, compared to 26.08 million vehicles produced in 2021.

- India will likely witness an investment of around USD 1.3 trillion in housing over the next seven years, during which it will likely witness the construction of 60 million new homes. The Union Cabinet of India approved the setting up a USD 3.58 billion alternative investment fund (AIF) to revive around 1,600 stalled housing projects across the top cities in the country.

- The Indian electronics market is expected to reach USD 400 billion by 2025. Additionally, India is expected to become the world's fifth-largest consumer electronics and appliances industry by 2025.

- According to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at 22% during the forecast period. Moreover, the Indian packaging market is expected to reach USD 204.81 billion by 2025, registering a CAGR of 26.7% between 2020 and 2025.

- In Japan, it is estimated that by 2025, the retail sales in the packaged food market are expected to reach USD 204.5 billion, a growth of 3.6% or USD 7 billion. Such projected growth in the packaging industry will likely drive the demand for aluminum used as foils during the forecast period.

- Hence, with the rapidly growing end-user industries in countries of the Asia-Pacific region, the region is expected to dominate the global market during the forecast period.

Aluminum Industry Overview

The aluminum market is partially fragmented in nature. The major companies include (not in any particular order) Aluminum Corporation of China Limited (CHINALCO), China Hongqiao Group Limited, RusAL, Xinfa Group Co. Ltd., and Rio Tinto, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Construction Activities in the Asia-Pacific Region

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Strict Regulations and Environmental Concerns Related to Aluminum Processing

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Import-Export Trends

- 4.6 Price Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Processing Type

- 5.1.1 Castings

- 5.1.2 Extrusions

- 5.1.3 Forgings

- 5.1.4 Flat Rolled Products

- 5.1.5 Pigments and Powders

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Packaging

- 5.2.6 Industrial

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alcoa Corporation

- 6.4.2 Aluminum Bahrain B.S.C. (Alba)

- 6.4.3 Aluminum Corporation of China Limited (CHINALCO)

- 6.4.4 China Hongqiao Group Limited

- 6.4.5 East Hope Group

- 6.4.6 Emirates Global Aluminum PJSC

- 6.4.7 Novelis Inc.

- 6.4.8 Norsk Hydro ASA

- 6.4.9 Rio Tinto

- 6.4.10 RusAL

- 6.4.11 State Power Investment Corporation (SPIC)

- 6.4.12 Xinfa Group Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growth in Electric Vehicles Market

- 7.2 Other Opportunities