|

市場調査レポート

商品コード

1910715

ポリエーテルアミン:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Polyetheramine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポリエーテルアミン:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

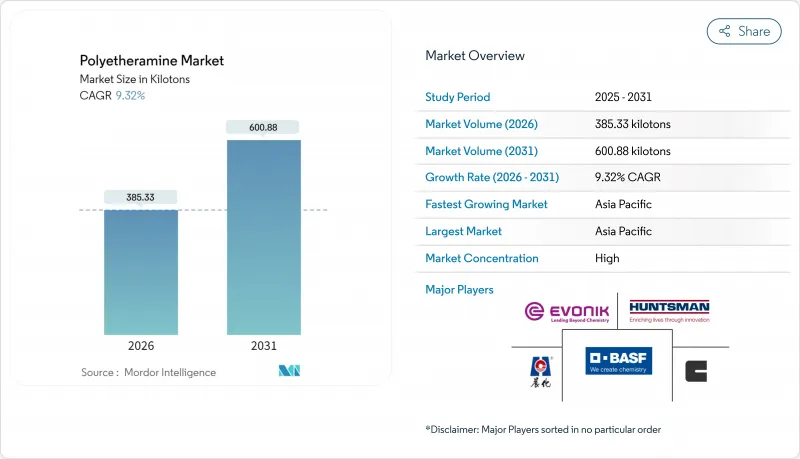

ポリエーテルアミン市場の規模は、2026年には385.33キロトンと推定されております。

これは2025年の352.47キロトンから成長した数値であり、2031年には600.88キロトンに達すると予測されております。2026年から2031年にかけては、CAGR9.32%で成長する見込みです。

この成長の勢いは、風力タービンブレード生産、複合材料製造、高性能コーティングにおける需要の増加に起因しており、下流産業がより軽量で耐久性の高い材料を追求しているためです。ジアミングレードが主流を占めておりますのは、そのバランスの取れた反応性が大規模なブレード硬化や構造用複合材料に適しているからです。洋上風力発電の拡大、自動車の軽量化、インフラ耐障害性プロジェクトが特殊アミン需要を牽引し続ける一方、3Dプリント調合業者は複雑な形状に対応するためポリエーテルアミン硬化エポキシを採用しています。原料価格の変動とアミン排出規制の強化が短期的な利益率を抑制するもの、バイオベース製品、アジア太平洋地域における生産能力増強、垂直統合戦略により、主要サプライヤーは持続的な収益成長の基盤を築いています。

世界の・ポリエーテルアミン市場の動向と展望

接着剤・シーラント産業への投資増加

建設業者や自動車メーカーが軽量で耐食性に優れた接着ソリューションを求める中、先進的な建設用・電動モビリティ用接着剤への資本配分が増加しています。ポリエーテルアミン改質システムは、低VOC特性と極限温度下での高い剥離強度を実現するため、プレミアム価格が設定されています。BASFのBaxxodur製品群(北米ではユニバーソリューションズ経由で販売)は、統合物流が市場浸透を強化する好例です。また、持続可能性への要求も、エボニック社のバイオ含有ポリエーテルアミン「Ancamide 2853/2865」などの製品発売を後押ししており、ISO 14001認証工場におけるポリエーテルアミンの採用を促進しています。

複合材製造分野における需要拡大

航空宇宙認証や自動車燃費規制の強化により、樹脂メーカーはポットライフを延長しつつ疲労抵抗性を高める硬化剤への転換を迫られています。世界の風力発電容量が既に743GWを超える中、100メートルを超えるブレードには、低温環境下での大型部品加工時に構造的完全性を維持するポリエーテルアミン硬化型エポキシ樹脂が不可欠です。光ファイバー内蔵センシングシステムの普及は、光学的に透明で収縮率の低い硬化剤の需要をさらに高めています。恒力(Hengli)や盛宏(Shenghong)といった中国の石油化学大手は、原料確保とリードタイム短縮のため下流工程への統合を進めており、これにより競合は激化する一方、供給の耐障害性も拡大しています。

アミン排出に関する環境懸念

米国環境保護庁(EPA)のNESHAP規制範囲拡大により、プラントはスクラバーの改修または閉鎖系システムの導入を迫られており、中規模生産者の設備投資額が増加しています。排出規制はアミン系炭素回収溶剤に対する社会的評価にも影響を与え、間接的にポリエーテルアミンの評判にも波及しています。サプライヤーは低臭気・バイオ含有グレードの販促や、機器OEMとの連携による低排出加工プロトコルの共同開発で対応しています。

セグメント分析

ジアミングレードは2025年出荷量の49.05%を占め、反応性と柔軟性のバランスが求められる風力ブレードや構造用複合材用途を支えており、2031年までCAGR9.88%で推移する見込みです。ハンツマン社のジェファミンDシリーズは分子量230~2,000の範囲をカバーし、20年の耐用年数を設計目標とするブレード向けに架橋密度を調整可能です。

モノアミンおよびトリアミンの生産量は少ないもの、ニッチなニーズに対応しています。モノアミンはコーティングにおける表面濡れ性を向上させ、トリアミンは高Tg航空宇宙パネル向けの架橋密度を高めます。中国メーカーのZibo Dexin Lianbang Chemicalは年間3万トン規模に拡大し、コスト重視のバイヤー向けの原料選択肢を広げています。エボニック社のアンカミン2880に代表されるバイオベースジアミンの研究開発は、屋外用キットの紫外線安定性を維持しつつ、持続可能な原料への移行を実証しています。

ポリエーテルアミン報告書は、タイプ別(モノアミン、ジアミン、トリアミン)、用途別(ポリウレア、燃料添加剤、複合材料、エポキシ塗料、接着剤・シーラント、その他)、エンドユーザー産業別(自動車、建築・建設、風力エネルギー、電子・電気、その他エンドユーザー産業)、地域別(アジア太平洋、北米、欧州、南米、中東・アフリカ)に分類されています。

地域別分析

2025年、アジア太平洋地域はポリエーテルアミン市場シェアの53.42%を占めました。中国、インド、東南アジアにおけるブレードおよび複合部品の生産量増加が背景にあります。生産能力の増強としては、BASFの南京特殊アミン工場および漕滄工場の年間1万8,800トンへの拡張が挙げられ、これにより地域供給が強化され、納期短縮が図られています。

北米は航空宇宙主要メーカーと先進的な3Dプリントサービス事業者を中核とするイノベーション拠点であり続けております。EPA NESHAP規制への適合は、確固たる環境認証を有するサプライヤーに利益をもたらし、ユーザーに低VOCジアミン化学品の採用を促しております。BASFのBaxxodur製品がユニバーソリューションズを通じて独占販売されることで技術サービス網が強化され、自動車・建設分野の一次OEMメーカーにおける迅速な仕様策定サイクルを支援しております。

欧州のエネルギー転換政策は、再生可能ブレードや循環型経済対応コーティングの需要を持続させております。TPIコンポジッツのトルコ拠点は欧州風力発電所向け生産能力を拡充し、REACH規制は複雑な文書管理をこなせる既存サプライヤーを優遇しております。南米や中東の新興地域では再生可能エネルギー設備と工業用コーティング需要が拡大中ですが、主にアジア太平洋地域の拠点からの輸入に依存しており、現地での混合施設導入が検討されております。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 接着剤・シーラント産業への投資増加

- 複合材料製造分野における需要拡大

- 風力タービンブレード生産の拡大

- 高性能ポリウレア保護塗料の需要急増

- 3Dプリント用エポキシ樹脂システムへの採用

- 市場抑制要因

- 原料プロピレンオキシド価格の変動性

- アミン排出に関する環境問題

- 食品接触用接着剤グレードの認可遅延

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- モノアミン

- ジアミン

- トリアミン

- 用途別

- ポリウレア

- 燃料添加剤

- 複合材料

- エポキシ樹脂コーティング

- 接着剤・シーラント

- その他

- エンドユーザー産業別

- 自動車

- 建設・建築

- 風力エネルギー

- 電子・電気

- その他のエンドユーザー産業

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- BASF

- Clariant

- Evonik Industries AG

- Huntsman International LLC

- Qingdao IRO Surfactant Co., Ltd.

- Shandong Longhua New Materials Co., Ltd.

- Wuxi Akeli Technology Co., Ltd.

- Yangzhou Chenhua New Material Co., Ltd.

- Yantai Dasteck Chemicals Co., Ltd.

- Zibo Zhengda Polyurethane Co., Ltd.