|

市場調査レポート

商品コード

1910682

エポキシ硬化剤:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Epoxy Curing Agent - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エポキシ硬化剤:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

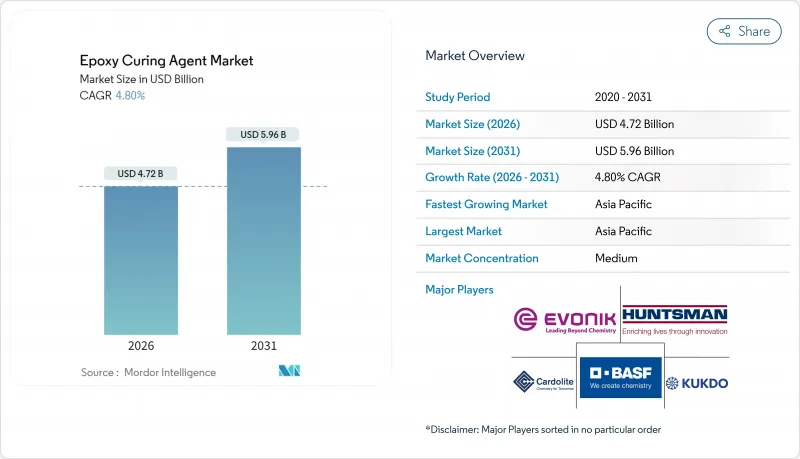

エポキシ硬化剤市場の規模は、2026年には47億2,000万米ドルと推定されており、2025年の45億米ドルから成長が見込まれます。

2031年の予測では59億6,000万米ドルに達し、2026年から2031年にかけてCAGR4.8%で成長すると見込まれています。

この成長は、アジア太平洋地域のインフラ整備、再生可能エネルギー資産の着実な導入、ならびにモビリティおよび航空宇宙分野における軽量複合材料の需要急増に支えられています。アンチダンピング関税が世界貿易の流れを変える中、競合環境は変化しており、欧米の生産者は高利益率の特殊化学品分野へ軸足を移しつつあります。製品革新は、低揮発性有機化合物(VOC)、バイオベース、短時間硬化システムなど、生産サイクルの短縮を可能にする方向へ偏っています。一方、北米および欧州におけるサプライチェーンの安全保障イニシアチブは、調達戦略の再構築を促しています。その結果、エポキシ硬化剤市場は統合が進んでいますが、持続可能性に焦点を当てたニッチな新規参入者が引き続き登場しており、競合情勢は複雑化しています。

世界のエポキシ硬化剤市場の動向と洞察

インフラブームが牽引する高性能床用コーティング材の需要

アジアにおけるインフラ大型プロジェクトは増加を続けており、化学薬品、機械的衝撃、高交通量に耐える産業用床材に対する厳しい性能仕様が生まれています。中国、インド、東南アジアにおける公共部門の支出は、データセンターキャンパス、地下鉄ネットワーク、再生可能エネルギー施設に資金を投入しており、これら全てに耐久性、帯電防止性、速硬化性を備えたコーティングが求められています。その結果、調合メーカーは、より厳しい環境規制に準拠しつつ、請負業者のダウンタイムを削減する低排出エポキシシステムをカスタマイズしています。この変化は、導電性床材が統合された資産追跡およびエネルギー管理技術を可能にするスマートビルディングの概念にも広がっています。バランスの取れたコストパフォーマンスのパッケージを提供できるサプライヤーは、複数年にわたる供給契約を獲得しており、エポキシ硬化剤市場の成長軌道を強化しています。

アジア太平洋地域および欧州における風力タービンブレード生産の急増

2024年、世界の風力発電設備容量は115GWを突破し、ブレードメーカーは受注残に対応するためタクトタイムの短縮を急いでいます。大型ローター設計には、発熱量が低く、ボイドを最小限に抑え、層間靭性を高める硬化剤が求められます。BASFのBaxxodurシリーズは、最適化されたアミンブレンドが機械的強度を損なうことなくサイクルタイムを短縮する好例です。欧州のOEMメーカーは温度低減とリサイクル性目標を設定し、ブレード部品分解を簡素化する可逆性化学技術の研究開発を促進しています。一方、中国のブレード工場は現地原料と物流の優位性を活用し、欧米メーカーに生産ラインの現地化を促すことで、アジアに製造拠点を有するエポキシ硬化剤市場参入企業に対する地域需要を拡大させています。

溶剤系アミン系に対するより厳格なVOC規制

米国国家エアゾール塗料規則の改正および南海岸大気質管理地区(AQMD)の改正案により、許容VOC閾値が大幅に引き下げられ、調合業者は水性・高固形分・無溶剤系化学技術への移行を迫られています。規制対応により環境に優しい代替品の市場機会は拡大する一方、特に性能を損なえない分野では、研究開発費および認証コストが増加しています。急速硬化型のバイオベース代替品は開発中ですが、スケールアップの障壁に直面しており、これが短期的な供給可能性を制約し、エポキシ硬化剤市場全体の成長加速を妨げる可能性があります。

セグメント分析

アミン系は2025年の売上高の41.12%を占め、ほとんどの複合材、塗料、接着剤システムの基幹化学品としての地位を確固たるものにしております。このカテゴリー内では、脂肪族および脂環式アミンが耐紫外線性を提供し、ポリエーテルアミンは船舶用保護塗料など柔軟性が求められる環境で優れた性能を発揮します。無水物は、180℃での使用が日常的な高温電気絶縁材や自動車エンジンルーム部品において、依然として重要な役割を果たしています。フェノールアルカミンはニッチな分野ではありますが、湿潤環境や低温作業現場での急速硬化を実現し、全天候型の生産性を追求する施工業者から評価される価値提案となっています。このセグメントの適応性の高い性能プロファイルは、持続可能性の動向が競合化学物質を招き入れる中でも、エポキシ硬化剤市場の中核であり続けることを保証しています。

アミン系が主流である一方、競合圧力は継続しております。ポリアミド供給業者はバイオ由来二量体酸プロセスを強調し、炭素削減優位性を主張。一方、無水物メーカーは優れた耐熱サイクル性能を訴求しております。特殊メーカーは、硬化遅延・硬化速度・機械的性能のバランスを図るため、ハイブリッド型アミンー無水物パッケージの実験を進めております。予測期間においては、アミン化学分野における重点的な研究開発が、硬化サイクルを延長することなく靭性を向上させる潜在性触媒やナノフィラーの統合を目指しています。こうした着実な改良の継続により、本セグメントはエポキシ硬化剤市場全体を牽引し続ける立場を確立しています。

地域別分析

アジア太平洋地域は2025年に35.12%のシェアを占め、公共インフラ投資、再生可能エネルギーへの取り組み、電子機器製造の地域集中を背景にCAGR5.66%で拡大しています。中国の風力タービンブレード工場やインドの半導体組立クラスターは、膨大な量のアミン系システムを吸収しています。地域メーカーは、エピクロルヒドリンやベンジルアミン原料への地理的近接性を活用し、物流コストとリードタイムを削減しています。持続可能性に関する規制は強化されていますが、コスト競争力が依然として最重要課題であり、エポキシ硬化剤市場における地域統合型サプライチェーンの必要性を裏付けています。

北米はシェアでは後塵を拝しますが、リショアリングの動きと航空宇宙複合材分野での主導的立場から恩恵を受けています。2025年に米国国際貿易委員会が正式決定したアジア産エポキシ輸入品への反ダンピング関税は、国内設備稼働率を押し上げ、特殊グレードへの投資を促進します。米国とメキシコにおける電気自動車(EV)バッテリー工場の拡張は高固形分接着剤の需要を刺激し、大西洋沿岸地域での洋上風力発電設備の増設はブレードグレード硬化剤の新たな消費層を生み出します。

欧州は高騰するエネルギーコストとアジアの激しい競合に直面し、企業は汎用品の生産合理化と高付加価値ニッチ分野への注力を余儀なくされています。ウェストレイク社のオランダ資産減損処理がこの再調整を象徴しています。しかしながら、自動車用複合材や再生可能風力ブレードの研究開発における欧州のリーダーシップが、次世代化学品への選択的需要を支えています。循環型経済への規制重視がバイオベースおよび低VOC硬化システムの採用を加速させ、地域のエポキシ硬化剤市場にイノベーション主導の道を切り開いております。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- インフラ整備の拡大が、高性能床用塗料の需要を牽引しております

- アジア太平洋地域および欧州における風力タービンブレード生産の急増

- 電子機器の小型化に伴う低ボイド封止材の需要

- 自動車・航空宇宙分野における軽量CFRPの採用

- 熱硬化性樹脂の3Dプリント向け超速硬化システムの台頭

- 市場抑制要因

- 溶剤系アミン系システムに対する揮発性有機化合物(VOC)排出量の上限規制強化

- 揮発性エピクロロヒドリン及びベンジルアミン原料価格

- カシュー由来フェナルカミン原料の供給不足

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ別

- アミン類

- ポリアミド

- 無水物

- その他の種類(フェノールアルカミン、アミドアミンなど)

- 用途別

- 塗料およびコーティング

- 接着剤およびシーラント

- 複合材料

- 電気・電子機器

- その他(産業用床材および補修など)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Aditya Birla Group

- Air Products Inc.

- Atul Ltd.

- BASF

- Cardolite Corporation

- DIC Corporation

- Evonik Industries AG

- Huntsman International LLC

- KUKDO CHEMICAL CO., LTD.

- Kumho P&B Chemicals Inc.

- Mitsubishi Chemical Group Corporation

- Olin Corporation

- Shandong Deyuan Epoxy Resin Co. Ltd

- Toray Industries Inc.

- Westlake Corporation