ビニルエステル:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Vinyl Ester - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689769

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

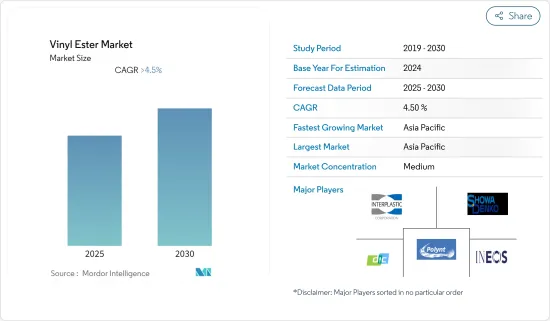

ビニルエステル市場は予測期間中に4.5%を超えるCAGRで推移すると予測されます。

2020年にはCOVID-19の大流行が市場にマイナスの影響を与えたが、大流行前の水準に達したと推定・予測されており、予測期間中(2022~2027年)は安定した成長が見込まれます。

市場を牽引する主な要因は、繊維強化プラスチックのタンクや容器の製造における用途の拡大と、耐腐食性機器の製造における用途の拡大です。

反面、ビニルエステル樹脂の毒性が市場の成長を妨げています。

排煙脱硫における用途の拡大は、予測期間中の市場成長に様々な機会を提供すると期待されています。

アジア太平洋地域はビニルエステル市場を独占しており、中国、インド、日本が市場需要に大きく貢献しています。

ビニルエステル市場の動向

パイプ・タンク分野が市場を独占する見込み

腐食産業では、メンテナンスや修理に多くの時間を奪われるのを避けるため、強度や耐久性を失うことなく耐腐食性があり高温にも耐えられる複合材料が選ばれています。

パイプやタンクにおける繊維強化プラスチック(FRP)の用途は近年増加しています。ビニルエステル樹脂は、耐薬品性に優れ、浸透性が低いため、多くの産業で広く使用されています。

繊維強化プラスチック(FRP)貯蔵タンク、パイプライン、ダックシステムの製造に広く使用されています。パイプ・タンク分野は、ビニルエステル市場で最大のシェアを占めると推定されます。

ビニルエステルベースのFRPパイプやタンクは、クロール・アルカリ・化学工業、発電工業、鉱業・金属工業、工業用水・廃水工業、食品加工工業、パルプ・製紙工業などの産業で広く使用されています。

ビニルエステル系FRP配管は、電力業界で多くの用途に使用されています。例えば、スラリー配管、脱硫装置のスプレーヘッダー、貯蔵タンクなどです。

ビニルエステル系配管は、長期的なメンテナンスコストやポンプ運転コストを削減できることから、産業廃水用途でも人気があります。

以上の点から、パイプ・タンク分野が市場を独占すると予想されます。

中国がアジア太平洋市場を独占する見込み

アジア太平洋地域では、中国がGDPで最大の経済大国です。

中国石油集団(CNPC)によると、中国のガス消費量は2020年に3,200億立方メートル(BCM)にまで増加する見込みで、2040年には約6,000億BCMに急増すると予想されています。増大するガス需要に対応するため、2040年までにガス生産量を2倍の325BCMに増やす計画です。

同国では、今後5年以内に数多くの化学プラントの建設が予定されています。BASFは、中国の広東省南部に位置する100億米ドルの総合石油化学プロジェクトの建設を開始しました。このプラントの第一段階は2022年末までに稼動する予定です。

中国は世界最大の自動車生産国です。2021年1~9月期の生産台数は、2020年同期比で53%増加しました。

以上の点から、中国はアジア太平洋市場を独占すると予想されます。

ビニルエステル業界の概要

ビニルエステル市場は部分的に統合されており、主要企業が大きなシェアを占めています。上位5社が市場全体の60%以上のシェアを占めています。主なプレーヤー(順不同)としては、Polynt、INEOS、DIC CORPORATION、Interplastic Corporation、昭和電工株式会社などが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 繊維強化プラスチック製タンクと容器の製造における用途拡大

- 耐腐食性機器の製造における用途の増加

- 抑制要因

- 樹脂の毒性

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競合の度合い

- 輸出入動向

- 原料分析

- 技術スナップショット

- 価格分析

第5章 市場セグメンテーション

- タイプ

- ビスフェノールAジグリシジルエーテル(DGEBA)

- エポキシフェノールノボラック(EPN)

- その他のタイプ

- 用途

- パイプ・タンク

- 塗料・コーティング

- 輸送

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AOC

- Bkdj Polymers India

- DIC CORPORATION

- INEOS

- Interplastic Corporation

- Poliya

- Polynt

- Scott Bader Company Ltd

- SHOWA DENKO K.K

- Sino Polymer Co. Ltd

- Swancor

第7章 市場機会と今後の動向

- 排煙脱硫におけるアプリケーションの成長

目次

The Vinyl Ester Market is expected to register a CAGR of greater than 4.5% during the forecast period.

The COVID-19 pandemic impacted the market negatively in 2020; however, it has been estimated to have reached pre-pandemic levels and is expected to grow at a steady rate during the forecast period (2022-2027).

The major factors driving the market are growing application in the manufacture of fiber-reinforced plastic tanks and vessels and increasing application in making corrosion-resistant equipment.

On the flip side, the toxicity of vinyl ester resin is hindering the growth of the market studied.

The growing application in flue gas desulphurization is expected to offer various opportunities for the growth of the market studied over the forecast period.

The Asia-Pacific region dominated the market for vinyl ester, with China, India, and Japan being the major contributors to the market demand.

Vinyl Ester Market Trends

The Pipes and Tanks Segment is Expected to Dominate the Market

To avoid losing a large amount of time to maintenance and repairs, the corrosion industry is choosing composite materials that are resistant to corrosion and can withstand high temperatures without losing their strength or durability.

The fiber-reinforced plastic (FRP) application in pipes and tanks has been rising in recent years. Vinyl ester resins are widely used in many industries due to their superior chemical resistance and low permeability.

They are being extensively used to fabricate fiber-reinforced plastic (FRP) storage tanks, pipelines, and duck systems. The pipes and tanks segment is estimated to have the largest share in the vinyl ester market.

Vinyl ester-based FRP pipes and tanks are widely used in industries such as the chlor-alkali and chemical industry, power generation industry, mining and metal industry, industrial water and wastewater industry, food processing industry, and pulp and paper industry.

Vinyl ester-based FRP pipings are used for many applications in the power industry. Some of these include slurry piping, FGD absorber spray headers, and storage tanks.

Vinyl ester-based pipes are also popular in industrial wastewater applications as they reduce long-term maintenance and pump operating costs.

Based on the above-mentioned aspects, the pipes and tanks segment is expected to dominate the market.

China is Expected to Dominate the Asia-Pacific Market

In the Asia-Pacific region, China is the largest economy in terms of GDP.

According to China National Petroleum Corp. (CNPC), the gas consumption in China was expected to rise to 320 billion cubic meters (BCM) in 2020; gas consumption is expected to surge to around 600 BCM by 2040. In order to meet the growing gas demand, the country is planning to double its gas production to 325 BCM by 2040.

There are numerous chemical plants lined up for construction within the period of the next five years in the country. BASF started the construction of its USD 10 billion integrated petrochemicals project, located in the southern province of Guangdong in China. The first phase of this plant is scheduled to come online by the end of 2022.

China is the world's largest automotive producer. The production increased by 53% in the first nine months of 2021 in comparison to the same period of 2020.

Based on the aforementioned aspects, China is expected to dominate the Asia-Pacific market.

Vinyl Ester Industry Overview

The vinyl ester market is partially consolidated, with the top players holding a significant share. The top five players account for a share of more than 60% of the total market. Some of the major players (in no particular order) include Polynt, INEOS, DIC CORPORATION, Interplastic Corporation, and SHOWA DENKO K.K., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Application in the Manufacture of Fiber Reinforced Plastic Tanks and Vessels

- 4.1.2 Increasing Application in Making Corrosion-resistant Equipment

- 4.2 Restraints

- 4.2.1 Toxicity of the Resin

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

- 4.5 Import-export Trends

- 4.6 Feedstock Analysis

- 4.7 Technological Snapshot

- 4.8 Price Analysis

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Bisphenol A Diglycidyl Ether (DGEBA)

- 5.1.2 Epoxy Phenol Novolac (EPN)

- 5.1.3 Other Types

- 5.2 Application

- 5.2.1 Pipes and Tanks

- 5.2.2 Paints and Coatings

- 5.2.3 Transportation

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AOC

- 6.4.2 Bkdj Polymers India

- 6.4.3 DIC CORPORATION

- 6.4.4 INEOS

- 6.4.5 Interplastic Corporation

- 6.4.6 Poliya

- 6.4.7 Polynt

- 6.4.8 Scott Bader Company Ltd

- 6.4.9 SHOWA DENKO K.K

- 6.4.10 Sino Polymer Co. Ltd

- 6.4.11 Swancor

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Application in Flue Gas Desulphurization

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日