|

市場調査レポート

商品コード

1940610

化学的機械研磨:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Chemical Mechanical Planarization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 化学的機械研磨:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

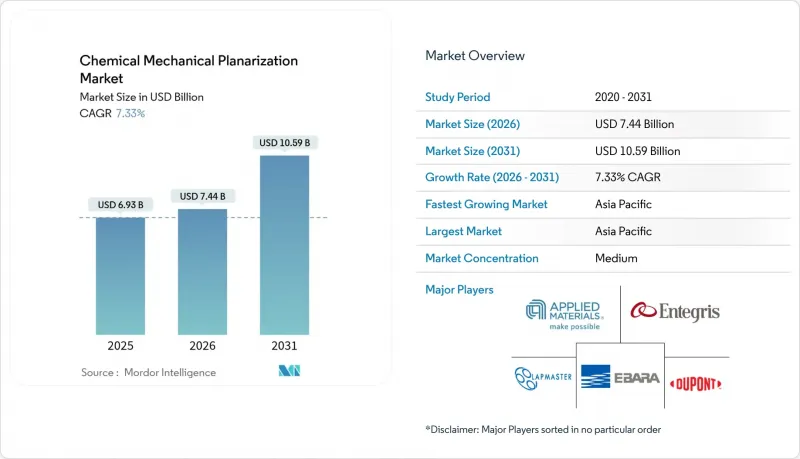

2026年の化学的機械研磨(CMP)市場の規模は74億4,000万米ドルと推定され、2025年の69億3,000万米ドルから成長が見込まれます。

2031年の予測では105億9,000万米ドルに達し、2026年から2031年にかけてCAGR7.33%で成長すると見込まれています。

成長は、FinFETからゲートオールアラウンド(GAA)トランジスタへの移行、3D集積化、およびパワーデバイスにおける炭化ケイ素(SiC)と窒化ガリウム(GaN)の使用増加によって推進されています。ファウンダリは引き続き大規模な生産能力の増強を進めており、米国および欧州連合(EU)における政府のインセンティブが、現地のCMPサプライチェーンを促進しています。装置の供給逼迫が生産拡大を制約する一方、持続可能性への取り組みが低研磨剤・無研磨剤スラリーの需要を加速させています。地政学的な輸出規制が装置の流れを再構築し、欧米と中国のベンダー間で並行した技術革新の流れを促進しています。

世界の化学的機械研磨(CMP)市場の動向と洞察

GAAおよび3D-ICの採用加速

ゲート・オール・アラウンド(GAA)トランジスタは、高度な選択的除去率と厳格な欠陥閾値を必要とする新たな金属ゲートスタックを導入することで、CMP化学薬品の性質を変えています。主要ファウンダリは3nm以下のGAAノード量産を計画しており、高度なエンドポイント制御を備えた300mm単結晶ポリッシャーの設備更新サイクルを推進しています。シリコン貫通ビアなどの補完的な3D集積技術では、複数のウエハー表面にわたる超平坦な銅層が求められます。そのためCMPプラットフォームは、閉ループ式パッド調整とリアルタイムスラリー監視を統合し、より厳しい許容差でも歩留まりを維持します。

SiC/GaNパワーデバイスの急速な成長

炭化ケイ素および窒化ガリウムウエハーは、硬度と化学的不活性性を備えているため、研磨時間と消耗品コストが大幅に増加します。アルカリ化学薬品と設計された研磨剤を使用した専用スラリーにより、表面粗さを0.05nm以下に保ちながら、1µm/hに近い除去率を達成しています。自動車の電動化によりこれらの材料への需要が加速し、工具メーカーはSiCラインと従来のシリコンライン間の研磨摩耗や相互汚染防止に耐性のあるパッド設計を発表しています。

研磨剤投入コストの急騰

酸化セリウム、過酸化水素などの高純度原料は、希土類供給が逼迫したり化学プラントがメンテナンスに入ったりすると価格が急騰します。米国地質調査所によれば、中国は依然として希土類輸入の主要供給源であり、世界のスラリーベンダーは貿易摩擦の影響を受けやすい状況にあります。ベンダーは、研磨剤負荷を低減したスラリーの再配合や、ろ過ループによる使用済み溶液のリサイクルで対応しています。

セグメント分析

2025年における化学的機械研磨(CMP)市場規模の62.78%を装置が占めました。支出は、ウエハー内不均一性を1nm未満に抑え、パッド表面状態管理のための閉ループ調整機能を統合したシングルウエハー装置に集中しています。このセグメントは、GAAプロセスやワイドバンドギャップ基板をサポートする新プラットフォームのファブ導入に伴い、2031年までCAGR7.54%で拡大すると予測されています。同時に、7nm以下のプロセスノードにおけるナノスケール欠陥除去のため、洗浄モジュールのアップグレードも進められています。

消耗品は収益の37.22%を占め、定期的な需要が安定した需要を保証するスラリーが主導しています。シリカ系誘電体スラリーが主流である一方、ニッチなセリア配合はガラスやサファイアの研磨に対応します。パッド供給業者は溝付きポリマーブレンドをリリースし、長寿命化に伴う除去率の安定維持と欠陥発生の最小化を実現しています。持続可能性目標の進展により低研磨性化学薬品への移行が加速し、性能と環境指標が両立する際に消耗品ベンダーはプレミアム価格設定が可能となります。

地域別分析

アジア太平洋地域は2025年の収益の64.12%を占め、2031年までCAGR8.41%で推移すると予測されています。中国本土の現地化推進により積極的なウエハー工場建設が進む一方、台湾は最先端ロジックおよび高度なパッケージング分野での主導権を維持しています。韓国は高層数3D NANDおよびDRAMへの投資を拡大し、誘電体および金属平坦化能力の需要を押し上げています。日本のサプライヤーは、超高純度化学薬品や精密パッドにおける数十年にわたる専門知識を活用し、同地域の垂直統合型エコシステムを強化しています。

北米は売上高で第2位です。連邦政府の優遇措置により新たなファブ建設が実現し、顧客が安全なサプライチェーンを優先する中、国内の装置メーカーが重要な受注を獲得しています。アリゾナ州とニューヨーク州における先進パッケージングの取り組みは、現地調達ルールに準拠したCMP消耗品に対する地域需要を刺激しています。輸出規制により中国向けハイエンドパッドの出荷が制限されることで市場が二分され、北米のCMPベンダーにとって戦略的価値が高まっています。

欧州は2030年までに世界の半導体生産量の20%を目標に掲げ、製造の持続可能性を重視しています。地域の材料メーカーは電子グレード過酸化水素と特殊スラリーの生産能力を拡大し、ドイツやオランダの装置メーカーはCMP製品をEU環境指令に適合させています。政府資金によるヘテロ統合のパイロットライン支援が、研究拠点や特殊ファウンダリにおけるCMP装置の段階的な導入を促進しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- GAAおよび3D-ICの採用加速

- SiC/GaNパワーデバイスの急速な成長

- 微細化に伴うノード固有のCMP工程数の減少

- AIデータセンター設備投資の波及効果(先進的相互接続層)

- 米国およびEUのファブ奨励策によるCMP供給の現地化

- 低研磨性スラリーへの持続可能性推進

- 市場抑制要因

- スラリー投入コストの急騰(希土類元素)

- 300mmツールのOEM生産能力逼迫

- 異種材料CMPにおける交差汚染リスク

- ハイエンドパッドおよびコンディショナーに対する米国と中国の輸出規制

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場規模と成長予測

- 製品タイプ別

- CMP装置

- シングルウエハーCMPシステム

- CMP後処理洗浄装置

- バッチCMPシステム

- その他

- CMP消耗品

- CMPスラリー

- シリカ系スラリー

- 酸化アルミニウムベースのスラリー

- 酸化セリウム系スラリー

- 複合材/エンジニアード研磨スラリー

- その他(ジルコニア、ダイヤモンドなど)

- パッド

- その他の消耗品(フィルター、CMP後処理用洗浄薬品など)

- CMPスラリー

- CMP装置

- 用途別

- 集積回路

- 化合物半導体

- MEMSおよびNEMS

- 先進パッケージング

- その他の用途

- エンドユーザー別

- ファウンダリ

- 統合デバイスメーカー(IDM)

- 半導体受託組立・試験(OSAT)

- 研究開発機関/大学

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度分析

- 戦略的動向と発展

- ベンダーポジショニング分析

- 企業プロファイル

- Applied Materials Inc.

- Entegris Inc.

- EBARA Corporation

- Lapmaster Wolters GmbH

- DuPont de Nemours, Inc.

- Fujimi Incorporated

- Revasum Inc.

- Resonac Holdings Corporation

- Okamoto Corporation

- FUJIFILM Corporation

- Tokyo Seimitsu Co., Ltd.

- Lam Research Corporation

- KLA Corporation

- Hitachi High-Tech Corporation

- Cabot Microelectronics Corporation

- 3M Company

- Saint-Gobain Surface Conditioning

- BASF SE

- Nagase ChemteX Corporation

- Ace Nanochem Co., Ltd.