|

市場調査レポート

商品コード

1910667

包装印刷:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Packaging Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 包装印刷:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

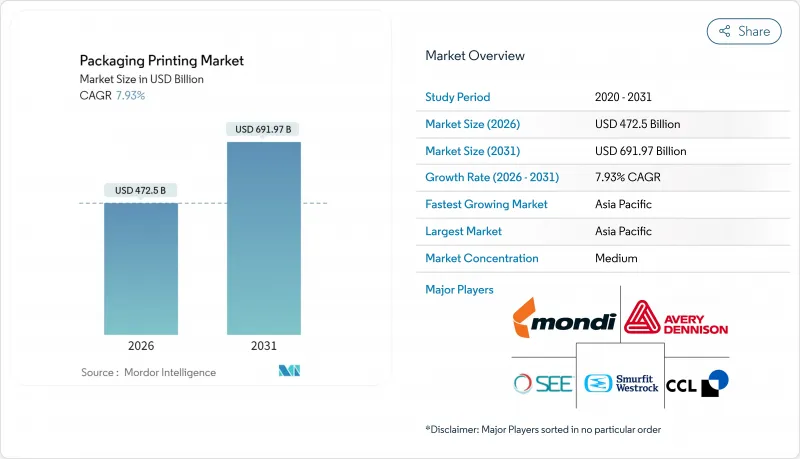

包装印刷市場の規模は、2026年には4,725億米ドルと推定されております。

これは2025年の4,377億8,000万米ドルから成長した数値であり、2031年には6,919億7,000万米ドルに達すると予測されております。2026年から2031年にかけては、CAGR7.93%で成長する見込みです。

急速なデジタル変革、急増する電子商取引活動、そして厳格な持続可能性政策が、技術選定、基材選択、地域別投資優先順位を再構築しています。フレキソ印刷は長尺印刷における生産性により量産面での優位性を維持していますが、ブランドオーナーは現在、SKUの多様化、可変データ、スマートパッケージ機能をサポートする小ロット生産においてデジタルプラットフォームを好んでいます。コンバーターが低エネルギー消費と高速処理を求める中、UV硬化型インク技術が普及を進めており、RFID対応パッケージはサプライチェーンの可視性を強化しています。戦略レベルでは、コンバーターはハイブリッド印刷ライン、地域密着型マイクロファクトリー、クローズドループ素材プログラムを組み合わせ、印刷品質・スピード・環境負荷がブランドロイヤルティを左右する市場において利益率を守っています。

世界の包装印刷市場の動向と洞察

RFID対応およびデジタル印刷の需要

IoT接続の普及により、各パッケージがデータノードへと変貌しつつあります。高付加価値医薬品には、RFIDを埋め込んだ感圧ラベルが標準装備されつつあります。デジタル印刷機は版替えなしでシリアルコードを統合するため、単価を削減しリアルタイム認証を可能にします。消費者向けアプリがこれらの識別子を読み取り、原産地情報やロイヤルティ特典を表示することで、エンゲージメントを深めつつリコール管理を支援します。フレキソ印刷の効率性とインラインインクジェットモジュールを組み合わせたコンバーターは、トレーサビリティ要件を満たし、迅速な対応が評価される契約を獲得しています。

Eコマース包装量の拡大

消費者直送物流では、商品を保護し、グラフィックを際立たせ、迅速に届く軽量フォーマットが優先されます。Gelatoなどのオンデマンド印刷ネットワークは配送距離を90%削減し、アナログ設定からデジタルワークフローへの移行により、地域生産の規模拡大が可能であることを実証しています。小ロット生産(多くの場合1万単位未満)は従来型オフセット印刷の競争力を低下させ、翌日納品可能な店頭品質を実現する高速インクジェット・トナー印刷機への投資を促進しています。開封動画が無料広告となることで包装印刷市場は恩恵を受け、ブランドはより頻繁にデザイン更新を行うよう促されています。

高額な設備投資要件

高速8色フレキソ印刷ラインは最大294万米ドルのコストがかかり、補助スリッター、プレートマウンター、溶剤回収装置も必要です。東南アジアの中小コンバーターは更新を遅らせ、ブランドオーナーがより厳しい公差を要求する中で陳腐化のリスクを負っています。リースプログラムは存在しますが、金利が総所有コストを押し上げます。このため、資金力のあるグループによる家族経営の工場買収が加速し、規模の拡大とより有利な基材契約の交渉が可能となります。

セグメント分析

フレキソ印刷は2025年時点で包装印刷市場規模の34.78%を占めており、フィルムや紙ウェブにおける比類なき高速性が支えています。ハイブリッド印刷プラットフォームでは現在、フレキソユニットにインクジェットステーションを積層することで、連続コードや地域別グラフィックを印刷工程を遅滞させることなく実現しています。デジタル機器は、コンバーターが短納期化とSKUの多様化を追求する中、2031年までに10.15%のCAGRを記録しています。グラビア印刷は、画像忠実度がシリンダー彫刻コストを正当化する高級タバコや化粧品分野でニッチな地位を維持しています。オフセット印刷は折り畳みカートンに集中し、スクリーン印刷やその他のニッチ手法は触感性ニスやメタリック効果に対応しています。

投資データはこの動向を裏付けています。2025年に導入される包装ラインには予知保全センサーが搭載され、予期せぬダウンタイムを18%削減。クラウドベースのカラーサーバーが工場間でアートワークをリアルタイムに調整します。ハイブリッドモデルを採用したコンバーター企業では、準備廃棄物が28%削減され、プロモーション用パッケージの市場投入までの時間(TTM)が半減したと報告されています。こうした状況を受け、設備サプライヤーは印刷機とワークフローソフトウェアをバンドル化し、サービス収益の確保と包装印刷市場におけるアフターマーケット利益率の強化を図っています。

2025年時点で、溶剤系システムは包装印刷市場規模の39.62%のシェアを維持しました。しかしながら、LEDランプが電力消費を1平方メートルあたり0.3~0.5kWhに抑制(熱風乾燥機の1.2~1.8kWhに対し)したことで、UV硬化インクの出荷量はCAGR9.52%で増加しています。水性インクは、食品接触規制によりVOCが制限される紙製品中心の分野で最も急速に成長しています。ラテックスおよびLED-UV技術は、従来水銀灯硬化が不可能だった収縮ラベルや熱感応フィルムへの対応を可能にします。

総コストモデルでは、多品種生産環境においてUVが有利です。版洗浄ステーションが不要となり、溶剤在庫が削減され、オンデマンド硬化により仕掛品が減少します。樹脂の揮発性は依然としてリスクですが、複数調達と社内配合により価格急騰を一部相殺できます。インクサプライヤーは、堆肥化試験に合格するバイオベースモノマーや光開始剤への投資を進めており、化学技術の進歩を包装印刷市場に浸透する持続可能性の課題と整合させています。

地域別分析

アジア太平洋地域は世界の生産量をリードし、2024年の新規印刷機導入の半数以上を占めます。中国のコンバーターは国内スナック需要に対応するため多層パウチラインを増設。インドでは生産連動型インセンティブ制度のもと設備投資優遇措置を実施。ベトナム・タイのフレキシブル包装メーカーはニアショアリングの恩恵を受け、迅速なスイングタグ・ポリ袋を必要とするアパレル輸出業者に供給。越境投資による地域ノウハウの向上と、日本のインクメーカーとの合弁事業が品質安定性を高めています。

北米事業者の技術とコンプライアンスへの取り組み。デジタル段ボール印刷機への投資により、当日配送用ECボックスの生産能力が3倍に拡大。州議会ではリサイクル可能な印刷物を評価する拡大生産者責任制度(EPR)手数料が導入されました。米国コンバーターはUV-LED改造を先導し、25%の省エネルギー効果を主張しています。カナダは食品接触制限をFDAと調和させ、越境調達を容易に。一方メキシコはUSMCA下での無関税アクセスを求めるティア1ブランドを誘致。

欧州は規制のペースを設定しています。同地域の包装材リサイクル率88%目標は、特殊インクを必要とする単一素材ラミネートへのブランドガイドライン転換を促しています。ドイツの機械輸出はリアルタイム粘度制御などのインダストリー4.0機能を活かし、イタリアの印刷機メーカーは高級ブランド獲得に向けインライン冷箔加工を標準装備しています。東欧、特にポーランドは西欧諸国より低い人件費で余剰生産を吸収しつつ、高い技能水準を維持しています。オランダのイノベーション助成金は紙製バリア包装のパイロットラインを資金援助し、包装印刷市場の勢いを維持しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- RFID対応およびデジタル印刷への需要

- 電子商取引包装量の拡大

- 持続可能性への取り組み:環境に優しいインクと基材の推進

- 新興市場における消費ブーム

- ブランドオーナーによるスマートパックシリアル化の導入状況

- 地域密着型オンデマンド印刷マイクロ工場の台頭

- 市場抑制要因

- 多額の資本投資が必要

- 複雑かつ多様化する世界の印刷規制

- 光開始剤および樹脂価格の変動性

- 熟練フレキソ印刷オペレーターの不足

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- マクロ経済的要因が市場に与える影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界エコシステム分析

第5章 市場規模と成長予測

- 印刷技術別

- オフセット印刷

- グラビア印刷

- フレキソ印刷

- デジタル印刷

- その他の印刷技術

- インクの種類別

- 溶剤系インク

- UV硬化型インク

- 水性インク

- ラテックスインク

- LED-UVインク

- 包装材料別

- ラベル

- プラスチック容器およびフィルム

- ガラス容器

- 金属缶および箔

- 紙および板紙カートン

- フレキシブルパウチ

- 段ボール箱およびトレイ

- 最終用途産業別

- 食品・飲料

- 医薬品・ヘルスケア

- 化粧品・パーソナルケア

- 家庭用および産業用

- 電子機器・電気機器

- その他の最終用途産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ベトナム

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor plc

- Smurtfit WestRock

- Tetra Pak Group

- Mondi plc

- Huhtamaki Oyj

- CCL Industries Inc.

- Avery Dennison Corporation

- Sealed Air Corporation

- International Paper Company

- Stora Enso Oyj

- Sonoco Products Company

- Georgia-Pacific LLC

- Constantia Flexibles GmbH

- Mayr-Melnhof Karton AG

- Ahlstrom-Munksj Oyj

- Clondalkin Group Holdings BV

- Autajon Group SA

- SATO Holdings Corp.

- Rotocontrol GmbH