|

市場調査レポート

商品コード

1851165

点滴灌漑:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Drip Irrigation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 点滴灌漑:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

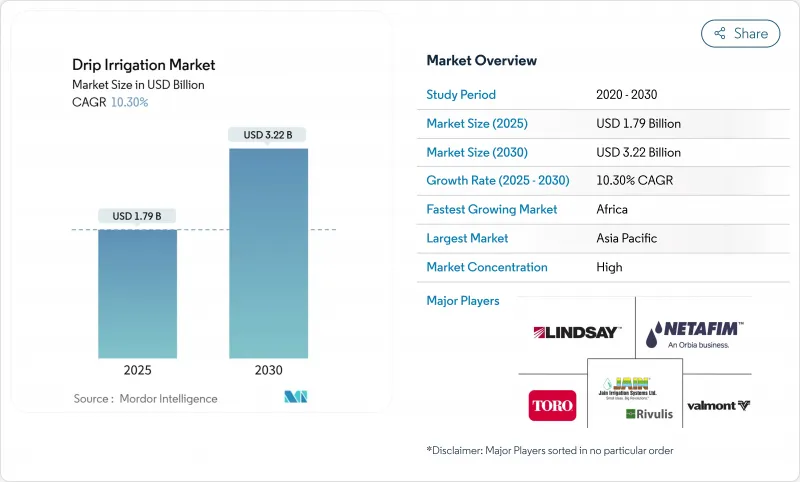

点滴灌漑市場は、2025年の17億9,000万米ドルから2030年には32億2,000万米ドルに拡大し、CAGRは10.3%を記録すると予測されています。

市場拡大の主な要因は、水不足への懸念の高まり、温室栽培の開拓、水効率の高い灌漑システムを義務付ける政府規制の施行などです。戦略的合併による業界再編は技術力を強化し、デジタル農業プラットフォームとの統合はセンサー技術、クラウド分析、露地栽培と保護栽培の両方の環境における圧力補償エミッターを組み込んでいます。製造企業は、小規模農業経営での採用を促進するため、包括的な資金調達と農学サービス・パッケージを導入しています。市場セグメンテーションは、欧州における大幅な成長機会、アジア太平洋におけるかなりの市場プレゼンス、中東とアフリカにおける有利な規制枠組みを示しており、地下灌漑システムとスマートコントローラーが製品セグメントの拡大を支配しています。

世界の点滴灌漑市場の動向と洞察

水不足の脅威

水不足は点滴灌漑市場成長の主な要因であり、根面灌漑システムはオーバーヘッドスプリンクラーに比べて水消費量を最大50%削減します。帯水層レベルの低下と自治体の給水制限により、農業生産者は流出と蒸発を最小限に抑える精密な灌漑方法を採用する必要に迫られています。調査は、干ばつ期間中の水配分の減少と、点滴灌漑の採用増加との間に直接的な関係があることを示しています。この技術は節水だけでなく、雑草の生育の減少や葉面病の発生率の低下など、その他の特典も提供し、収益性を向上させ、市場の継続的拡大を支えています。

政府からの有利な政策と補助金

公的助成プログラムは、市場全体の点滴灌漑導入率に影響を与えます。スペインでは、150万ヘクタールの灌漑網の近代化により、局地的システムが灌漑総面積の48.23%に増加しました。インド、イスラエル、湾岸地域のコストシェア補助金は、初期投資と投資回収期間を短縮しています。バレンシアの調査によると、小規模な協同組合ではメンテナンス費用が補助金を上回ることがあり、設備と継続的なメンテナンス費用の両方をカバーする包括的なプログラムの重要性が浮き彫りになっています。水道料金の引き上げと政策的インセンティブの組み合わせが、点滴灌漑市場の成長を引き続き促進しています。

高額な初期設備投資

点滴灌漑市場では、特に小規模農家が多くクレジットアクセスが限られている地域では、初期コストの高さが依然として大きな障壁となっています。25,000インドルピー(300米ドル)の土壌水分プローブなど、必要不可欠な機器のコストは、ほとんどの零細農家の資金能力を超えています。多国間銀行は、ペイアズ・ユー・グロウ・ローンや機器リース・プログラムのような柔軟な融資オプションを導入していますが、導入率は地域によって異なります。さらに、水不足への懸念が高まっているにもかかわらず、補助金や定額制の水価格設定によって、点滴灌漑システムに投資する経済的インセンティブが低下しています。

セグメント分析

2024年の点滴灌漑市場の62.0%は地表設置型であり、その理由は簡単な設置、効率的なメンテナンス、掘削要件の低減にあります。農業経営者は、ピボット・システムを効率的に変換するために表面ラインを導入し、専門的な設備なしで即座に節水効果を生み出しています。商業農場は、作物の最適な温度制御を維持するため、表面ドリップシステムを葉面ミストと統合し、複数の作物や土壌組成に対応するシステムの汎用性を確保しています。

サブサーフェスシステムは、現在の市場規模は小さいもの、2030年までのCAGRは11.8%と予測されています。これらの設備は、灌漑インフラを機械的損傷から守りつつ、特に乾燥地域では水の蒸発を最小限に抑えます。ワシントンの大学が行った調査によると、地下15cmに設置されたエミッターは、表面流出を大幅に減少させる。水コストの高騰と規制要件の強化が相まって、地下システムの経済性が強化され、点滴灌漑市場における戦略的重要性が確立されています。

エミッターは2024年の売上高の28.5%を占め、これは均一な水流を供給するという重要な役割を反映しています。精密成形と圧力補正技術の向上は、延長された側線にわたって一貫した吐出速度を維持するのに役立ち、必要な圧力ヘッドを低減し、ポンプ1台あたりの圃場カバー範囲を広げることを可能にします。

クラウドに接続されたコントローラー、水分センサー、灌漑バルブなどのスマート灌漑コンポーネントは、CAGR14.6%で成長しています。EPAのデータによると、スマート・コントローラーは計画灌漑を20~43%削減し、統合土壌センサー・システムは干ばつ時の水消費量を最大72%削減できます。ハードウェアのコスト削減とスマートフォンのインターフェイスの改善は、普及を促進します。農業経営者が収量と資源利用を関連付けるにつれて、データ主導の洞察がコントローラーの採用を加速し、市場セグメンテーション市場におけるデジタル分野のシェアを拡大します。

地域分析

アジア太平洋は2024年の売上高の34.9%を占め、インドと中国の地下水枯渇への取り組みが牽引しています。Jain Irrigation社は、衛星画像と現場での遠隔測定を組み合わせた農学アドバイザリーチームを使って、52作物850万エーカーを管理しています。政府補助金と無利子融資により、農家はデジタル監視機能を備えた統合点滴灌漑システムを導入しています。投入コストの上昇と農村から都市への移動が導入率を加速させ、アジア太平洋地域の点滴灌漑市場における支配的地位が強化されます。

アフリカは2030年までのCAGR予測で最速の12.1%を記録。多国間開発プログラムは、小規模農家向けの太陽光発電灌漑システムを支援し、限られた電力インフラに対応します。ケニアとモロッコにおけるMITのGEAR Labイニシアチブは、作動圧力の低減、バッテリー効率の改善、砂質土壌条件下での揚水コスト削減のためにシステムを最適化しています。ケニア、エチオピア、モロッコの輸出向け花卉・野菜生産者は、欧州のトレーサビリティ要件を満たすためにクラウドベースのモニタリングシステムを導入し、地域市場の成長を牽引しています。

欧州市場は、農家の高齢化とともに厳しい水に関する指令を反映しています。欧州市場の成長は、節水規制と農業人口動態の変化を反映しています。スペインでは、10万ヘクタールの近代化のための次世代EU資金が割り当てられる一方、農業人口の高齢化という課題にも取り組んでいます。メーカー各社は、簡素化されたインターフェースとリモート更新機能を備えた、使いやすいコントローラーを開発します。水価格改革により運用コストが増加し、伝統的な農家に点滴灌漑システムの採用を促し、安定した市場需要を維持します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 水不足の脅威

- 政府からの有利な政策と補助金

- 高付加価値温室野菜の総合かんがい需要

- ピボット灌漑から点滴灌漑への転換による労働コスト削減

- 気候変動の影響に適応する地中海のブドウ畑

- 従来の洪水灌漑からマイクロ灌漑システムへ移行する大規模農場

- 市場抑制要因

- 高い初期設備投資

- 複雑なセットアップによる点滴灌漑の損害

- 新興市場におけるアフターサービス網の未整備

- 水道料金の不確実性とROIの抑制

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- アプリケーション

- サーフェス点滴灌漑

- サブサーフェス点滴灌漑

- コンポーネント別

- エミッター/ ドリッパー

- ドリップチューブとライン

- フィルター

- 圧力ポンプ

- バルブと継手

- コントローラーとセンサー

- アクセサリー(ステイク、ジョイナー、プラグ)

- 作物の種類

- 畑作物

- 野菜作物

- 果樹園作物

- ブドウ畑

- その他の作物(商業用および観賞用植物)

- エンドユーザー別

- 商業農場

- 温室とナーサリー

- 住宅用庭園と情勢

- スポーツフィールドとゴルフコース

- 販売チャネル別

- 直接販売

- ディーラーおよび販売店

- オンライン小売

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- インド

- 中国

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 中東・アフリカ

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- その他中東・アフリカ

- 北米

第6章 競合情勢

- 最も採用された戦略

- 市場シェア分析

- 企業プロファイル

- Jain Irrigation Systems Ltd.(Rivulis Irrigation Ltd.)

- The Toro Company

- Netafim Limited(An Orbia Business)

- Rain Bird Corporation

- Valmont Industries, Inc.

- Chinadrip Irrigation Equipment Co. Ltd

- Antelco Pty Ltd

- Sistema Azud

- Metzer Group(Adam Partners)

- DripWorks Inc.

- Mahindra EPC Irrigation Ltd

- Irritec SpA

- Hunter Industries Inc.