|

市場調査レポート

商品コード

1910634

線量計:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Dosimeter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 線量計:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 147 Pages

納期: 2~3営業日

|

概要

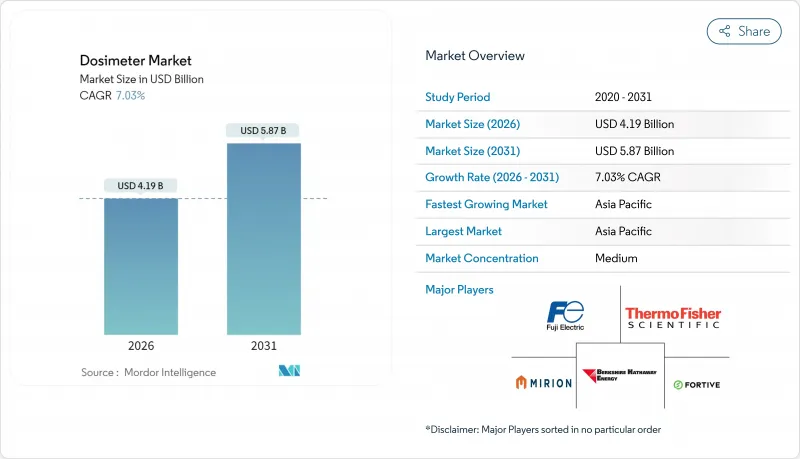

線量計市場は2025年に39億1,000万米ドルと評価され、2026年の41億9,000万米ドルから2031年までに58億7,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは7.03%と見込まれます。

最近の収益拡大は、放射線安全規制の強化、小型モジュール炉の導入、および線量データをリアルタイムで送信する接続型電子個人線量計(EPD)の急速な技術革新と密接に関連しています。国際規制当局が年間許容被ばく線量制限を大幅に引き下げたことを受け、医療機関では眼内レンズモニターの購入量が増加しています。一方、産業用非破壊検査(NDT)チームでは、複数拠点でのコンプライアンス文書化を簡素化する無線バッジへの移行が進んでいます。また、サプライヤーは既存ハードウェアに人工知能(AI)分析機能を組み込み、安全チームが累積被ばく動向を予測し、報告を自動化できるようにしています。アジア太平洋地域では、原子力発電所の建設拡大と診断用画像分野の急成長が相まって、同地域は線量測定ソリューションにおける最大かつ最速で拡大する需要拠点としての地位を確立しています。一方、主要メーカーがニッチ技術企業の買収を継続し、地域サービス拠点を拡大し、長期顧客を確保するサブスクリプション型データプラットフォームを提供しているため、市場は中程度の分散状態が続いています。

世界の線量計市場の動向と洞察

腫瘍画像診断および放射線治療の需要増加

精密放射線治療と高スループット診断画像検査への需要拡大に伴い、継続的なモニタリングを必要とする放射線作業従事者が増加しています。現代の線形加速器は高エネルギーの散乱中性子を放出するため、施設では混合放射線場を捕捉するバブル検出器や半導体バッジの導入が進んでいます。陽子線治療センターでは、複雑な放射線場内の線量分布をマッピングするマルチサイトマイクロ線量計の早期導入が進んでいます。病院では、バッジデータにAIダッシュボードを重ねて管理者が累積被ばく量を予測し、制限値に達する前にスタッフのローテーションを行うことも可能です。その結果、四半期ごとのフィルムバッジから、病院情報システムと統合されたリアルタイムのEPD(推定被ばく線量)への明確な移行が進み、厳格化された職業被ばく制限への準拠が確保されています。

原子力発電容量の拡大(小型モジュール炉および寿命延長プロジェクト)

アジア太平洋地域の数十の電力会社が、小型モジュール炉(SMR)の導入を承認しました。SMRは、従来の原子炉と比較して、設置メガワットあたりの線量計の設置密度を高める必要があります。老朽化した原子炉群の寿命延長プログラムでは、従来のフィルムバッジを、集中管理による線量記録が可能な無線式EPDに置き換えることで、さらなる需要が生じています。ミリオン社などのベンダーは、SMR専用のモニタリングスイートをリリースし、この分野で2桁の収益増加を報告しています。業界のALARA(可能な限り低い放射線量)文化は、より細かい測定粒度を求めており、電力会社は低レベルのガンマ線環境向けに高感度半導体検出器の購入を促進しています。

校正用放射性物質の不足と同位体サプライチェーンの混乱

モリブデン99、セシウム137、コバルト60の慢性的な不足は、校正スケジュールを混乱させ、サービス機関に認証サイクルの延長を余儀なくさせ、バッジの精度に対する信頼を損なっています。新興市場は輸入源に依存し、国内の照射施設が限られているため、最も深刻な影響を受けています。一部の研究所では代替光子源の実験を行っていますが、規制当局は新手法の承認に時間がかかり、認定期間を延長し、バッジ調達を遅らせています。

セグメント分析

電子式個人線量計は2025年に線量計市場の38.72%を占め、施設が即時被曝フィードバックへ移行する中、CAGR8.75%で拡大が見込まれます。無線接続、GPSタグ付け、累積線量動向が加速した際にユーザーへ警告するAI分析技術が本セグメントの強みです。熱蛍光線量計は、実績ある精度を求める価格重視のプログラムに依然として支持されています。一方、光励起蛍光線量計は、迅速な読み取りが重要なニッチ市場で注目を集めています。フィルムバッジは一部発展途上地域で残存していますが、規制当局が迅速な監査サイクルをサポートするシステムを優先する傾向から、そのシェアは縮小を続けています。ハイブリッド型直接イオン蓄積装置は、受動的な長寿命性と電子読み取りの利便性を両立させ、電子線量計の本格導入に慎重な事業者にとって移行経路を円滑にしています。

EPDベンダーは、温度・湿度・気圧を記録する環境センサーを統合し、安全担当者が被ばく量と変化する作業環境を関連付けられるようにしています。大規模な産業施設では、部門横断的な線量分布を可視化するクラウドダッシュボードに接続された数千台の装置が導入されています。ファームウェア更新による新センサー機能の追加により、中間交換サイクルは長期化していますが、SaaS契約による継続的な収益がベンダーロックインを強化しています。

受動型モニタリングは、確立された規制上の受容により、2025年の線量計市場規模の52.10%を占めました。しかしながら、能動型システムは8.52%のCAGRでより急速に成長しています。高線量インターベンショナル心臓病学スイートを導入する病院では、可聴警報とリアルタイム線量ダッシュボードを求め、能動型バッジへの調達を推進しています。原子力発電所では、作業時間が短縮され被ばく線量が急激に変動する停止作業において能動型システムが好まれます。サービスプロバイダーは、制限値追跡を自動化するクラウドベースの分析機能をバンドルし、放射線安全担当者の管理負担を軽減しています。

受動型バッジは、低コスト・軽量・最小限のユーザートレーニングで済むため、大規模スクリーニングプログラムでは依然として人気があります。低所得地域では、政府保健機関が診療所にフィルム式受動型バッジを配布していますが、現在では寄付金によるパイロットプロジェクトで光学刺激ルミネッセンス(OSL)リーダーが導入され、結果の迅速化が図られています。受動型と能動型の両技術を網羅する互換性のあるエコシステムを提供するベンダーは、顧客のアップグレードライフサイクル全体を捉える上で有利な立場にあります。

地域別分析

アジア太平洋地域は2025年に線量計市場で28.45%のシェアを占め、中国・インド・東南アジア諸国が新規原子炉の認可と放射線治療能力の拡大を進める中、8.63%のCAGRで成長を加速しています。中国の原子力建設計画と大規模な同位体生産施設は、電力会社および製薬セグメントにおける安定したバッジ需要を保証します。日本では福島第一原子力発電所事故後の改修においてデジタル線量追跡が優先され、マレーシアとフィリピンでは小型モジュール炉(SMR)の導入が進んでおります。いずれもモジュール式サイト周辺に高密度な個人線量測定ネットワークを必要とします。

北米では旧式原子炉の設置ベースと全国規模の医療用画像装置群が依然として存在します。米国原子力規制委員会によるリアルタイム作業員モニタリングの重視により、病院では四半期ごとのバッジプログラムからリアルタイムEPDダッシュボードへの移行が進んでいます。カナダのCANDU原子炉改修やウラン採掘事業では中性子対応検出器が調達される一方、メキシコの産業用放射線撮影請負業者は、国家の労働衛生規制に対応するためバッジサブスクリプションを拡大しています。

欧州では、原子炉寿命延長プロジェクトに伴う線量計の更新や、閉鎖されたドイツの原子炉を解体する技術者向けに除染チームが装備を整えるなど、導入が徐々に進んでいます。英国の先進炉パイロット事業では、プロジェクト開始時から次世代半導体検出器を統合。GDPR規制が製品設計に影響を与え、サプライヤーはデータ暗号化モジュールの認証取得やオンプレミスサーバーの提供を推進。東欧諸国では小型モジュール炉(SMR)導入を検討する国々が、現地ホスト型線量測定サービス局を設立し、地域販売をさらに促進しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 腫瘍学イメージングおよび放射線治療の需要増加

- 原子力発電容量の拡大(小型モジュール炉および寿命延長プロジェクト)

- 眼レンズ線量制限の強化とリアルタイムコンプライアンス監査

- 産業用放射線検査のデジタル化(配管溶接品質管理、5Gインフラ整備)

- EPDハードウェアと統合されたAI搭載線量解析プラットフォーム

- 新興市場におけるバイオドシメトリー研究所の増加と緊急時対応能力の強化

- 市場抑制要因

- 校正源の不足と同位体サプライチェーンの混乱

- 低エネルギー中性子分野における持続的な精度格差

- データ統合におけるサイバーセキュリティ上の責任

- バッジ処理のサブスクリプション費用によるエンドユーザーの負担感

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- 電子式個人線量計(EPD)

- 熱ルミネッセンス線量計(TLD)

- 光励起発光法(OSL)

- フィルムバッジ

- 直接イオン貯蔵およびDIS-OSL

- 用途別

- アクティブ

- パッシブ

- エンドユーザー産業別

- ヘルスケア

- 原子力発電・燃料サイクル

- 石油・ガス

- 鉱業・金属

- 産業用非破壊検査/製造

- 防衛・安全保障

- 検出技術別

- 半導体(シリコン、炭化ケイ素、PIN)

- シンチレータベース

- ガス充填式GM/比例式

- 固体受動素子(LiF、Al2O3、BeO)

- バブル/過熱滴

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- 東南アジア

- その他アジア太平洋

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Mirion Technologies Inc.

- LANDAUER(Berkshire Hathaway Energy)

- Thermo Fisher Scientific Inc.

- Fuji Electric Co., Ltd.

- Fortive Corp.(Fluke Biomedical)

- ATOMTEX JSC

- Polimaster Ltd.

- Ludlum Measurements Inc.

- Panasonic Industrial Devices

- Arrow-Tech Inc.

- SE International Inc.

- Automess Automation & Measurement GmbH

- Radiation Detection Company Inc.

- Unfors RaySafe AB

- ECOTEST Group Ukraine

- Dosimetrics GmbH

- Kromek Group PLC

- Electronic & Engineering Co.(I)P. Ltd.

- Bubble Technology Industries Inc.

- Qingdao TLead International Co. Ltd.