|

市場調査レポート

商品コード

1940570

英国のファシリティマネジメント:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)United Kingdom (UK) Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のファシリティマネジメント:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

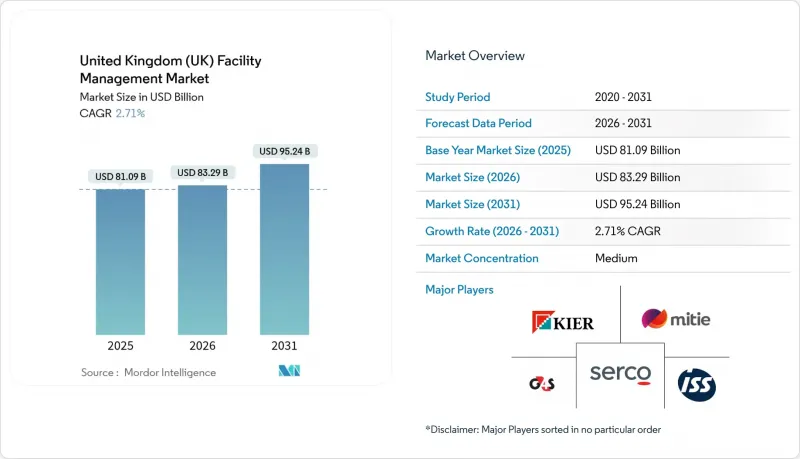

英国のファシリティマネジメント市場は、2025年に810億9,000万米ドルと評価され、2026年の832億9,000万米ドルから2031年までに952億4,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは2.71%と見込まれます。

この測定された成長軌跡は、エネルギー効率化義務、デジタルトランスフォーメーション、そしてアウトソーシングサービスモデルへの持続的な選好の下で進展する成熟したセクターを示しています。ハードサービスは、老朽化した建築ストックが最低エネルギー効率基準を満たすために厳格な機械・電気・配管設備の維持管理を必要とするため、極めて重要です。一方、ソフトサービスは職場のウェルビーイングや厳格な衛生規則に対応するため、急速に進化しています。IoTセンサーネットワークからAIを活用した分析技術に至るまでの技術統合は、対応時間の短縮、エネルギー消費の削減を実現し、人員比率に応じた拡大なしに収益を増加させる成果連動型契約を可能にします。公共・民間クライアントが、変動する投入価格の中でコンプライアンスを保証しコスト確実性を提供する専門的知見を求める中、アウトソーシングの勢いは継続しています。ブレグジット関連の労働力不足とコストインフレが利益率を圧迫する一方、公共部門の改修資金増加とフレキシブルワークスペースの普及は、迅速に革新するプロバイダーにとって拡大の道筋を提供します。

英国(UK)ファシリティマネジメント市場の動向と洞察

技術統合(IoT、AI、自動化)

AI駆動型ビル管理プラットフォームはサービス提供を再定義しており、英国知的財産庁ではデジタル作業指示ポータル導入後、保守対応時間を14日間から数秒に短縮しました。スマートセンサーがリアルタイムの占有率・温度・空気質データを送信することで、プロバイダーは事後対応型から予知保全へ移行しつつ、エネルギー使用量の削減と従業員の快適性向上を実現しています。CBREがハイパースケールデータセンターのファシリティマネジメントに参入したことは、24時間体制の分析的監視を必要とする分野における高収益の可能性を裏付けています。医療・教育分野の顧客が導入を主導している背景には、コンプライアンス体制による継続的な環境監視の義務化があります。デジタルダッシュボードがソフトサービスとハードサービスを統合する中、プロバイダーは清掃、セキュリティ、オフィスサポート、資産保守をデータ豊富な契約にパッケージ化し、価格プレミアムを獲得しています。

商業用不動産の急速な拡大

英国王立チャータード測量士協会(RICS)のデータによれば、2025年第1四半期にテナント需要がプラスに転じ、ロンドン中心部の優良オフィス賃料は年間で約5%上昇が見込まれます。産業用資産は投資意欲が最も強く、eコマースとニアショアリングの推進により投資家需要のネットバランスが+18%を記録しています。新規開発により、コミッショニング、ライフサイクル資産管理、継続的なコンプライアンス監査の需要が増加しています。開発業者と早期に提携するファシリティマネジメント者は、初日からESGダッシュボードを統合したスマート対応ビルにおいて、複数年にわたる収益源を確保します。同様に、物流の成長は、高処理能力倉庫向けに在庫追跡技術、ドック管理、高度な消火設備メンテナンスを組み合わせた特注のFMパッケージを推進しています。

労働力不足とスキルギャップ

ホスピタリティ、清掃、ケータリング部門では、ブレグジット後に13万2,000件の職位が空席となり、FM要員の確保が困難な状況です。2025年移民政策白書では、熟練労働者ビザの要件がRQFレベル6に引き上げられ、FMの初級職における国際人材の採用が制限されます。雇用主による研修投資は2005年以降28%減少しており、建物が高度なデジタルシステムを導入するまさにそのタイミングで技能不足が生じています。企業はSamsicのJPCによる12モジュール構成の次世代プログラムなど、リーダーシップと技術的スキル向上に焦点を当てた監督者養成アカデミーで対応しています。しかしながら、高い離職率と労働力の高齢化が引き続き業界の能力を制限しています。

セグメント分析

2025年時点で、ハードサービスは英国ファシリティマネジメント市場の60.12%を占めております。これは、NHS(国民保健サービス)の116億ポンド(31億9,000万米ドル)に上る保守遅延と、厳格なエネルギー性能証明書(EPC)基準達成期限に支えられたものです。英国のファシリティマネジメント市場において、ハードサービス契約の規模は拡大が見込まれます。商業施設の28%が依然としてエネルギー性能評価(EPC)でD等級以下と評価されており、機械・電気・配管設備の改修が急務となっているためです。MEP(機械・電気・配管)およびHVAC(冷暖房換気空調)分野は、2035年までに47~62%の排出量削減を義務付けるネットゼロ規制の道筋から恩恵を受けています。資産のデジタル化は、予測保全分析の需要をさらに押し上げ、プロバイダーが資産故障前に介入できると同時に、コンプライアンス報告要件を満たすことを可能にします。

ソフトサービスは現在規模が小さいもの、病院レベルの清掃基準や職場体験の革新により、2031年までCAGR2.78%で拡大が見込まれます。感染管理規則の強化により、ロボット消毒システムやセンサー検証型衛生プロトコルの需要が高まっています。コワーキング事業者にはスマートアクセス制御が求められ、セキュリティサービスの近代化を推進しています。グレネル火災後の法規制に伴う防火安全対策の強化により、統合警報テストと避難計画サービスの需要が増大しています。これらの要因が相まって、プロバイダーの提供内容は、ソフトサービスの卓越性とデータに基づくコンプライアンスを融合した包括的なパッケージへと移行しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 現在の稼働率

- 主要FM事業者の収益性率

- 労働力指標- 労働参加率

- サービス種類別ファシリティマネジメント市場シェア(%)

- ファシリティマネジメント市場シェア(%)、ハードサービス別

- ソフトサービス別ファシリティマネジメント市場シェア(%)

- 主要都市圏における都市化と人口増加

- 英国インフラ整備計画におけるセクター別投資優先順位

- 労働基準および安全基準に特化した規制上の促進要因

- 市場促進要因

- 商業用不動産の急速な拡大

- 技術統合(IoT、AI、自動化)

- アウトソーシングの増加動向

- 職場体験と従業員のウェルビーイングへの注目の高まり

- 厳格なエネルギー効率規制およびネットゼロ規制

- 柔軟なワークスペースの台頭によるアジャイルFM契約の必要性

- 市場抑制要因

- 労働力不足とスキルギャップ

- 運営コスト上昇による利益率の圧力

- サービス標準化を阻害する断片化されたサプライヤーエコシステム

- スマートビルシステムにおけるデータセキュリティ上の懸念

- バリューチェーン分析

- PESTEL分析

- 新規参入企業向けの規制・法的枠組み

- マクロ経済指標がFM需要に与える影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資と資金調達分析

第5章 市場規模と成長予測

- サービスタイプ別

- ハードサービス

- アセットマネジメント

- MEPおよびHVACサービス

- 消防設備・安全対策

- その他のハードFMサービス

- ソフトサービス

- オフィスサポートおよびセキュリティ

- 清掃サービス

- ケータリングサービス

- その他のソフトFMサービス

- ハードサービス

- 提供タイプ別

- 自社管理

- 外部委託

- 単一FM

- 包括的ファシリティマネジメント(Bundled FM)

- 統合型ファシリティマネジメント(Integrated FM)

- エンドユーザー業界別

- 商業施設(IT・通信、小売・倉庫など)

- ホスピタリティ(ホテル、飲食店、大規模レストラン)

- 公共・公共インフラ(政府機関、教育機関、輸送機関)

- 医療(公的・民間施設)

- 工業・プロセス(製造業、エネルギー、鉱業)

- その他のエンドユーザー産業(集合住宅、娯楽、スポーツ・レジャー)

第6章 競合情勢

- 市場集中度

- 戦略的動向と提携関係

- 市場シェア分析

- 企業プロファイル

- ISS UK

- Mitie Group PLC

- Serco Group PLC

- Kier Group PLC

- G4S Facilities Management UK Limited

- Sodexo Facilities Management Services

- Compass Group

- Equans

- VINCI Facilities Limited

- Aramark Facilities Services

- Andron Facilities Management

- CSM Facilities Management Group

- Orton Group

- Global Facilities.

- BGIS