航空機防火システム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Aircraft Fire Protection Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 102 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687966

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

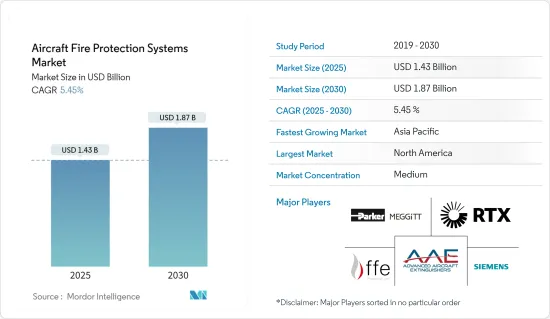

航空機防火システム市場規模は2025年に14億3,000万米ドルと予測され、予測期間(2025-2030年)のCAGRは5.45%で、2030年には18億7,000万米ドルに達すると予測されます。

主なハイライト

- 近年、航空旅行の急増と航空技術の進歩が航空機防火システムの需要を押し上げています。世界中の航空当局が課す厳しい安全規制が、市場の重要性を強調しています。米国連邦航空局(FAA)、欧州連合航空安全機関(EASA)、中国民用航空局(CAAC)などの規制機関は、防火安全基準とコンプライアンスの形成に重要な役割を果たしています。

- 業界の成長軌道は基本的に航空セクターの成長に依存しており、主要なプレーヤーはその将来を形作る上で極めて重要な役割を果たしています。市場が発展するにつれ、航空業界における最高水準の安全性を世界的に確保するためには、業界のリーダーと規制機関の協力が不可欠となっています。高度な火災検知システム、警報・警告システム、各商用・軍用機用の高度な消火システムなど、包括的な技術がこの市場のソリューションを構成しています。これらの技術は、厳格な国際安全基準や規制に基づいて運用されています。

- しかし、適切な航空インフラが整備されていないことや、新興国での追加的な航空税の賦課は、航空機の販売を妨げ、それによって市場の見通しに水を差す可能性があります。

航空機防火システム市場動向

商用航空機セグメントが予測期間中に最も高い成長を示す

商用航空機セグメントは予測期間中に著しい成長を示すと予測されます。この成長の背景には、航空機納入数の増加と高度な防火システムに対する需要の高まりがあります。防火システムは、乗客や貨物の安全を確保するために、あらゆるタイプの旅客機や貨物機に装備することが義務付けられています。そのため、防火システムの成長は予測期間中の商用航空機の成長に直結します。航空旅客数の増加に伴い、商用航空機の調達もCOVID-19の影響からの回復後に急増しました。

航空会社は、世界中で増大する旅客需要に対応するため、巨額の発注を行っています。2023年12月現在、エアバスは約2,000機の航空機を受注しており、ボーイングは約1,200機で2位を占めています。このうち、インディゴは2023年6月にA320ファミリーを500機発注しており、商用航空業界最大の受注を維持しています。さらに、エミレーツ航空は2023年11月、ボーイングB777ワイドボディ機95機(520億米ドル相当)の発注を発表しました。このような受注は、防火システムメーカーが巨大市場を獲得する機会を高めることを目的としています。これらの航空機は予測期間を通じて納入されると予想され、それによって航空機に取り付ける必要がある防火システムの成長を直接促進します。

予測期間中、北米が市場を独占

潤沢な資金を持つ航空産業が存在し、航空機保有台数が最も多く、航空分野への支出が増加していることから、北米は予測期間中も市場シェアの支配を続けると予想されます。航空交通量の増加は、この地域の地域航空会社や国際航空会社による複数の航空機の調達につながりました。米国を本拠地とする大手航空機OEMの1つであるボーイングは、航空機防火システムに膨大な需要を生み出しています。連邦航空局(FAA)がすべての現役航空機に避難システムの設置を義務付けているため、OEMが航空機の新規注文を受けると同時に、商用航空機用防火システムにも需要が発生します。

原材料の入手可能性、政治的安定性、生産コストの低さといった要因が、この地域における新たな航空宇宙製造施設の設立を後押ししました。例えば、米国空軍(USAF)は、制空権2030プログラムの一環として、ペネトレイト・カウンター・エアーと呼ばれる2機の新型ハイテク戦闘機の開発を進めています。高度な兵器を統合するためには、航空機の重要なコンポーネントの誤作動によって引き起こされる軽微な火災でも検知するための高度な火災検知システムを統合する必要があります。

一方、火災の拡大を食い止め、航空機の他のシステムに対する巻き添え被害を最小限に抑えるためには、同様に高度な消火システムが必要となります。このように、乗客のセキュリティ強化への注目の高まりと航空機納入数の増加が、この地域全体の市場を牽引しています。

航空機防火システム産業の概要

航空機防火システム市場は半固有の性質を持っており、市場において重要なシェアを持つ少数のローカルおよび世界プレーヤーが存在しています。市場の主要企業としては、Parker-Meggitt(Parker Hannifin Corporation)、RTX Corporation、Siemens AG、FFE Ltd、Advanced Aircraft Extinguishers Ltd.などが挙げられます。一般に、この市場のプレーヤーは長期契約を結んでおり、航空業界で航空機の需要があれば、企業は一定の利益を含めることができます。

パーカー・メギット(パーカー・ハニフィン・コーポレーション)とRTXコーポレーションは、商用航空機やビジネスジェットの大半に防火ソリューションを提供しているため、かなりの市場シェアを占めています。RTXコーポレーションは、エアバスA220、イルクートMC-21-300、エアバスA380、ボーイングB767、COMAC C919、ガルフストリームG280、ガルフストリームG650などに防火システムを提供しています。一方、Meggitt PLCは、エアバスA320、エアバスA330、エアバスA350 XWB、エアバスA380、エアバスA400M、ボーイングB737、ボーイングB777、ボーイングF/A-18スーパーホーネット、エンブラエルE-Jet 170シリーズ、エンブラエルE-Jet 190シリーズ、エンブラエルERJ-145シリーズなどの航空機プログラムに提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 火災検知システム

- 警報・警告システム

- 消火システム

- 航空機タイプ

- 商用航空機

- 軍用機

- 一般航空機

- 用途

- キャビンおよび化粧室

- コックピット

- 貨物室

- エンジンおよびAPU

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- RTX Corporation

- Meggitt(Parker Hannifin Corporation)

- Siemens AG

- H3R Aviation Inc.

- AMETEK Inc.

- Advanced Aircraft Extinguishers, Ltd.

- Gielle Group

- Diehl Stiftung & Co. KG

- FFE Ltd.

- Curtiss-Wright Corporation

- Southern Electronics Pvt Ltd

- Amerex Corporation

- Aerocon Engineering

- Hazard Control Technologies, Inc.

第7章 市場機会と今後の動向

目次

The Aircraft Fire Protection Systems Market size is estimated at USD 1.43 billion in 2025, and is expected to reach USD 1.87 billion by 2030, at a CAGR of 5.45% during the forecast period (2025-2030).

Key Highlights

- In recent years, a surge in air travel and advancements in aviation technologies have propelled the demand for aircraft fire protection systems. Stringent safety regulations imposed by aviation authorities worldwide underscore the market's importance. Regulatory bodies such as the Federal Aviation Administration (FAA) in the United States, the European Union Aviation Safety Agency (EASA), and the Civil Aviation Administration of China (CAAC) play critical roles in shaping fire safety standards and compliance.

- The industry's growth trajectory is fundamentally dependent to the growth of the aviation sector, with key players playing a pivotal role in shaping its future. As the market evolves, collaboration between industry leaders and regulatory agencies remains critical to ensuring the highest standards of safety in aviation globally. A comprehensive range of technologies constitutes the market's solutions, including advanced fire detection systems, alarm and warning systems, and sophisticated fire suppression systems for various commercial and military aircraft. These technologies operate by stringent international safety standards and regulations.

- However, the lack of proper aviation infrastructure and the imposition of additional aviation taxes in emerging economies may hamper aircraft sales and thereby dampen market prospects.

Aircraft Fire Protection Systems Market Trends

Commercial Aircraft Segment Will Showcase Highest Growth during the Forecast Period

The commercial aircraft segment is projected to show remarkable growth during the forecast period. The growth is attributed to the increasing number of aircraft deliveries and rising demand for advanced fire protection systems. Fire protection systems are mandatory to be equipped on all types of passenger and cargo aircraft to ensure the safety of passengers and cargo. Therefore, the growth of the fire protection systems is directly related to the growth of commercial aircraft during the forecast period. With an increase in air passenger traffic, procurement of commercial aircraft also saw a surge after the recovery from the COVID-19 impact.

Airlines are placing huge orders to meet the growing demand for passenger travel across the world. As of December 2023, Airbus has orders for around 2,000 aircraft while Boeing is leading second at around 1,200 orders. Out of these orders, Indigo's order of 500 A320 family aircraft in June 2023 has remained the largest order in the commercial aviation industry. In addition, in November 2023, Emirates also announced an order of 95 Boeing B777 wide-body aircraft worth USD 52 billion. Such orders are aimed at enhancing the opportunities for fire protection system manufacturers to capture huge market. These aircraft is expected to delivered through the forecast period, thereby directly driving the growth of fire protection systems that needs to be installed onto the aircraft.

North America Dominates the Market During the Forecast Period

Due to the presence of a well-financed aviation industry, the highest aircraft fleet, and rising spending on the aviation sector, North America is expected to continue its market share domination during the forecast period. Higher air traffic resulted in the procurement of several aircraft by regional and international airline operators in the region. Boeing, one of the major aircraft OEMs based in the US, generates a huge demand for aircraft fire protection systems. As the OEMs receive new orders for aircraft, the demand is simultaneously generated for commercial aircraft fire protection systems, as the FAA mandates the installation of evacuation systems in all active aircraft.

Factors such as the availability of raw materials, political stability, and low production costs drove the establishment of new aerospace manufacturing facilities in the region. For instance, as part of its Air Superiority 2030 program, the US Air Force (USAF) is developing a pair of two new high-tech fighter aircraft, dubbed the Penetrating Counter Air. The integration of advanced weaponry necessitates the integration of sophisticated fire detection systems to detect even minor fires caused by the malfunction of any critical component of the aircraft.

In contrast, a similarly advanced fire suppression system is required to contain the spread of the fire and ensure minimal collateral damage to other systems of the aircraft. Thus, increasing focus on enhancing passenger security and the rising number of aircraft deliveries is driving the market across the region.

Aircraft Fire Protection Systems Industry Overview

The aircraft fire protection systems market is semi-consolidated in nature, with a presence of few local and global players with significant shares in the market. Some of the key players in the market are Parker-Meggitt (Parker Hannifin Corporation), RTX Corporation, Siemens AG, FFE Ltd, and Advanced Aircraft Extinguishers Ltd. Generally, the players in the market receive long-term contracts, and this allows the companies to include constant profits if there is demand for aircraft in the aviation industry.

A substantial market share is dominated by Parker-Meggitt (Parker Hannifin Corporation) and RTX Corporation, as they provide fire safety solutions for the majority of commercial aircraft and business jets. RTX Corporation provides fire protection systems to Airbus A220, Irkut MC-21-300, Airbus A380, Boeing B767, COMAC C919, Gulfstream G280, Gulfstream G650, etc. while, Meggitt PLC provides for aircraft programs like Airbus A320, Airbus A330, Airbus A350 XWB, Airbus A380, Airbus A400M, Boeing B737, Boeing B777, Boeing F/A-18 Super Hornet, Embraer E-Jet 170 series, Embraer E-Jet 190 series, and Embraer ERJ-145 series, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Fire Detection Systems

- 5.1.2 Alarm and Warning Systems

- 5.1.3 Fire Suppression Systems

- 5.2 Aircraft Type

- 5.2.1 Commercial Aircraft

- 5.2.2 Military Aircraft

- 5.2.3 General Aviation Aircraft

- 5.3 Application

- 5.3.1 Cabin and Lavatories

- 5.3.2 Cockpit

- 5.3.3 Cargo Compartment

- 5.3.4 Engine and APU

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 RTX Corporation

- 6.2.2 Meggitt (Parker Hannifin Corporation)

- 6.2.3 Siemens AG

- 6.2.4 H3R Aviation Inc.

- 6.2.5 AMETEK Inc.

- 6.2.6 Advanced Aircraft Extinguishers, Ltd.

- 6.2.7 Gielle Group

- 6.2.8 Diehl Stiftung & Co. KG

- 6.2.9 FFE Ltd.

- 6.2.10 Curtiss-Wright Corporation

- 6.2.11 Southern Electronics Pvt Ltd

- 6.2.12 Amerex Corporation

- 6.2.13 Aerocon Engineering

- 6.2.14 Hazard Control Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 102 Pages

- 納期

- 2~3営業日