航空機防火システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Aircraft Fire Protection Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750361

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

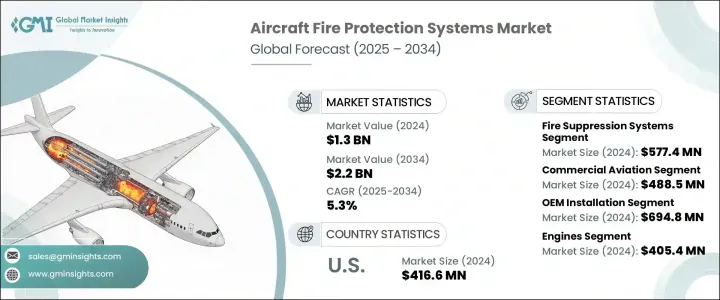

世界の航空機防火システム市場は、2024年に13億米ドルと評価され、世界の航空需要の高まりと、防衛用途での無人航空機(UAV)やドローンの使用増加により、CAGR 5.3%で成長し、2034年には22億米ドルに達すると推定されています。

世界の旅客輸送量の増加が続く中、特にアジア太平洋、中東・アフリカのような急速に拡大している地域では、新型航空機の需要が大幅に急増しています。これらの地域では、経済成長、都市化、中産階級の人口増加が進んでおり、これらすべてが航空旅行の需要を促進しています。その結果、航空業界では航空機の新規発注が増加し、乗客と航空機の安全を確保するための効率的で信頼性の高い高度な防火システムの必要性が高まっています。

こうした需要の高まりに対応するため、メーカー各社は、煙探知器、火炎探知器、エンジン・貨物火災抑制システムなど、堅牢な火災探知・抑制技術の提供に注力しています。これらのシステムは、潜在的な火災の危険性を特定して対応するよう設計されており、乗客と航空機自体の両方を保護するための迅速な行動を保証します。防火システムのもう一つの重要な構成要素である客室用消火器も、客室内で発生する可能性のある火災の制御と消火に重要な役割を果たし、民間航空機の全体的な安全基準を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 13億米ドル |

| 予測金額 | 22億米ドル |

| CAGR | 5.3% |

航空産業の拡大に伴い、メーカーは防火システムの需要増に対応することに注力しています。民間航空セグメントは、2024年に4億8,850万米ドルを生み出しました。世界の旅客輸送量の急増に伴い、航空機の増便や新型機の納入の必要性が高まっています。航空会社やOEMは、安全規制を遵守するために高度な防火技術を統合しています。さらに、電気航空機や垂直離着陸機(eVTOL)の台頭により、リチウムイオン電池がもたらすリスクに対処するための特殊な消火システムの需要が高まっています。

消火システム市場は最大セグメントで、2024年の市場規模は5億7,740万米ドルでした。この背景には、航空機の生存性と乗客の安全性が重視されるようになっていることがあります。また、長距離機や超長距離機の採用により、消火システムの需要も高まっています。さらに、戦闘機やUAVなどの軍事分野では、高い運用効率と安全性を確保するために消火システムが組み込まれています。

米国航空機防火システム2024年の市場は4億1,660万米ドルを占め、大規模な民間および一般航空機に支えられています。新しい航空機モデルの統合など、継続的な航空機の近代化に伴い、高度な防火技術に対する需要が高まっています。さらに、次世代軍用機への投資も最先端の消火システムの需要に貢献しています。

航空機防火システム市場の主要企業には、 Siemens, Collins Aerospace, Hazard Control Technologies, Curtiss-Wright, and Diehl Stiftung. などがあります。これらの企業は、航空業界の進化するニーズに応える最先端のソリューションを提供することに注力しています。市場での地位を強化するため、航空機防火システム分野の企業はいくつかの戦略を採用しています。特に効率性、軽量化、IoTベースのモニタリングシステムとの統合など、製品の性能を高めるための研究開発に投資している企業が多いです。OEM、軍事請負業者、航空会社とのコラボレーションも、長期契約を確保するための重要な戦略です。さらに、防火製品のリサイクル性や持続可能性の向上に注力している企業もあり、環境意識の高い顧客にアピールしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 世界の航空旅客数の増加

- キャビンと貨物室の安全性に重点を置く

- 防衛における無人航空機とドローンの利用増加

- 電気航空機とハイブリッド航空機の導入

- 格安航空会社(LCC)の拡大

- 業界の潜在的リスク&課題

- 技術統合の複雑さ

- 設置および保守コストが高め

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021 –2034

- 主要動向

- 火災検知システム

- 煙探知器

- 熱探知機

- 炎検知器

- ガス検知器

- その他

- 警報および警告システム

- 消火システム

- 消火スプリンクラー

- 消火器

- ガス消火システム

- 泡消火システム

第6章 市場推計・予測:プラットフォーム別、2021 –2034

- 主要動向

- 商用航空

- ナローボディ機

- ワイドボディ機

- リージョナルジェット

- 軍事航空

- 戦闘機

- 輸送機および偵察機

- 軍用ヘリコプター

- ビジネスおよび一般航空

- 無人航空機(UAV)

第7章 市場推計・予測:適合別、2021 –2034

- 主要動向

- OEMインストール

- アフターマーケット

第8章 市場推計・予測:用途別、2021 –2034

- 主要動向

- 航空機の貨物室

- エンジン

- 補助動力装置(APU)

- キャビンとトイレ

- コックピット

- その他

第9章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Advanced Aircraft Extinguishers

- Amerex

- Collins Aerospace

- Curtiss-Wright

- Diehl Stiftung

- FFE

- Gielle Group

- H3R Aviation

- Hazard Control Technologies

- Meggitt

- Siemens

- Southern Electronics

目次

The Global Aircraft Fire Protection Systems Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 2.2 billion by 2034, driven by the rising global demand for air travel and the increasing use of unmanned aerial vehicles (UAVs) and drones in defense applications. As global passenger traffic continues to rise, there is a significant surge in the demand for new aircraft, especially in rapidly expanding regions like Asia Pacific, the Middle East, and Africa. These regions are experiencing economic growth, urbanization, and an increasing middle-class population, all driving the demand for air travel. Consequently, the aviation industry is seeing a higher volume of new aircraft orders, increasing the need for efficient, reliable, and advanced fire protection systems to ensure passenger and aircraft safety.

To meet these rising demands, manufacturers focus on providing robust fire detection and suppression technologies, such as smoke detectors, flame detectors, and engine and cargo fire suppression systems. These systems are designed to identify and respond to potential fire hazards, ensuring swift action to protect both passengers and the aircraft itself. Cabin fire extinguishers, another essential component of fire protection systems, also play a critical role in controlling and extinguishing fires that may occur in the cabin, enhancing the overall safety standards of commercial aircraft.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 5.3% |

With the expansion of the aviation industry, manufacturers are focused on meeting the growing demand for fire protection systems. The commercial aviation segment generated USD 488.5 million in 2024. As global passenger traffic surges, there is a greater need for fleet expansion and the delivery of new aircraft. Airlines and OEMs integrate advanced fire protection technologies to comply with safety regulations. Additionally, the rise of electric aircraft and vertical takeoff and landing (eVTOL) vehicles is driving demand for specialized fire suppression systems to address the risks posed by lithium-ion batteries.

The fire suppression systems market was the largest segment, valued at USD 577.4 million in 2024. This is driven by increasing emphasis on aircraft survivability and passenger safety. The demand for fire suppression systems is also rising due to the adoption of long-haul and ultra-long-range aircraft. Furthermore, the military sector, including combat aircraft and UAVs, incorporates fire suppression systems to ensure high operational efficiency and safety.

United States Aircraft Fire Protection Systems Market accounted for USD 416.6 million in 2024, supported by a large commercial and general aviation fleet. With continuous fleet modernization, such as the integration of new aircraft models, there is ongoing demand for advanced fire protection technologies. Additionally, investments in next-generation military aircraft further contribute to the demand for state-of-the-art fire suppression systems.

Key players in the aircraft fire protection systems market include Siemens, Collins Aerospace, Hazard Control Technologies, Curtiss-Wright, and Diehl Stiftung. These companies are focused on offering cutting-edge solutions to meet the evolving needs of the aviation industry. To strengthen their market position, companies in the aircraft fire protection systems sector are adopting several strategies. Many are investing in research and development to enhance the performance of their products, particularly in terms of efficiency, weight reduction, and integration with IoT-based monitoring systems. Collaboration with OEMs, military contractors, and airlines is another key strategy to secure long-term contracts. Additionally, some companies are focusing on improving the recyclability and sustainability of their fire protection products, which appeals to environmentally conscious customers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising global air passenger traffic

- 3.3.1.2 Focus on cabin and cargo compartment safety

- 3.3.1.3 Growing use of UAVs and drones in defense

- 3.3.1.4 Adoption of electric and hybrid aircraft

- 3.3.1.5 Expansion of low-cost carriers (LCCS)

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Technological integration complexity

- 3.3.2.2 High installation and maintenance costs

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Fire detection systems

- 5.2.1 Smoke detectors

- 5.2.2 Heat detectors

- 5.2.3 Flame detectors

- 5.2.4 Gas detectors

- 5.2.5 Others

- 5.3 Alarm & warning systems

- 5.4 Fire suppression systems

- 5.4.1 Fire sprinkler

- 5.4.2 Fire extinguishers

- 5.4.3 Gas-based suppression systems

- 5.4.4 Foam-based suppression systems

Chapter 6 Market Estimates and Forecast, By Platform Type, 2021 – 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Commercial aviation

- 6.2.1 Narrow-body aircraft

- 6.2.2 Wide-body aircraft

- 6.2.3 Regional jets

- 6.3 Military aviation

- 6.3.1 Fighter jets

- 6.3.2 Transport & reconnaissance aircraft

- 6.3.3 Military helicopters

- 6.4 Business & general aviation

- 6.5 Unmanned aerial vehicles (UAVs)

Chapter 7 Market Estimates and Forecast, By Fitment, 2021 – 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 OEM installation

- 7.3 Aftermarket

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Aircraft cargo compartments

- 8.3 Engines

- 8.4 Auxiliary power units (APU)

- 8.5 Cabins & lavatories

- 8.6 Cockpits

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Advanced Aircraft Extinguishers

- 10.2 Amerex

- 10.3 Collins Aerospace

- 10.4 Curtiss-Wright

- 10.5 Diehl Stiftung

- 10.6 FFE

- 10.7 Gielle Group

- 10.8 H3R Aviation

- 10.9 Hazard Control Technologies

- 10.10 Meggitt

- 10.11 Siemens

- 10.12 Southern Electronics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日