|

市場調査レポート

商品コード

1910620

光変調器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Optical Modulators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 光変調器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 158 Pages

納期: 2~3営業日

|

概要

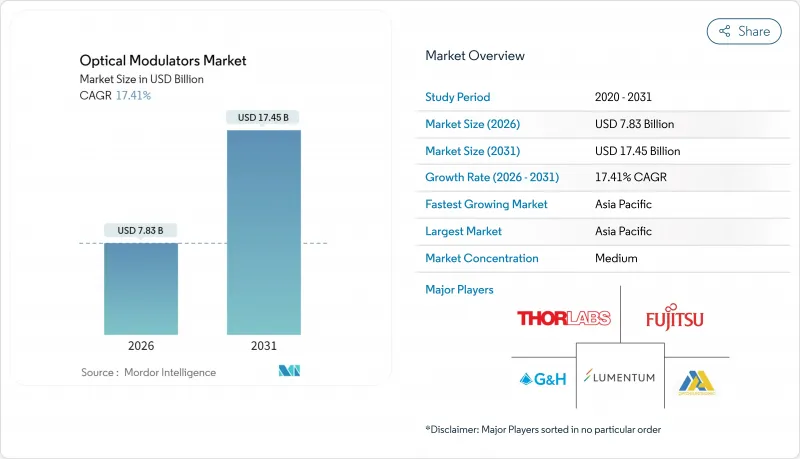

光変調器市場は、2025年の66億7,000万米ドルから2026年には78億3,000万米ドルへ成長し、2026年から2031年にかけてCAGR17.41%で推移し、2031年までに174億5,000万米ドルに達すると予測されています。

この成長軌跡は、800Gおよび1.6T光通信、ハイパースケールデータセンターの展開、初期段階の量子コンピューティングネットワークなど、いずれも高速化を続ける電気光学部品に依存する分野における帯域幅需要の加速を反映しています。ベンダー各社は、コパッケージド光学部品内の熱設計要件を満たすため、位相安定性と低駆動電圧設計を優先しています。一方、薄膜ニオブ酸リチウムやシリコンフォトニクスにおける材料革新がコスト構造を変革中です。スイッチASICベンダーが100ギガバウド以上に対応した光エンジンを要求する中、集積変調器チップはニッチ市場から主流へと移行しつつあります。一方、新興経済国の政策立案者は、5GバックホールおよびFTTH(Fiber-to-the-Home)向けに周波数帯域と補助金を継続的に割り当てており、50~100Gbpsクラスの大規模導入が持続しています。

世界の光変調器市場の動向と洞察

光ファイバー通信インフラへの投資増加

クラウドプロバイダーがビット単価の低減を追求する中、記録的なAIクラスター構築により、2024年には800Gトランシーバーの出荷台数が2,000万台を突破しました。400Gから800Gへの移行、およびCiena社の224G SerDesを用いた1.6Tコヒーレントライト実証など初期の1.6T技術実証により、モジュレータは電力予算を破綻させることなく100Gbaudのシンボルレートを達成することが求められています。リニア・プラグ可能光モジュールの市場規模は、2024年の50億米ドルから2026年までに100億米ドル以上に倍増し、コンパクトで低Vπアーキテクチャへの短期的な需要を加速させています。コパッケージド光モジュール内部の熱設計マージンは縮小傾向にあり、同一基板上でドライバICと変調器の導波路を共同最適化できる統合サプライヤーが優位性を発揮します。スイッチASICのロードマップが51Tおよび102Tファブリックを確定するにつれ、光エンジンの搭載率が加速し、短期的なCAGRに対するドライバの好影響がさらに強まります。

新興国における5GおよびFTTHの展開加速

インドでは5Gサービス開始後、月間光ファイバー敷設量が101,550kmに急増し、5G導入前の6倍に達しました。これは「基地局の70%光ファイバー化」といった政策目標が、実際の光部品需要に直結する実例です。各スモールセルには最低1本の25Gまたは50G光フロントホールリンクが必要となるため、コストと耐熱性に最適化された変調器は大量発注が見込まれます。中国のクラウド事業者は2024年に20~30億米ドル規模の国内トランシーバー市場を創出し、変調器製造工場に波及する地域調達サイクルを強化しました。広範な環境条件下でのデバイス認証を取得できるベンダーは、公共通信入札において優先サプライヤーの地位を獲得し、中期的な成長見通しを高めています。

100Gbaudを超える設計の複雑性と熱管理の限界

シンボルレートを100ギガボーデ超に押し上げることは、熱負荷を増大させ、マイクロ波信号と光信号の速度整合に課題をもたらします。MITリンカーン研究所のインダクタンス調整電極は、50オームのインピーダンスを維持しながら100GHzを超える帯域幅を実現しますが、こうした革新技術を量産可能なモジュールに組み込むことは依然として困難です。特殊基板や液体金属熱ビアは部品コストを押し上げ、認証サイクルを長期化させるため、短期的供給多様性を制限し、CAGRを抑制する要因となります。

セグメント分析

位相変調器は、コヒーレント検出の基盤技術として、2025年の光変調器市場シェアの37.65%を占めました。しかしながら、集積モジュレーターチップは18.05%という最も高いCAGRで推移する見込みです。これは、コパッケージド光学素子が単一基板設計に依存し、電力と遅延を削減するためです。タワーセミコンダクターのようなファウンドリがレーンあたり400Gビットのユニットを認定するにつれ、集積チップに関連する光モジュレーター市場規模は拡大しています。

確立された振幅・偏光デバイスは、直接検出やセンシング用途で引き続き活用されます。アナログ変調器は、速度よりも直線性が重視されるニッチな無線光伝送(ROF)分野での地位を維持します。ウェーハレベルテストへの移行が平均販売価格(ASP)の低下を促し、フォトニック・エレクトロニクスの共同設計を習得した新規参入者を招き入れています。

優れた電気光学係数と温度安定性により、ニオブ酸リチウムは43.55%のシェアを維持しています。しかしながら、CMOSファブによる大量生産・低コスト化が実現したシリコンフォトニクスは、18.25%のCAGRで急成長中です。大規模クラウド購入者がエンドツーエンドの単一サプライヤー製フォトニックICを要求する中、シリコンフォトニクスに起因する光変調器市場規模は拡大しています。集積レーザーが必須の分野ではリン化インジウムが足場を維持し、電気光学ポリマーは100GHz超のマイクロ波フォトニクスに対応していますが、信頼性の課題は依然として残っています。

地域別分析

2025年時点でアジア太平洋地域は光変調器市場シェアの38.35%を占めました。これは中国の垂直統合型トランシーバーエコシステムと、インドにおける基地局の光ファイバー化推進が牽引しています。地域の製造基盤の厚みが部品コスト(BOM)を抑え、5GおよびFTTH(光ファイバー家庭接続)網への迅速な展開を可能にしています。政府の補助金プログラムと現地調達義務が生産基盤をさらに強化しています。北米では成熟した市場ながらイノベーション主導の需要が見られ、ハイパースケール事業者や防衛主要企業が最先端の薄膜LiNbO3およびシリコンフォトニクスを採用し、AIファブリックや量子研究を支えています。欧州ではメトロネットワークの着実なアップグレードが継続する一方、自動車用LiDARや産業用センシングがアナログ・偏光変調器の隣接市場を開拓しています。これらの成熟地域における光変調器市場規模は技術更新によって拡大し、新興経済圏の数量主導型拡大とは対照的です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 光ファイバー通信インフラへの投資増加

- ハイパースケールデータセンターの拡張と800G/1.6T光通信のロードマップ

- 新興国における5GおよびFTTHの展開加速

- メトロ/長距離リンクにおける400G以上のコヒーレント光通信への移行

- 絶縁体上ニオブ酸リチウム(LNOI)変調器の商用化

- 量子フォトニクスおよび極低温インターコネクトの需要

- 市場抑制要因

- 設計の複雑性と100Gbaudを超える熱管理の限界

- InP/LiNbO3ウェハーおよび分極プロセスの高い部品原価

- 高速フォトニクスパッケージングにおける熟練労働者不足

- 上流リチウム鉱石サプライチェーンの集中リスク

- 業界サプライチェーン分析

- 規制情勢

- マクロ経済要因の影響

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- 振幅変調器

- 偏波変調器

- 位相変調器

- アナログ変調器

- 統合型(SiPh/InP/LNOI)変調器チップ

- 素材プラットフォーム別

- ニオブ酸リチウム(LiNbO3)

- リン化インジウム(InP)

- シリコンフォトニクス(SiPh)

- 電気光学ポリマー

- その他

- データレートクラス別

- 25 Gbps以下

- 25~50 Gbps

- 50~100 Gbps

- 100 Gbps超

- 用途別

- 光通信

- データセンター相互接続

- 5Gフロントホール/バックホール

- 海底ケーブル

- 都市圏/長距離路線

- 光ファイバーセンサー

- 産業および構造上の健全性

- 石油・ガス監視

- 宇宙・防衛

- 試験・測定機器

- 量子コンピューティングと極低温技術に関するリンク集

- 光通信

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- 東南アジア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Lumentum Holdings Inc.

- Fujitsu Optical Components Ltd.

- Thorlabs Inc.

- Hamamatsu Photonics K.K.

- Lightwave Logic Inc.

- Gooch and Housego PLC

- APE Angewandte Physik and Elektronik GmbH

- AA Opto-Electronic SAS

- Conoptics Inc.

- L3Harris Technologies Inc.

- AMS Technologies AG

- Sumitomo Electric Device Innovations USA Inc.

- iXblue Photonics(Exail)

- Ciena Corporation

- Civicom Photonics

- HyperLight Corp.

- Keysight Technologies Inc.

- ThinkPhotonics Ltd.

- Optilab LLC

- Mellanox Technologies(NVIDIA Photonics)