|

市場調査レポート

商品コード

1851102

インドの金属加工:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)India Metal Fabrication - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの金属加工:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月25日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

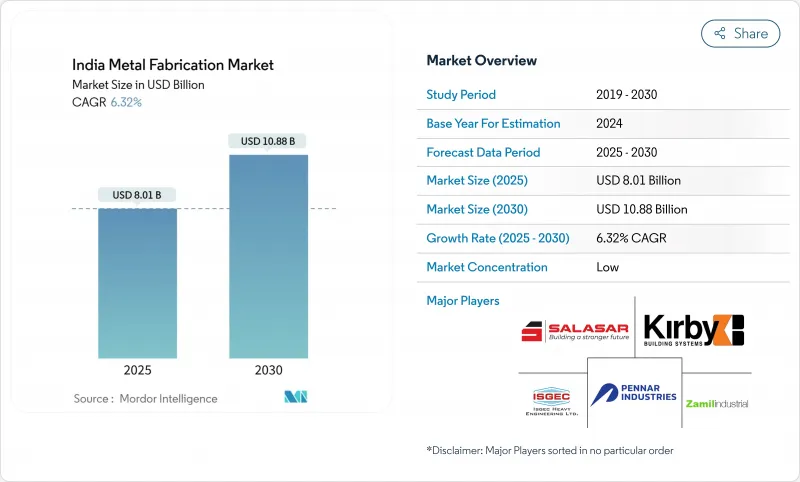

インドの金属加工市場規模は2025年に80億1,000万米ドル、2030年には108億8,000万米ドルに達し、CAGRは6.32%で推移すると予測されています。

Gati Shakti首相の下での大規模なインフラ整備、国防オフセットの増加、再生可能エネルギー設備のスケールアップが拡大を導きます。航空宇宙、データセンター、グリーン水素プロジェクトがより軽量で高精度のアセンブリーを要求しているため、機械加工は依然として支配的なサービスであるが、溶接とアルミニウム加工が急成長しています。南部の加工クラスターは防衛回廊とインダストリー4.0の採用から恩恵を受けるが、西部のハブは依然としてメガ鋼鉄とロジスティクス投資の大部分を引きつけています。インドの金属加工市場は、データセンターやプレハブ建築用のモジュラー・ソリューションを供給する一方で、変動しやすい原料炭コストをヘッジし、厳格化する環境基準を遵守できる総合プレーヤーに引き続き有利です。

インドの金属加工市場の動向と洞察

再生可能エネルギー機器製造需要の急増

国内の太陽電池モジュールの生産能力は2026年までに110GWに達し、精密加工を必要とする架台、トラッカー、インバーターハウジングの安定したパイプラインが確保されます。2024年の鉄鋼需要は、再生可能エネルギーの普及を背景に7.7%増加します。国家グリーン水素ミッションは、グリーン水素の統合に146億6,000万インドルピー(1億7,663万米ドル)を計上し、電解槽フレームと圧力容器の契約を開始しました。すでに部品の70~80%を現地調達している風力タービンメーカーは、米国への輸出用にタワーとナセルの加工を陸上で行っています。プロジェクト開発者が短いリードタイムと現地調達率を優先させるため、これらのプログラムを総合すると、インドの金属加工市場に数年分の数量を供給することになります。

政府の「ガティ・シャクティ」インフラ・パイプラインが鉄鋼加工を加速

マスタープランは200以上のプロジェクトを同期させ、橋のデッキ、駅の屋根、架線電化のガントリーなどの必要性を促進します。28,602カロールインドルピー(34億5,000万米ドル)の資金が投入された12の新産業ノードは、ロジスティクス・パークやユーティリティ・コリドー(公共事業用通路)にまたがる重・軽加工の付帯受注を約束しています。製鉄能力は2047年までに3倍の5億トンに増加する計画で、厚板の切断、圧延、断面溶接の需要が増加します。デリー・ムンバイ間産業大動脈の進展により、タタ・エレクトロニクスのようなアンカー・テナントがすでに確保され、川下の加工契約が拡大しています。

不安定な原料炭輸入コストが投入価格を押し上げる

原料炭の輸入量は25年度上半期に2,960万トンと6年ぶりのピークを記録し、工場が値引きを求めたため、ロシアのカーゴは前年同期比200%の急増となりました。オーストラリア産のシェアは2022年度の80%から54%に低下したが、それでも海底炭への依存度は総需要の85%を超えています。政府はボラティリティを抑えるためにコンソーシアム・スケールの買い付けとモンゴルの回廊を模索しているが、目先の板価格は影響を受けやすいままです。熱延コイル価格が高騰すると、加工業者の粗利率は80-120ベーシス・ポイント低下し、EPC顧客にコストを転嫁するか、小規模の受注を延期せざるを得なくなります。このように、インドの金属加工市場は一時的な圧力に直面しているが、最終的な国産コークスの開拓によって長期的な利益を得ています。

セグメント分析

2024年のインドの金属加工市場シェアは機械加工が33.4%を占め、航空宇宙、自動車、防衛関連の多軸CNC加工工場から供給されています。HurcoのChatCNCに代表されるAI対応CAMソフトウェアの採用は、プログラミング時間を短縮し、スピンドルの稼働率を向上させ、輸出の呼び戻しに迅速に対応できるようにします。自動化のアップグレードは、熟練労働者の不足を和らげ、高価値アセンブリのロットサイズワン生産を可能にします。

溶接は、高層インフラ、風力タワー、LNGモジュールなどで、非破壊検査済みの特殊な接合部が必要とされるため、規模は小さいもの、CAGRは最速の7.01%を記録しています。統合されたプレーヤーは、ロボットMIGラインとリアルタイムの溶接プール分析を組み込み、品質規定と圧縮されたプロジェクトスケジュールの両方を満たします。切断サービスでは、25 mmの炭素鋼を3 m/分でスライスするファイバーレーザーシステムが威力を発揮し、成形セルではサーボプレスブレーキを使用して高度な高強度鋼を曲げます。パンチング、スタンピング、仕上げの各工程では、環境基準を満たすため、インライン集塵機と水性塗料ブースにアップグレードしています。SAMARTH Udyog Bharat 4.0プログラムは、プネとベンガルールの体験センターを通じてこれらのアップグレードを支援し、インドの金属加工市場内の技術対応可能なワークショップに新規注文を誘導します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 再生可能エネルギー機器製造需要の急増

- 政府の「Gati Shakti」インフラパイプラインが鉄鋼加工を加速

- 国防オフセットと「メイク・イン・インディア」が精密加工を刺激

- 重い構造モジュールを必要とする急速なデータセンター建設

- ティア2・3都市におけるプレハブ建築の採用状況

- 市場抑制要因

- 変動する原料炭輸入コストが投入価格を押し上げる

- MSMEファブリケーターにとっての慢性的な電力供給のボトルネック

- 断片化したサプライチェーンが輸出グレードの品質保証を制限

- 環境対応(EPRとカーボン)コスト負担

- バリュー/サプライチェーン分析

- 政府規制と主な取り組み

- テクノロジーの展望

- 産業の魅力- ファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 最近の世界的な混乱がインドの金属加工市場に与える影響

第5章 市場規模と成長予測

- サービスタイプ別

- カッティング

- 成形/ベンディング

- 溶接

- 機械加工

- パンチング/スタンピング

- 仕上げ/表面治療

- その他(組立等)

- 材料別

- 炭素鋼

- ステンレス・合金鋼

- アルミニウム

- その他(銅、真鍮、特殊合金、板金(CRCA、GI、HR))

- エンドユーザー業界別

- 建設・インフラ

- 自動車・自動車部品

- 鉄道・地下鉄

- 電力・公益事業

- 航空宇宙・防衛

- 石油・ガス・製油所

- 海洋・造船

- 製造業(重機械・耐久消費財)

- その他(ジョブショップ、農機具、電気製品、耐久消費財など)

- 地域別

- 西インド(マハラシュトラ、グジャラート、ゴア)

- 南インド(タミル・ナードゥ、カルナータカ、テランガナ、アンドラ・プラデシュ、ケララ)

- 北インド(デリーNCR、ハリヤナ、パンジャブ、ウッタルプラデシュ、ウッタラーカンド、ヒマーチャル・プラデシュ、ラジャスタン)

- 東インド(西ベンガル、ジャールカンド、オディシャ、ビハール)

- 中央インド(マディヤ・プラデーシュ、チャッティースガル)

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Larsen & Toubro Ltd

- Kirby Building Systems India

- Zamil Industrial Investment Co.

- ISGEC Heavy Engineering Ltd

- Pennar Industries Ltd

- Salasar Techno Engineering Ltd

- JSW Severfield Structures Ltd

- Godrej Process Equipment

- Diamond Engineering(India)Pvt Ltd

- TEMA India Ltd

- Novatech Projects(India)Pvt Ltd

- Karamtara Engineering Pvt Ltd

- Bharat Heavy Electricals Ltd(Fabrication Div.)

- Tata Projects Ltd

- Welspun Corp Ltd

- Hindustan Dorr-Oliver Ltd

- Jindal Stainless-Fabrication Unit

- Bharat Forge Ltd(Fabrication Business)

- Essar Heavy Engineering Services

- Techno-Fab Engineering Ltd*