工作機械:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Machine Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1910603

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

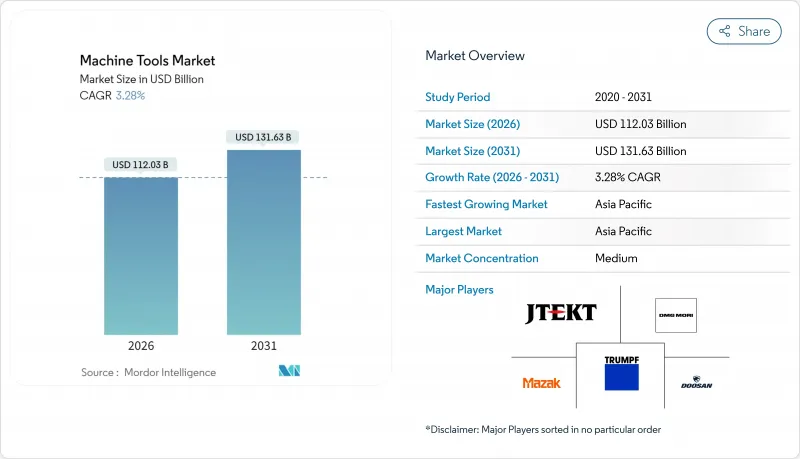

工作機械市場の規模は、2026年には1,120億3,000万米ドルと推定されており、2025年の1,084億7,000万米ドルから成長が見込まれます。

2031年の予測では1,316億3,000万米ドルに達し、2026年から2031年にかけてCAGR3.28%で成長すると見込まれています。

この拡大は、サプライチェーンの再編、貿易ルールの厳格化、半導体ファブへの記録的な投資という背景のもとで起こっており、いずれも超精密加工能力を必要としています。ASML社の高NA EUVシステム(1台あたり4億米ドル以上)は、次世代リソグラフィ技術がナノメートルレベルの金属切削・仕上げ性能の基準を引き上げている好例です。自動車の電動化と航空宇宙分野の近代化が進む中、多軸加工センターの需要が高まっており、インダストリー4.0プロジェクトでは、送り速度や工具経路を自己最適化するAI搭載CNC制御装置の採用が増加しています。地域別投資動向では、アジアが新規生産能力増強の大半を占めておりますが、米国におけるリショアリング優遇策や欧州の関税不透明感により、将来の需要はより分散化された工場配置へと移行しつつあります。直接販売が依然として世界の流通形態の大半を占めておりますが、電子商取引プラットフォームは中価格帯CNCモデルや交換用工具の調達サイクルを加速させております。

世界工作機械市場の動向と洞察

電動化急拡大が精密eパワートレイン加工を牽引

電気自動車用モーター工場では公差がマイクロレベルに要求され、自動化された固定子挿入・ヘアピン巻線工程と、二次仕上げ工程を不要とする5軸加工センターの組み合わせが一般的です。ZF社は2030年までにEV駆動系ラインの自動化率70%を目標としており、中国サプライヤーは2034年までに年間1億2,000万台超の電動モーター生産を見込んでいます。ゼネラルモーターズとメルセデス・ベンツはともに電動モーターハウジングの生産を内製化し、アルミシリコン合金を切削する際にパスオフチャタリングを発生させない機械を優先しています。ミクロンレベルの形状誤差から生じる電磁ノイズを抑制するため、工程内測定、切削油管理、閉ループ補償に対する需要が高まっています。

半導体ファブ拡張に伴う超精密装置の必要性

世界の300mmファブ投資額は2027年に1,370億米ドルに達すると予測され、南北アメリカでは3年間で支出が倍増する見込みです。ASMLの多トン級投影光学系には、1mの移動距離で50nm未満の形状誤差を維持するダイヤモンド旋削加工およびエアベアリング研削システムが求められます。TSMCの1,650億米ドル規模のアリゾナ複合施設は、国家レベルの半導体プログラムが、組み立て工程で重量部品を州内に留保できる超精密機械加工工場の地域需要を創出する好例です。クリーンルーム対応性、静圧スライドウェイ、無汚染潤滑方式は、このニッチ市場に参入する装置メーカーにとって現在では基本仕様となっています。

先進CNCシステムの高額設備投資と長期回収期間

アトランタ連銀の調査によれば、製造業者の80%が設備投資決定前に金利を重視しており、この傾向は2025年のプライムレート上昇によりさらに強まっています。最上位の5軸加工セルは設置費用が300万米ドルを超える場合があり、中量生産の受注生産工場では採算回収期間が5年を超えることもあります。設備のサービスとしての契約が暫定的な解決策として台頭していますが、ソフトウェアのアップグレードにより初期世代のコントローラーが陳腐化した際の残存価値リスクについて、多くのCFOが依然として警戒感を抱いています。

セグメント分析

多軸セグメントは2026年、工作機械市場規模の262億9,000万米ドルを占め、2031年までにCAGR6.88%で拡大が見込まれます。フライス盤は2025年時点で28.05%のシェアを維持する最大の収益源ですが、成長は現在、複雑なハウジングを1回のクランプで仕上げ加工する同時5軸プラットフォームに集中しています。自動車メーカーは内燃機関用シリンダーブロックラインを電動駆動用ケーシングセルに置き換える際、床面積とハンドリングコスト削減のため多軸加工機を採用しています。航空宇宙メーカーは高トルク傾斜スピンドル加工機を導入し、1.2m長で0.015mmの平面精度を維持しながらチタンスパーを加工しています。工具室オペレーターは依然として三軸膝型フライス盤に依存していますが、デジタル表示装置やプローブ機能を備えた改造キットにより、メンテナンス作業での競合を維持しています。

レーザー切断システムの需要は回復傾向にあります。AIガイド式パラメータウィザードが薄板ステンレスの廃棄率を低減しているためです。放電加工は、フライス盤では経済的に加工が困難な微小コーナー半径を必要とする金型キャビティ分野でニッチを維持しています。指向性エネルギー堆積と仕上げフライス加工を組み合わせたハイブリッド機は、サイクルタイム短縮が設備コストを上回るプロトタイプラボに導入されつつあります。プラズマ切断およびウォータージェット切断プラットフォームは重工業現場で活用されていますが、両技術とも歪んだ鋼板での切断品質維持のため、閉ループ式高さ制御の統合が始まっています。

CNCプラットフォームは2025年に売上高の68.55%を占め、CAGR6.08%で上昇し、工作機械市場の中心的な地位を確固たるものとしています。新興コントローラーはGPU加速アルゴリズムを採用し、STEPファイルを最適化された工具経路へ直接変換。これにより短納期部品のプログラミング時間を大幅に短縮します。中国のファーストオートメーション社はサーボドライブとPLCスタックの国産化に向け約1億元を調達。海外ファームウェア依存のリスク低減に向けた戦略的取り組みが顕著です。従来の手動式機械は小規模工場や職業訓練校で依然として使用されていますが、新規導入機は制御装置なしで購入される場合でも、将来の改造を見据えたサーボ対応フレームの動向が強まっています。ハイブリッド積層・切削複合システムは最先端技術として、レーザー金属積層と5軸加工を組み合わせ、航空宇宙用ブラケットにおけるサポート構造除去工程を省略します。

デジタルツイン技術により工具のたわみや熱膨張をシミュレート可能となり、試作段階での衝突を防止するオフマシン検証を実現しました。ChatCNC(TM)プラグインは直方体形状を自動認識し、荒加工から仕上げ加工までの工程を自動生成。経験の浅いプログラマーでも熟練者並みのサイクルタイムを達成できます。予知保全プラットフォームはスピンドルの異常を重大故障発生前に検知し、オペレーターの監視が最小限の無人運転環境において特に有用です。

本工作機械市場レポートは、製品別(金属切削工具、金属成形工具)、技術別(従来型機械、CNC機械など)、エンドユーザー産業別(自動車、航空宇宙・防衛など)、販売チャネル別(直販など)、地域別(北米、アジア太平洋、欧州など)に分類されています。本レポートでは、上記の全セグメントについて、市場規模および予測(金額ベース、米ドル)を提供しております。

地域別分析

戦略的転換の中でアジア太平洋地域が主導的立場を維持する一方、北米は国内回帰を進め、欧州は逆風の中でも革新を推進しています。アジア太平洋地域は2026年時点で世界収益の45.10%を占め、6.05%のCAGRが見込まれています。これは各国政府が電気自動車(EV)、航空宇宙、半導体産業クラスターへの優遇措置を集中的に実施しているためです。中国では、米国による中級機械への25%関税導入を相殺するため、小規模工場からハイエンドCNCセル工場への高度化が進められています。インドの生産連動型奨励プログラムは、300mmウェーハ工場や防衛用機体製造へ資本を誘導し、精密水平加工機および垂直加工センターの受注を創出しています。日本は数十年にわたるモーションコントロール技術を活用し、複数シフト稼働サイクルでサブミクロンの再現性を維持する超精密研削盤を輸出しております。一方、韓国の家電大手は折りたたみ式スマートフォンのヒンジプレートやカメラモジュール向け加工能力に投資を進めております。ベトナムやタイなどのASEAN諸国は、地理的リスク分散を重視する「中国プラスワン」調達モデルを採用するOEMメーカーからシェアを獲得しております。

北米では戦略的製造業の自立再建を目指すリショアリング政策の恩恵を受けています。米国では宇宙ロケット構造物用大型立形旋盤の生産能力増強に伴い、地域工具メーカーの受注が2001年以来最高の11.9%に達しました。メキシコの9.1%増はニアショア自動車組立が牽引し、ヌエボ・レオン州の政府支援工業団地では24時間許可承認を実現しています。カナダは鉱業部門や低炭素エネルギープロジェクトから工作機械受注を獲得していますが、熟練労働者不足により全体的な勢いは抑制されており、この制約は大陸全体に共通しています。

欧州では電力コスト上昇と通貨変動による利益率の圧迫に直面しているもの、高精度5軸加工機やレーザー金属積層システム分野では圧倒的な優位性を維持しています。ドイツのメーカーは国内受注の低迷に対応し、アフターサービス契約や改造事業(48時間保証付き主軸交換プログラムを含む)への注力を進めています。TRUMPF社は2025年に5億3,000万ユーロを研究開発に投資し、売上高が9%減少したにもかかわらずビームソース効率における優位性を維持しました。北欧企業は、新規機械出荷ごとにカーボンフットプリント証明書を提供することで持続可能性におけるリーダーシップを強調しており、この取り組みは公共部門の入札で義務化されるケースが増加しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電動化の流れが精密eパワートレイン加工を牽引

- インダストリー4.0の導入がスマートCNCプラットフォームの需要を促進

- 軽量合金・複合材料の普及には高速多軸加工工具が不可欠

- 半導体ファブ拡張に伴う超高精度装置の必要性

- 老朽化(20年以上)工作機械群の世界の更新サイクル

- 柔軟な加工による多品種少量生産の自動化

- 市場抑制要因

- 特殊鋼及び直動部品コストの急騰

- 高度なCNCシステムにおける高額な設備投資と長期的な回収期間

- 世界の熟練CNCプログラマー・オペレーターの不足

- 積層造形技術への資本転換

- バリュー/サプライチェーン分析

- 規制見通し(主要な政府規制と施策)

- 技術概要

- コネクテッド&自動化機械

- 高度制御/モーションシステム

- デジタル化とインダストリー4.0

- AIによる金属切削精度の向上

- 金属加工業界の概要

- 地政学が工作機械市場に与える影響

- 業界の魅力度- ファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額、単位:10億米ドル)

- 製品別

- 金属切削工具

- フライス盤

- 掘削機

- 旋盤

- 研削盤

- レーザー切断機

- 放電加工機(EDM)

- ウォータージェット切断機

- プラズマ切断機

- 多軸加工センター

- その他(ボーリングなど)

- 金属成形工具

- プレス機(機械式、油圧式、サーボ式)

- 鍛造機械

- 曲げ加工機

- その他(剪断、押出、圧延など)

- 金属切削工具

- 技術別

- 従来型機械(手動または半自動)

- CNC工作機械

- 積層造形/ハイブリッド機械

- エンドユーザー業界別

- 自動車

- 航空宇宙・防衛

- 電気・電子機器

- 産業機械・設備

- 医療機器

- 造船・海洋

- 精密工学

- エネルギー・電力

- 金属加工(請負工場など)

- その他の産業(鉄道、その他一般製造業など)

- 販売チャネル別

- 直接販売(OEMからエンドユーザーへ)

- 販売代理店・卸売業者

- オンライン/Eコマース

- その他(システムインテグレーター、イベント・展示会、リビルダー・再生品業者など)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- ペルー

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベネルクス(ベルギー、オランダ、ルクセンブルク)

- 北欧諸国(デンマーク、フィンランド、アイスランド、ノルウェー、スウェーデン)

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ASEAN(インドネシア、タイ、フィリピン、マレーシア、ベトナム)

- その他アジア太平洋地域

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- トルコ

- エジプト

- 南アフリカ

- ナイジェリア

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Yamazaki Mazak Corporation

- DMG MORI Co. Ltd

- TRUMPF Group

- JTEKT Corporation

- Doosan Machine Tools

- Okuma Corporation

- Makino Milling Machine Co. Ltd

- Haas Automation Inc.

- FANUC Corporation

- Hyundai Wia Corp.

- Schuler AG

- Sandvik AB(Seco & Walter)

- GF Machining Solutions

- Fives Group

- GROB-Werke GmbH & Co. KG

- Hermle AG

- EMAG GmbH & Co. KG

- Hardinge Inc.

- HURCO Companies Inc.

- Amada Co. Ltd

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日