|

市場調査レポート

商品コード

1687858

米国の不動産管理:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)US Property Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の不動産管理:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

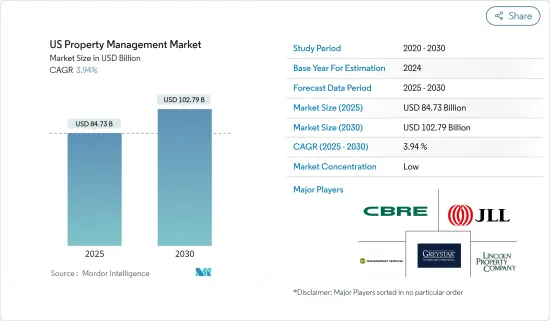

米国の不動産管理市場規模は2025年に847億3,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは3.94%で、2030年には1,027億9,000万米ドルに達すると予測されます。

米国は、新しいインフラや技術が頻繁に開発され、急速に進歩しており、この地域の全体的な経済統計も徐々に押し上げられています。多くの刺激的な製品の発売や、支援的な管理・統計技術によって、企業は圧倒的に成長しています。

不動産管理産業は、米国で最も急成長している産業のひとつです。米国内の主要都市で建設される新築アパートの増加に伴い、効果的な不動産管理ソリューションへのニーズが高まっています。

SaaSモデルは、刻々と変化する不動産環境の中で競合他社に先んじ、機敏に対応したいと考える不動産管理会社にとって、戦略的に必要なものとなりつつあります。さらに、職場の流動性の変化は、米国の不動産専門家にとって大きな成長機会となっています。米国には2023年時点で29万6,477の不動産管理事業者が存在し、2022年から2.1%増加しています。米国の不動産管理産業は労働集約型であり、資本よりも労働力への依存度が高いです。売上高に占める米国の不動産管理産業の事業コストの割合が最も高いのは、賃金(42.9%)、仕入(2.7%)、家賃・光熱費(2.7%)です。

米国不動産管理市場の動向

住宅部門の需要が市場を支える

景気の不透明感、インフレ、金利上昇にもかかわらず、ほとんどの州で住宅価格の上昇が続いています。最も住宅価格が上昇したのは、アリゾナ州、メイン州、コネチカット州、ニューハンプシャー州でした。2023年第2四半期には、カリフォルニア州、ワシントン州、コロラド州を含む8州とコロンビア特別区で価格が下落しました。

カリフォルニア州では、住宅価格の中央値が新築・中古住宅ともに平均販売価格を大きく上回りました。カリフォルニア州は米国で最も人気のある住宅市場のひとつです。

不動産管理ソフト会社RealPageは、2024年に完成するアパート戸数は67万1,953戸になり、1974年以来最多になると予測しています。

米国のアパート供給は2023年に爆発的に増加し、1987年以来の高水準に達し、43万9,000戸以上が新たに建設されました。この供給増は、賃借人の選択肢を増やし、賃料の伸びを大幅に鈍化させたため、多くの市場でアパート賃料が全面的に下落する結果となりました。

住宅セグメントの需要が高まるにつれ、不動産管理に対する需要も同時に高まりました。これらすべての業務を管理するには、多くの事務作業が伴う。そのため、不動産管理業者は、これらすべてのタスクを管理するためにソフトウェアを使用しています。

スマートホームの需要が市場を牽引

IoT技術やスマートデバイスの導入は、不動産ビジネスのさまざまな側面で普及が進むと予想されます。不動産ビジネスでは、顧客サービス性を向上させるためにIoTのニーズが継続的に高まっています。

ソフトウェアプロバイダーは、不動産とその管理者、所有者、投資家などの間のコミュニケーションを改善するために、ソフトウェアと技術を統合し始めています。例えば、テキサス州を拠点とする開発会社Capstone Partnersは、IoTソリューション・プロバイダーのIOTASと提携し、入居者向けに連動したスマートホーム環境を構築しました。その結果、スマートホームの普及が進むと、不動産管理ソフトウェアソリューションが促進される可能性が高いです。

すべての連携デバイス、プラットフォーム、民生用電子機器製品によって作成される膨大な量のデータは、ソフトウェア機能の改善に利用される可能性があります。さらに、データ分析により、IoTの採用は、不動産所有者が接続されたデバイスの性能を認識し、適切な行動を取ることを支援し、賃貸人により良いサービスを提供すると予測されます。ジョンソンコントロールズの建物効率パネル調査によると、回答者の70%が、動向を予測・診断するためにIoTを導入することで、ソフトウェアの需要が高まると感じています。

米国不動産管理産業概要

米国の不動産管理市場の大手企業は、収益管理、決済サービス、通信ソリューション、施設管理、賃貸管理などの知識を得て、ソフトウェアの能力と製品の適用性を高めることに注力しています。この手法は、米国における企業の足跡を増やすのに役立っています。

買収に伴い、パートナーシップと協力に大きな重点が置かれ、主要な利害関係者が新しい商品や経験を提供できるよう支援しています。さらに、既存の製品群の開発と成長は、サプライヤーが市場での地位を向上させるのに役立っています。同市場の主要企業としては、Greystar Real Estate Partners、JLL、Lincoln Property Company、CBREなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 商業セグメントの需要増加が市場を牽引

- 消費者の可処分所得の増加が市場を牽引

- 市場抑制要因

- 経済の不確実性が市場を抑制

- 市場機会

- アパートの急速な開発が市場を牽引

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- PESTLE分析

- COVID-19パンデミックの市場への影響

第5章 市場セグメンテーション

- エンドユーザー

- 商業

- 住宅

- サービス

- マーケティング

- 物件評価

- テナントサービス

- メンテナンス

- その他

第6章 競合情勢

- 市場集中度概要

- 企業プロファイル

- Greystar Real Estate Partners

- Lincoln Property Company

- CBRE Group

- Jones Lang LaSalle Incorporated

- CoStar Group Inc.

- Pinnacle Property Management

- Equity Residential

- FPI Management

- AvalonBay Communities

- WinnCompanies*

- その他の企業

第7章 市場の将来

第8章 付録

The US Property Management Market size is estimated at USD 84.73 billion in 2025, and is expected to reach USD 102.79 billion by 2030, at a CAGR of 3.94% during the forecast period (2025-2030).

The United States is rapidly progressing with newer infrastructures and technologies frequently developed, which also gradually boosts the overall economic statistics in this part of the world. Businesses are overwhelmingly growing with many stimulating product launches and supportive management and statistical techniques.

The property management industry is one of the fastest-growing industries in the United States. With the increasing number of new apartments being built in major cities across the United States, there is an increasing need for effective real estate management solutions.

SaaS models are becoming a strategic necessity for property management companies that want to stay ahead of the competition and stay agile in the ever-changing real estate environment. In addition, the changing landscape of workplace mobility presents a huge growth opportunity for real estate professionals in the United States. There were 296,477 property management businesses in the United States as of 2023, an increase of 2.1% from 2022. The US property management industry is labor intensive, which means businesses are more reliant on labor than capital. The highest costs for business in the US property management industry as a percentage of revenue are wages (42.9%), purchases (2.7%), and rent and utilities (2.7%).

US Property Management Market Trends

Demand from the Residential Sector is Supporting the Market

House prices continued to increase in most states despite economic uncertainty, inflation, and rising interest rates. The strongest home appreciation was in the state of Arizona, as well as in Maine, Connecticut, and New Hampshire. In Q2 of 2023, prices decreased in eight states and in the District of Columbia, including California, Washington, and Colorado.

In California, the median home value was significantly above the average sales price for both new and existing homes. California is one of the most sought-after housing markets in the United States.

Property management software company RealPage predicts that the number of apartment units completed in 2024 will be 671,953, which is the highest number since 1974.

The apartment supply in the United States exploded in 2023, reaching its highest level since 1987, with over 439,000 new units being built. This increase in supply has provided renters with more options and significantly slowed rent growth, resulting in outright apartment rent decreases in many markets.

As the demand in the residential segment increased, there was also a simultaneous demand for property management. Managing all these tasks comes with a lot of paperwork. That's the reason property managers are using software to manage all these tasks.

Demand for Smart Homes is Driving the Market

Implementing IoT technology and smart devices is expected to witness an increase in penetration in various aspects of the real estate business. The need for IoT is continuously increasing in the real estate business in order to improve customer serviceability.

Software providers have begun to integrate technology with software to improve communication between the property and its administrators, owners, investors, and others. For example, Capstone Partners, a Texas-based developer, teamed with IOTAS, an IoT solution provider, to create a linked smart home environment for tenants. As a result, the increasing penetration of smart homes is likely to drive property management software solutions.

The massive amount of data created by all linked devices, platforms, and appliances may be used to improve software functions. Furthermore, with data analysis, the adoption of IoT is projected to assist property owners in recognizing connected device performance and taking appropriate action to deliver better services to renters. According to Johnson Controls' building efficiency panel poll, 70% of respondents feel that introducing IoT to anticipate and diagnose trends will fuel demand for the software.

US Property Management Industry Overview

Leading players in the US property management market focus on obtaining knowledge in revenue management, payment services, communication solutions, facility management, and lease management to improve their software capabilities and product applicability. This technique assists organizations in increasing their corporate footprint in the United States.

Along with the acquisition, a significant emphasis on partnership and cooperation assists major stakeholders in providing new goods and experiences. Furthermore, the development and growth of the existing product range are assisting suppliers in improving their market position. Some of the major players in the market are Greystar Real Estate Partners, JLL, Lincoln Property Company, and CBRE.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand from the Commercial Segment is Driving the Market

- 4.2.2 Increasing Disposable Income of Consumers is Driving the market

- 4.3 Market Restraints

- 4.3.1 Economic Uncertainties are Restraining the Market

- 4.4 Market Opportunities

- 4.4.1 Rapid Development of Apartments is Driving the Market

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 PESTLE Analysis

- 4.8 Impact of the COVID-19 pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 End User

- 5.1.1 Commercial

- 5.1.2 Residential

- 5.2 Service

- 5.2.1 Marketing

- 5.2.2 Property Evaluation

- 5.2.3 Tenant Services

- 5.2.4 Maintenance

- 5.2.5 Other Services

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Greystar Real Estate Partners

- 6.2.2 Lincoln Property Company

- 6.2.3 CBRE Group

- 6.2.4 Jones Lang LaSalle Incorporated

- 6.2.5 CoStar Group Inc.

- 6.2.6 Pinnacle Property Management

- 6.2.7 Equity Residential

- 6.2.8 FPI Management

- 6.2.9 AvalonBay Communities

- 6.2.10 WinnCompanies*

- 6.3 Other Companies