ペット向け獣医食:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Pet Veterinary Diet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 374 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687808

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

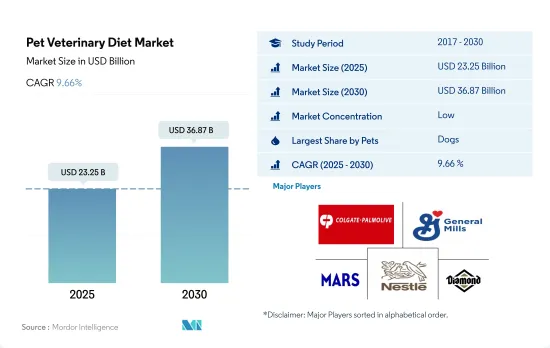

ペット向け獣医食の市場規模は2025年に232億5,000万米ドルと予測され、2030年には368億7,000万米ドルに達し、予測期間(2025-2030年)のCAGRは9.66%で成長すると予測されています。

犬は様々な病気にかかりやすくなっているため、世界のペット向け獣医食市場を独占

- 世界経済の急速な成長に伴い、ペットの飼育率は着実に上昇しています。ペットに対する考え方も、特に新興諸国では年々進化しています。その結果、世界の獣医食市場は2022年に176億4,000万米ドルに達し、2017年から2022年の間に74.4%増加しました。この成長の原動力は、ペットの人間化の動向の高まりです。

- 犬セグメントは世界の獣医食市場で主要シェアを占め、2022年には91億1,000万米ドルに達しました。この優位性は、犬の飼育数が多いことと、生活習慣や遺伝的要因で様々な病気にかかりやすくなっていることに起因しています。さらに、犬の体格が大きいため、犬特有の栄養ニーズを満たすための獣医食の需要が高まっています。

- 猫のセグメントは、世界のペット向け獣医食市場で最も急速に成長しているセグメントの1つとして浮上しており、予測期間中のCAGRは8.8%と予測されています。これは、他のペットに比べてメンテナンスの必要性が低く、費用対効果が高いため、ペットとしての猫の人気が高まり、猫の飼育数が大幅に増加しているためです。

- 他のペットもまた、様々な潜在的な健康問題を予防するために、獣医学的な食事療法をかなり必要としています。しかし、その他のペットの飼育頭数は、法律や環境の制約から少ないです。その結果、その他のペットの獣医食市場は2022年に27億6,000万米ドルの規模に達しました。

- ペットの飼い主の意識の高まりとペット数増加が、予測期間中の世界のペット向け獣医食市場を牽引すると予測されます。

ペットの人間化の進展とペットの健康に対する飼い主の関心の高まりがペット向け獣医食市場を牽引している

- 世界の獣医食市場では、北米が最大の市場シェアを占め、2022年には市場の47.9%を占める。同地域では米国が最大の市場であり、同年の市場規模は75億4,000万米ドルでした。米国の市場シェアが大きいのは、ペット専用食の普及と、ペットを家族の一員とみなし、専門的なケアを受ける「ペットの人間化」の動向が拡大しているためと考えられます。

- 欧州は世界のペット向け獣医食市場で2番目のシェアを持ち、2022年の市場規模は46億4,000万米ドルです。この地域の成長は、ペットの健康と福祉に対する飼い主の意識の高まりが大きな原動力となっています。獣医食は、この地域全体で重要性を増しています。欧州のペット向け獣医食市場は、2017年の2億9,050万人から2022年には3億2,440万人に達する同地域のペット数の増加により、2017年から2021年の間に44.6%増加しました。

- アジア太平洋は市場の17.6%を占め、2022年には31億米ドルとなりました。アジア太平洋地域のペット数は、同期間の世界のペット数の32.8%であるため、大きなシェアを占めています。アジア太平洋では、ペットの飼い主の間でペットの健康上の懸念やペットの人間化傾向に対する意識が高まっていることから、同地域のペット向け獣医食市場は2017年から2021年の間に40%増加しました。

- 南米はペット向け獣医食市場の急成長地域で、予測期間中にCAGR 14.2%を記録すると予測されています。これは、ペットのヒューマニゼーション(人間化)が進み、飼い主がペットの健康を重視するようになったためです。

- 世界のペット数の増加とペットの人間化は、予測期間中に市場を牽引すると予想される要因です。

世界のペット向け獣医食市場の動向

猫は、コンパニオンとしての採用が増加し、猫を飼うことの利点についての認識が高まっているため、世界的に2番目に採用数の多いペットです。

- 世界的に、犬の飼育に比べ猫の飼育は少ないです。2022年、猫の飼育数は世界のペット数の24.8%を占め、2017年から2022年の間に19.2%増加しました。欧州では、猫は幸運や幸運の象徴と考えられているため、猫のシェアは高くなると思われます。これは歴史的な時代からそうであり、特にロシアはペットとしての猫の飼育数が多い主要国でした。世界的に猫の飼育数が多くなったのは、ペットの人間化が進んだからです。猫は犬に比べ居住スペースが少なくて済み、世話をする人間がいない間、家の中で一匹で長く留まることができます。例えば、2017年から2022年にかけて、ロシアと米国では、猫の親を含むペットの親の70%以上が、猫を家族、友人、または子供とみなしています。

- さらに、パンデミックの間、人々は屋内で過ごさなければならず、猫は屋内に閉じこもることなく過ごすことができ、犬に比べ物静かな動物であるため、猫の養子縁組が大幅に増加しました。米国では、パンデミックの間、在宅勤務の文化がペットとしての猫の飼育を増加させ、交友関係の需要につながり、ペットを飼う人の多くがミレニアル世代でした。例えば2022年には、米国ではミレニアル世代がペットを飼う人の33%を占めるようになりました。パンデミック時の猫の採用率の上昇は、ペットフード市場の成長に長期にわたって好影響を与えると予想されます。猫の養子縁組や購入の増加、ペットの人間化の増加といった要因は、ペットの猫の飼育数の増加を助け、予測期間中のペットフード市場の成長にさらに役立つと予想されます。

北米と欧州ではペット向け獣医食への支出が増加しており、ペットの健康と福祉に対する関心の高まりがペットの支出を促進しています。

- 世界的に、ペットの支出は増加しており、2017年から2022年の間に25.4%増加しています。これは、プレミアム化の上昇とペットの健康に対する懸念の高まりによるものです。ペット支出に占める犬の割合は高く、2022年には39.7%に達します。猫よりもペットフードの消費量が多く、プレミアムペットフードを与えることが増えているため、シェアが高くなっています。

- ペットの親はペットの健康に気を配っているため、ペットフードに投資する割合が最も高いです。ペットのグルーミング、ペットのデイケア、他のペットとのより良い社会化のためのペットの散歩などの他のサービスを提供することが増加しています。この動向は北米、欧州、アジア太平洋などの地域で見られます。例えば、米国では2022年にペットフードがペット費用の21%を占めました。さらに、人々はペットに高品質のフードを摂取させたいと考え、プレミアム価格を支払うことを厭わないため、プレミアムペットフードを購入しています。米国では、2022年にペットの親の約40%がプレミアム・ペットフードを購入し、香港のキャットフード市場では、2022年にプレミアム・ペットフード部門がペットフード売上の75%を占める。

- 特にCOVID-19パンデミックの後、ウェブサイト上で多くのペット用品が入手できるようになったため、動物用食餌をオフラインの店舗からオンラインストアで購入するように変化しているが、オランダのように、ペット保護者がペットショップが提供する商品の品質により、ペットショップからの購入を好む国もあります。例えば米国では、獣医食を含むペットケアのオンライン販売は、2020年の32%から2022年には40%に増加しました。プレミアム化とペットの健康に対する関心の高まりが、2023年から2029年にかけてのペット支出の増加に寄与すると予想される要因です。

ペット向け獣医食の業界概要

ペット向け獣医食市場は細分化されており、上位5社で34.77%を占めています。この市場の主要企業は以下の通りです。 Colgate-Palmolive Company(Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle(Purina)and Schell & Kampeter Inc.(Diamond Pet Foods)(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他のペット

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ製品

- 糖尿病

- 消化器過敏症

- 口腔ケア食

- 腎臓

- 尿路疾患

- その他の獣医食

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンライン・チャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 地域

- アフリカ

- 国別

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- フィリピン

- 台湾

- タイ

- ベトナム

- その他アジア太平洋地域

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ロシア

- スペイン

- 英国

- その他欧州

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他北米地域

- 南米

- 国別

- アルゼンチン

- ブラジル

- その他南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Affinity Petcare SA

- Alltech

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- Heristo aktiengesellschaft

- Mars Incorporated

- Nestle(Purina)

- PLB International

- Schell & Kampeter Inc.(Diamond Pet Foods)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Pet Veterinary Diet Market size is estimated at 23.25 billion USD in 2025, and is expected to reach 36.87 billion USD by 2030, growing at a CAGR of 9.66% during the forecast period (2025-2030).

Dogs dominated the global pet veterinary diets market due to their increasing susceptibility to various diseases

- Global pet ownership rates are steadily rising as the global economy is rapidly growing, driven by increasing urbanization and industrial rates. The attitude toward pets has been evolving, particularly in developing countries over the years. As a result, the global veterinary diet market reached USD 17.64 billion in 2022, which increased by 74.4% between 2017 and 2022. This growth is driven by the growing trend of pet humanization.

- The dog segment held a major share of the global pet veterinary diet market, with a value of USD 9.11 billion in 2022. This dominance is attributed to the presence of a large population of dogs and their increased susceptibility to various diseases due to their lifestyle and genetics. Furthermore, the larger size of dogs necessitates a higher demand for veterinary diets to meet their specific nutritional needs.

- The cats segment is emerging as one of the fastest-growing segments in the global pet veterinary diet market, with a projected CAGR of 8.8% during the forecast period. This is owing to the significant increase in the cat population as a result of the growing popularity of cats as pets due to their low maintenance requirements and cost-effectiveness compared to other pets.

- Other pets also have significant requirements for veterinary diets to prevent various potential health problems. However, the population of other pets is low due to legal and environmental restrictions. As a result, the other pets' veterinary diet market reached a value of USD 2.76 billion in 2022.

- The increasing awareness among pet owners and the growing population of pets are estimated to drive the global pet veterinary diet market during the forecast period.

Growing pet humanization and increasing focus of pet owners on their pet health are driving the pet veterinary diets market

- In the global veterinary diets market, North America held the largest market share, accounting for 47.9% of the market in 2022. In the region, the United States is the largest market, valued at USD 7.54 billion in the same year. The large market share of the United States can be attributed to the prevalent usage of specialized pet diets and the growing trend of pet humanization, where pets are regarded as family members and receive specialized care.

- Europe has the second-largest share of the global pet veterinary diets market, with a value of USD 4.64 billion in 2022. The region's growth is highly driven by increasing awareness of pet owners on their pet health and well-being. Veterinary diets have gained significant importance across the region. Europe's pet veterinary diets market increased by 44.6% between 2017 and 2021, owing to the rising pet population in the region, which reached 324.4 million in 2022, increasing from 290.5 million in 2017.

- Asia-Pacific accounted for 17.6% of the market, valued at USD 3.10 billion in 2022. Asia-Pacific had a major share due to its pet population being 32.8% of the global pet population in the same period. The growing awareness about pet health concerns and pet humanization trend among pet owners in Asia-Pacific increased the pet veterinary diets market in the region by 40% between 2017 and 2021.

- South America is the fastest-growing region for the pet veterinary diets market, which is anticipated to record a CAGR of 14.2% during the forecast period. This can be attributed to the growing pet owner's focus on their pet health driven by the increasing pet humanization.

- The growing pet population and pet humanization globally are the factors anticipated to drive the market during the forecast period.

Global Pet Veterinary Diet Market Trends

Cats are the second-largest adopted pets globally due to their growing adoption as companions and increasing awareness about the benefits of owning a cat

- Globally, cats are being less adopted compared to the adoption of dogs. In 2022, the cat population accounted for 24.8% of the global pet population, witnessing an increase in the population by 19.2% between 2017 and 2022. The share of cats will be higher in Europe as they consider them to be a symbol of luck or fortune. This has been true since historical times, particularly in Russia, which has been a major country with a high population of cats as pets. The high growth of the cat population globally was because of the rise in pet humanization. Cats require less space to live compared to dogs and can stay alone in a home for a longer time while no human is available to take care of the cat. For instance, between 2017 and 2022, more than 70% of pet parents, including cat parents, in Russia and the United States considered cats as family members, friends, or children.

- Moreover, there was a significant increase in cat adoption during the pandemic as people had to stay indoors, and cats can stay indoors without being cooped up and are silent animals compared to dogs. The United States witnessed higher adoption of cats as pets during the pandemic because of the work-from-home culture, leading to a demand for companionship and a higher number of pet owners being millennials. For instance, in 2022, millennials were 33% of pet parents in the United States. The higher adoption of cats during the pandemic is expected to have a positive impact for a longer period on the pet food market's growth. Factors such as an increase in the adoption and purchase of cats and an increase in pet humanization are expected to help the growth of the pet cat population, and it further helps in the growth of the pet food market during the forecast period.

North America and Europe are increasingly spending on pet veterinary diets, with rising concerns over pet's health and well-being driving pet expenditure

- Globally, pet expenditures are increasing, having risen by 25.4% between 2017 and 2022 because of the rise in premiumization and growing pet health concerns. Dogs have a higher share of pet expenditure, which amounted to 39.7% in 2022. They have a higher share due to the higher consumption of pet food than cats and are increasingly being fed with premium pet food.

- Pet parents invest the highest share of the pet expenditure on pet food as they are concerned about their pets' well-being. There has been a rise in providing other services such as pet grooming, pet daycare, and pet walking for better socialization with other pets. This trend has been witnessed in regions such as North America, Europe, and Asia-Pacific. For instance, pet food accounted for 21% of pet expenses in the United States in 2022. Moreover, people are purchasing premium pet food as they want their pets to consume high-quality food and are willing to pay premium prices. In the United States, about 40% of pet parents purchased premium pet food in 2022, and in Hong Kong's cat food market, the premium pet food segment accounted for 75% of pet food sales in 2022.

- There has been a change in purchasing veterinary diets from offline stores to online stores, especially after the COVID-19 pandemic, because of the large number of pet products available on websites, but there are countries such as the Netherlands where pet parents prefer purchasing from pet stores due to the quality of the products offered by them. For instance, in the United States, online sales of pet care, including veterinary diets, increased from 32% in 2020 to 40% in 2022. Premiumization and growing concerns over their pet's health are the factors expected to contribute to the increase in pet expenditure during 2023-2029.

Pet Veterinary Diet Industry Overview

The Pet Veterinary Diet Market is fragmented, with the top five companies occupying 34.77%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and Schell & Kampeter Inc. (Diamond Pet Foods) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Product

- 5.1.1 Diabetes

- 5.1.2 Digestive Sensitivity

- 5.1.3 Oral Care Diets

- 5.1.4 Renal

- 5.1.5 Urinary tract disease

- 5.1.6 Other Veterinary Diets

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Region

- 5.4.1 Africa

- 5.4.1.1 By Country

- 5.4.1.1.1 South Africa

- 5.4.1.1.2 Rest of Africa

- 5.4.2 Asia-Pacific

- 5.4.2.1 By Country

- 5.4.2.1.1 Australia

- 5.4.2.1.2 China

- 5.4.2.1.3 India

- 5.4.2.1.4 Indonesia

- 5.4.2.1.5 Japan

- 5.4.2.1.6 Malaysia

- 5.4.2.1.7 Philippines

- 5.4.2.1.8 Taiwan

- 5.4.2.1.9 Thailand

- 5.4.2.1.10 Vietnam

- 5.4.2.1.11 Rest of Asia-Pacific

- 5.4.3 Europe

- 5.4.3.1 By Country

- 5.4.3.1.1 France

- 5.4.3.1.2 Germany

- 5.4.3.1.3 Italy

- 5.4.3.1.4 Netherlands

- 5.4.3.1.5 Poland

- 5.4.3.1.6 Russia

- 5.4.3.1.7 Spain

- 5.4.3.1.8 United Kingdom

- 5.4.3.1.9 Rest of Europe

- 5.4.4 North America

- 5.4.4.1 By Country

- 5.4.4.1.1 Canada

- 5.4.4.1.2 Mexico

- 5.4.4.1.3 United States

- 5.4.4.1.4 Rest of North America

- 5.4.5 South America

- 5.4.5.1 By Country

- 5.4.5.1.1 Argentina

- 5.4.5.1.2 Brazil

- 5.4.5.1.3 Rest of South America

- 5.4.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Affinity Petcare SA

- 6.4.2 Alltech

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 General Mills Inc.

- 6.4.6 Heristo aktiengesellschaft

- 6.4.7 Mars Incorporated

- 6.4.8 Nestle (Purina)

- 6.4.9 PLB International

- 6.4.10 Schell & Kampeter Inc. (Diamond Pet Foods)

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 374 Pages

- 納期

- 2~3営業日