欧州のオンライン保険:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Online Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687793

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

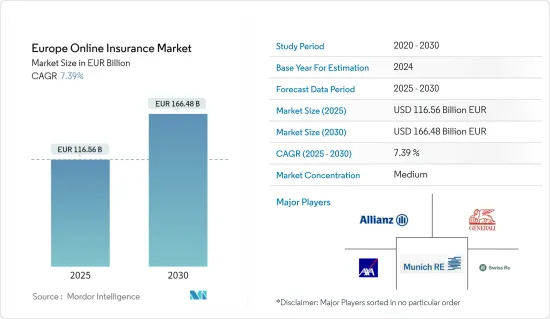

欧州のオンライン保険市場規模は2025年に1,165億6,000万ユーロと推定され、予測期間(2025年~2030年)のCAGRは7.39%で、2030年には1,664億8,000万ユーロに達すると予測されます。

ビジネス環境が急速に変化する中、保険会社にとって保険販売チャネルの開拓はますます重要になっています。近年、大半の世界企業にとってデジタルへの移行は自然な流れであったが、保険セクターにとっては簡単なことではありません。

保険は常に、顧客をよく知るブローカーや代理店によって販売されてきました。特に生命保険や医療保険に関しては、信頼関係が不可欠です。保険料の面では、生命保険プランの99%以上が対面販売または仲介業者を通じて販売されています。ウェブ・アグリゲーターを含む他の方法で販売されるのは最後の1%だけです。

ブルガリアではオンライン販売は禁止されており、チェコ共和国ではCOVID-19によりすでに部分的に施行されています。デンマークでは80%から90%以上がオンライン販売です。エストニアではオンライン販売が増加しています。インターネット販売のみを行っている企業もあります。フランスでは、ネット販売は独立した流通チャネルとは見なされておらず、他のチャネルと一緒になっています。クロアチアでは、オンライン販売は全体の1%程度です。イタリアではオンライン販売が可能で、自動車のインターネット販売は7%です。ノルウェーでは損害保険商品のオンライン販売が非常に普及しています。トルコのオンライン販売はGWPの2.5%に過ぎないです。

消費者や保険会社の間で価格比較サイトの人気が高まるにつれ、価格比較サイト会社は市場での存在感や商品提供の充実を図るため、提携や買収活動に余念がないです。

欧州のオンライン保険市場動向

COVID-19はデジタル保険を加速させた

COVID-19危機の間、保険分野では、顧客とその仲介業者との間の伝統的な対面対話の一部にチャットやビデオ会議が取って代わりました。また、個人的な接触が重要であることに変わりはないです。

ベルギーの証券会社のうち、ソフトウェアやインシュアテック・アプリケーションを活用して効率的に業務を行っているのは22%に過ぎないが、比較サイトの増加により、ブローカーは顧客のニーズによりマッチした提案を開発できるようになっています。

証券会社のペーパーレス化はますます進んでおり、その3分の2はすでにこの目標を達成したと主張しています。

インシュアテックの資金調達数の増加

2021年、欧州のインシュアテックの資金調達額は過去最高を記録し、92件の取引を通じて約25億ユーロが投資されました。

エコシステムは成熟しつつあり、平均取引規模は2020年の800万ユーロから2021年には2,800万ユーロに急増しています。そのほとんどが上半期に開示された:英国のZegoとBoughtByMany、ドイツのWefox、フランスのAlanとShift Technologyです。2021年下半期に発表されたのは1社のみである:英国のEnvelopRiskです。

欧州のオンライン保険業界の概要

本レポートでは、欧州のオンライン保険市場で事業を展開する主要な国際企業を取り上げています。市場シェアの面では、伝統的な大手企業は現在、市場競争上の優位性を獲得するためにテクノロジー企業と提携しています。しかし、中堅・中小のインシュアテック企業との厳しい競合に直面しています。インシュアテック企業は、ニーズに合ったソリューションを提供することで、調査対象市場を破壊することに注力しています。主な企業には、アリアンツ・セ、アッシクラツィオーニ・ジェネラリ、アクサ・サ、ミュンヘン再保険などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

- 調査の成果

- 調査の前提

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 市場機会

- 産業バリューチェーン分析

- 市場の最新技術革新と最新動向に関する洞察

- 業界の政府規制に関する洞察

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 保険タイプ別

- 生命保険

- 損害保険

- 地域別

- ドイツ

- フランス

- 英国

- イタリア

- その他の欧州

第6章 競合情勢

- Market Concentration

- 企業プロファイル

- Allianz SE

- Assicurazioni Generali SpA

- AXA SA

- Munich RE

- Swiss Re AG

- Aviva

- Zurich Insurance*

第7章 市場機会と今後の動向

第8章 免責事項と出版社について

目次

The Europe Online Insurance Market size is estimated at EUR 116.56 billion in 2025, and is expected to reach EUR 166.48 billion by 2030, at a CAGR of 7.39% during the forecast period (2025-2030).

In a business environment that is changing quickly, exploring insurance distribution channels has become more and more important for insurance firms. While the transition to digital has been a natural process for the majority of global companies in recent years, it has not been simple for the insurance sector.

Insurance has always been sold by brokers and agents who know their clients well. It is a trusting relationship, particularly when it comes to life and health insurance. In terms of premiums, more than 99% of life insurance plans are sold in person or through intermediaries. Only the final 1% is sold via other methods, including web aggregators.

Online sales are barely getting started; online sales are prohibited in Bulgaria and are already being partially enforced in the Czech Republic due to COVID-19. Over 80% to 90% of Denmark's sales are made online. Online sales are rising in Estonia. Some businesses only conduct internet sales. Online sales are not seen as a separate channel of distribution in France; they are included with other channels. In Croatia, around 1% of all sales are made online in total.Online sales are possible in Italy and internet sales for cars were 7%. Online sales of non-life products are very widespread in Norway. Online sales in Turkey only account for 2.5% of GWP.

With the growing popularity of price comparison websites among consumers and insurance companies, price comparison website companies are indulging in partnerships and acquisition activities to enrich their market presence and product offerings.

Europe Online Insurance Market Trends

Covid-19 accelerated the Digital insurance

During the COVID-19 crisis, In Insurance sector, chat and videoconference replaced some of the traditional face-to-face interactions between clients and their intermediaries. And, while personal contact remains important.

While only 22% of Belgian brokerage offices is leveraging software or InsurTech applications to work more efficiently, a growing number of comparison websites is helping brokers develop an offering that better matches client needs.

Brokerage firms are becoming increasingly paperless, with two-thirds of them claiming to have already reached this goal.

Rising Numbers of Insurtech Funding

In 2021, European insurtech funding reached an all-time high, with around EUR 2.5 billion invested through 92 deals.

The ecosystem is maturing so that the average deal size jumped from ~EUR 8 million in 2020 to EUR 28 million in 2021 That's also related to mega-rounds (tickets over EUR 100 million) announced across Europe. Most of them were disclosed in the first half of the year: Zego and BoughtByMany in the UK, Wefox in Germany, and Alan and Shift Technology in France. Only one happened in H2 2021: EnvelopRisk in the UK.

Europe Online Insurance Industry Overview

The report covers the major international players operating in the European online insurance market. In terms of market share, the major traditional players are currently partnering with technological companies to gain competitive advantage in the market studied. However, they face stiff competition from mid-size and smaller insurtech companies, which focus on disrupting the market studied by offering tailored solutions. Some of the major Companies includes Allianz Se, Assicurazioni Generali, Axa Sa, Munich Re among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Defination

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Study Deliverables

- 2.2 Study Assumptions

- 2.3 Analysis Methodology

- 2.4 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Market Opportunities

- 4.5 Industry Value Chain Analysis

- 4.6 Insights into Latest Technological Innovations and Recent Trends in the Market

- 4.7 Insights on Government Regulations in the Industry

- 4.8 Porters Five Force Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Insurance Type

- 5.1.1 Life Insurance

- 5.1.2 Non-life Insurance

- 5.2 By Geography

- 5.2.1 Germany

- 5.2.2 France

- 5.2.3 United Kingdom

- 5.2.4 Italy

- 5.2.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Company Profiles

- 6.2.1 Allianz SE

- 6.2.2 Assicurazioni Generali SpA

- 6.2.3 AXA SA

- 6.2.4 Munich RE

- 6.2.5 Swiss Re AG

- 6.2.6 Aviva

- 6.2.7 Zurich Insurance*

7 MARKET OPPORTUNTIES AND FUTURE TRENDS

8 DISCLAIMER AND ABOUT US

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日