|

市場調査レポート

商品コード

1850995

米国の健康および医療保険:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)United States Health And Medical Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の健康および医療保険:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 152 Pages

納期: 2~3営業日

|

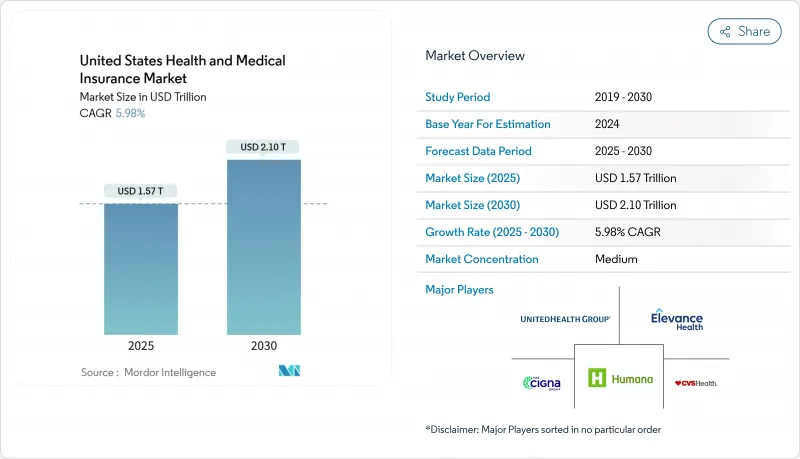

概要

米国の健康および医療保険市場は2025年に1兆5,700億米ドルに達し、2030年には2兆1,000億米ドルに拡大すると予測されています。

高齢化の進展、慢性疾患罹患率の上昇、ACA補助金の充実、メディケア・アドバンテージ加入の活発化などが、保険加入者の拡大と保険料の伸びを後押ししています。雇用者のプランの弾力性、高免責オプションの急速な普及、デジタル販売もプラス基調に寄与しており、バリュー・ベース・ケアやAI主導のアンダーライティングに対するキャリアの投資は、商品の差別化とコスト管理を向上させています。保険会社の統合は、メディケア・セグメントにおける最近の資産買収に見られるように、医療損害率のプレッシャーを回避し、全国的な事業展開を可能にするために、各社が規模を追求する中で続いています。地域的な公募パイロットや再保険制度は保険料をさらに安定させ、特に欧米では競争を刺激しています。

米国の健康および医療保険市場動向と洞察

ヘルスケアコストの上昇と高齢化

保険料の伸びは、医療費の上昇と高齢者の利用率の上昇と密接に関連しており、大口団体医療損害率は2023年に低下する前に90%を超えるまで上昇しています。メディケア・アドバンテージの2024年の新規加入者数は5.4%増となったが、専門薬剤費の増加や慢性疾患の罹患率がマージンを圧迫し、保険会社はリスク管理の強化やバリュー・ベースの取り決めへと舵を切りました。雇用主の調査によると、76%の企業が専門薬剤のコストを懸念しており、サイト・オブ・ケア・ステアリングやバイオシミラー導入への関心を高めています。したがって、人口動態の勢いは、対応可能なプールを拡大すると同時に、アナリティクス、ケアコーディネーション、ベネフィットの再設計を通じて動向を抑制するキャリアへの課題となっています。

ACA補助金とマーケットプレース加入の拡大

インフレ抑制法(Inflation Reduction Act)の補助金拡大により、2025年には2,400万人の保険加入が見込まれ、平均世帯貯蓄額は年間800米ドルとなり、ACA加入者数は過去最高となりました。2024年後半にはDACA受給者が加わり、リスクプールはさらに拡大した。また、州ベースのマーケットプレースでは、追加的なインセンティブが付与され、保険加入が深まり、保険料が手頃になりました。補助金は2025年まで続くが、更新をめぐる政治的な不透明感から長期的な価格設定が難しくなり、一部の保険会社は地理的な拡大を控えています。それでも、加入者数の安定は予測可能な保険金請求実績を下支えし、加入コストを下げるデジタル・アウトリーチを後押ししています。

ACA補助金延長をめぐる規制の不確実性

2025年に保険料控除が期限切れとなるため、価格設定が曖昧になり、一部の保険会社は2026年の料率を保守的に設定したり、新規参入を制限したりする可能性があります。保険料高騰の可能性は、雇用者給付のない中所得世帯の加入を阻害し、リスク・プールを不安定化させ、逆選択を増幅させる可能性があります。州単位のマーケットプレースには補助金があり、参加保険会社は加入者と収入源をより予測しやすくなるため、ボラティリティは緩和されます。しかし、連邦政府からの補助金だけに頼っている州では、追加的な支援がないため、保険料が急激に上昇する可能性があります。このような格差は、地域間の保険料格差を拡大し、連邦政府主導の保険取引所にさらなる負担を強いる可能性があります。

セグメント分析

雇用者拠出型保険は2024年時点で米国の健康および医療保険市場の47.5%を占め、保険料の伸びを安定させる大きなリスクプールを確保しています。しかし、メディケア・アドバンテージは、団塊世代の高齢化と保険料ゼロのプラン・マーケティングに後押しされ、CAGR 7.80%と他のすべての保険種目を上回っています。ACAによる補助金付き保険も、保険料控除の強化が続く中で拡大し、メディケイドのマネージドケアは予算の見通しを追い求める各州で上昇を続けています。軍や連邦政府の従業員向け保険制度は引き続き堅調だが、伸びは鈍いです。

一方、メディケア・アドバンテージ保険会社は、歯科、視力、OTC手当を追加し、総合的な給付を求める高齢者にアピールしています。ICHRAは、一部の労働者を個人保険に移行させるかもしれないが、税制上の優遇措置や管理の手間が省けることから、依然として団体保険が主流です。メディケア・アドバンテージの参加者は、規制による支払い調整とスターレーティングのしきい値によって運営上の逆風を受け、利幅を維持するためのケア調整への投資を迫られています。

プリファード・プロバイダー・オーガニゼーション(PPO)契約は、2024年の保険料の46%を維持し、より消費者主導の形態にシェアが流出しつつあるにもかかわらず、米国の健康および医療保険市場で最大のスライスを確保しています。PPOの耐久性は、幅広いネットワークへのアクセスとわかりやすいネットワーク外オプションに対する加入者の要望を反映しており、統一された給付設計を必要とする複数の州にまたがる雇用主によって評価されています。保険会社は、遠隔医療を優先したプライマリ・ケア・モデル、バリュー・ベースの病院への誘導インセンティブ、治療前にエピソード・レベルのコストを表示するAI対応の価格透明性ツールによってPPOの提供を刷新しており、PPOは支出規律に欠けるという批判を鈍らせるのに役立っています。チャットボット、プロバイダー品質スコア、控除額トラッカーからなるデジタル・ナビゲーション・レイヤーは、現在、ほとんどの大グループPPO契約に付随しており、会員のエンゲージメントを向上させ、不必要な専門医の受診を抑制しています。

高免責医療保険制度(HDHP)は、保険数理上の価値を縮小させることなく保険料の支出を抑えるために、雇用主が播種した医療貯蓄口座と組み合わせることで、CAGR最速の9.45%を記録しています。しかし、予防医療の遅れや従業員の離職率の上昇に気づいた一部の企業が方針を転換したため、HDHPに加入する労働者の割合は2023年には41.7%に低下します。この勢いを維持するため、保険会社は、連邦政府のHSAコンプライアンスを維持しながら、バーチャル緊急ケア、糖尿病治療用品、メンタルヘルス・コーチングに無控除保障を組み込んでいます。健康維持機構(Health Maintenance Organization)と専属プロバイダー機構(Exclusive Provider Organization)の商品は、コストに敏感な中小企業や、統合された医療提供システムがシームレスなケア経路を提供する地域で、ニッチな関連性を維持しています。セグメンテーションを総合すると、従来のプランの原型を全面的に放棄するのではなく、手頃な価格、明確な価格、ネットワークの効率性へと積極的に再調整していることがわかる。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ヘルスケア費の高騰と人口の高齢化

- ACA補助金とマーケットプレースプレイス登録の拡大

- 各州におけるメディケイド・マネージドケア導入の増加

- 雇用主のICHRAとQSEHRAが個人市場への適用範囲を移行

- AIによるリスク層別化でマイクロ保険の提供が可能に

- 遠隔医療の恒久的な償還均等化によりバーチャルケアの適用範囲が拡大

- 市場抑制要因

- ACA補助金延長をめぐる規制の不確実性

- 医療損失率の上昇が保険会社の利益を圧迫

- 州レベルの公的オプション制度が価格競合を激化

- サイバーセキュリティとデータプライバシーのコンプライアンスコストの高騰

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 補償タイプ別

- 雇用主支援

- 個人(ACA/非団体)

- メディケイドマネージドケア

- メディケアアドバンテージ

- 軍隊/政府(TRICARE、VA、FEHBP)

- プランタイプ別

- HMO

- PPO

- EPO

- POS

- HDHP/消費者主導

- 保険タイプ別

- 主要医学(総合)

- メディケアサプリメント

- 歯科

- 入院給付金/限定給付

- ビジョン

- 短期医療

- その他の付帯保険(事故、重篤な病気)

- 流通チャネル別

- 消費者向け

- ブローカーとエージェント

- 雇用者福利厚生コンサルタント

- オンラインマーケットプレイス/取引所

- 地域別

- 北東部

- 中西部

- 南部

- 西部

第6章 競合情勢

- 市場集中分析

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- UnitedHealth Group

- CVS Health(Aetna)

- Elevance Health(Blue Cross Blue Shield)

- Cigna Group

- Humana

- Centene

- Kaiser Permanente

- Health Care Service Corp(HCSC)

- Molina Healthcare

- GuideWell(Florida Blue)

- Independence Health Group

- Highmark Health

- Blue Cross Blue Shield of Alabama

- Blue Cross Blue Shield of Michigan

- Blue Cross Blue Shield of North Carolina

- Medica

- Oscar Health

- Bright Health

- Clover Health

- Triple-S Management