北米のHVAC機器:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

North America HVAC Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687783

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

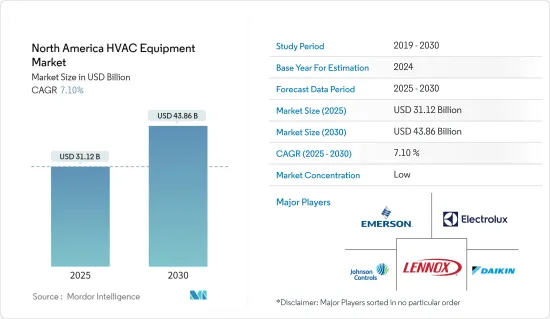

北米のHVAC機器の市場規模は2025年に311億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは7.1%で、2030年には438億6,000万米ドルに達すると予測されます。

可処分所得の増加、建設活動の急速な拡大、気象パターンの変化が、調査対象市場の成長を牽引しています。北米では、スマートホームやスマートシティプログラムの導入が大幅に増加しており、市場の成長を牽引しています。

主なハイライト

- 持続可能な地域社会の発展を目的とした予算配分の増加という形で、政府支援の高まりが商業・工業建設部門の継続的な成長に寄与している可能性があります。また、建設活動の増加、急速な都市化、インフラ改革は、HVACユニットの交換の急増をもたらし、HVAC機器市場を牽引しています。

- 北米のHVAC機器市場の成長は、スマートシステムに対する需要の増加と、モノのインターネット(IoT)、産業オートメーションシステム、スマート製造、インダストリー4.0の統合によってもたらされます。市場の平均を上回る成長の大部分は、グリーンビルディングの建設活動の活発化から予測されます。急速に拡大しているスマートホーム市場は、HVACシステム市場の成長を後押しすると予測されます。

- グリーンビルディング建設プロジェクトは、同地域のHVAC機器市場の拡大をさらに後押しします。例えば、2022年2月、カナダ・グリーンビルディング協議会(CAGBC)は、世界中で使用されているグリーンビルディング認証プログラムであるLEED(Leadership in Energy and Environmental Design)の年間トップ10国・地域リストで、2021年に同国が世界第2位にランクされたと発表しました。居住者の健康とエネルギー消費に対する意識の高まりから、政府機関が課す基準を満たす空調機器の設置は、グリーンビルディング設計における重要な基準となりつつあります。

- しかし、IEAと米国エネルギー省によれば、電力消費の約25~35%はHVACシステムによるものです。同出典によると、このエネルギー消費の大部分(20%~60%)は、寄生的エネルギー使用(冷暖房の移送に使用されるファンやポンプの動力源として使用されるエネルギー)が寄与しています。従って、集中型空調システムは、ユニット型システムよりも(空調される空間の単位面積当たりのエネルギー消費量という点では)効率的であるにもかかわらず、エネルギー代が負担となっています。

- 製造業全体の雇用が不足しています。悲しいことに、冷暖房空調業界も例外ではないです。現在の労働力不足がこれらに起因するものであるかどうかは別として、市場の成長を妨げる要因になりかねないです。

北米のHVAC機器市場動向

ヒートポンプが大きく成長

- ヒートポンプが占める市場シェアは大きいと予測されます。気候条件、機器による利便性、政府による税額控除、規制など様々な要因により、ヒートポンプの使用は北米地域で着実に増加しています。

- エネルギー効率の高い製品を採用する方向へのパラダイムシフトと消費支出の増加により、米国の住宅用ヒートポンプ市場は今後も堅調に拡大すると思われます。事業環境は、脱炭素経済への進行によって刺激され、これは法制化されたエネルギー政策とインセンティブによって支えられると思われます。老朽化した建物の改修が進むにつれ、柔軟性と快適性の向上に対する需要が高まると思われます。これにより、業界はよりダイナミックになると思われます。

- ヒートポンプは、水熱源、空気熱源、地中熱源などのタイプに分類されます。空気熱源ヒートポンプ(ASHP)は、電気を取り込み、周囲の空気から熱を取り出し、摂氏90度までの温水を生成します。周囲の空気から熱を取り出すため、空気は冷たくなります。このように、温水と冷気の両方に対する要求が、空気熱源ヒートポンプの成長を促進しています。

- さらに、北米の多くの地域で寒冷地用ヒートポンプの人気が高まっており、これがこの分野における大きな技術革新の原動力となっています。寒冷地用ヒートポンプは、摂氏マイナス25度までの条件下で効率的に作動するように開発されており、摂氏マイナス18度でも200%以上の効率を維持するシステムもあります。

- 2022年6月、米国(DOE)は、レノックス・インターナショナルが米国エネルギー省(DOE)の住宅用寒冷地ヒートポンプ技術の最初のパートナーとなったと発表しました。

米国が大きな市場シェアを占める

- 米国は不可欠な機器市場のひとつであり、安定した成長率を示しています。建設活動の活発化、高効率システムの入手可能性、極端な気候条件が、施設全体へのシステム設置に有利となっています。さらに、キャリア、エマソン・エレクトリック社などの大手メーカーの存在が、今後の北米市場の成長を補完しています。

- さらに、モノのインターネット(IoT)の統合に伴い、複数のメーカーがスマート暖房・空調・換気システムの提供を開始し、米国全体の市場成長を後押ししています。

- 持続可能な未来を確保するため、米国エネルギー省(DOE)は国全体のエネルギー効率基準の改善に多額の投資を行っています。DOEは、環境、エネルギー、原子力の問題に対する科学技術による解決策を見出すことで、アメリカの安全と繁栄を確かなものにしたいと考えています。

- さらに、エネルギー情報局(EIA)の住宅エネルギー消費調査(RECS)によると、主に居住している米国の住宅7,600万戸(全体の64%)がセントラル空調機器を使用していると推定されています。約1,300万世帯(11%)が冷暖房にヒートポンプを使用しています。2023年までに、米国で販売されるすべての新しい住宅用エアコンと空気熱源ヒートポンプシステムは、最新のエネルギー効率基準を満たす必要があり、HVAC機器の成長に拍車をかけています。

- さらに、米国国勢調査局によると、2022年6月の米国の新築住宅建設件数は約136万件でした。2022年6月の米国における個人所有の新築住宅戸数は約155万戸でした。これはさらに、予測期間中に同国でヒートポンプの大きな新規需要を生み出すと予想されます。

北米のHVAC機器産業の概要

北米のHVAC機器市場の競争企業間の敵対関係は高く、ダイキン、キャリア、レノックスのような著名ベンダーが各分野で主要な市場シェアを占め、確立された流通網を利用しています。HVAC機器産業は最大級の市場であるため、市場シェアに妥協することなく、このように多数の主要ベンダーが存在することは持続可能です。しかし、各ベンダーは、特に冷暖房分野で、より大きなシェアを獲得するために熾烈な競争を繰り広げています。

- 2023年2月- レノックスは、EnlightとXion製品ラインの導入により、パッケージ型屋上ユニットの包括的な品揃えを強化しました。同社のEnlight製品ファミリーは、環境への影響を最小限に抑え、効率を最大化することを目的としています。

- 2022年10月-Carrier Corporationは、北米でAquaEdge19DV水冷ターボ冷凍機の容量拡大を宣言。AquaEdge19DVは、商業用高層ビルや複合用途ビル、大規模製造施設や医療機関など、より大きな容量の需要に応えるため、最大1,150トンまで供給可能です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の想定と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- マクロ経済動向の市場への影響評価

第5章 市場力学

- 市場促進要因

- 住宅・非住宅ユーザーの増加

- 市場抑制要因

- HVAC機器の高いエネルギー消費量

第6章 市場セグメンテーション

- 機器別

- 空調機器

- 暖房機器

- ヒートポンプ

- 除湿機・加湿器

- エンドユーザー別

- 住宅

- 産業

- 商業

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Johnson Controls International PLC

- Daikin Industries Ltd

- Lennox International Inc.

- Electrolux AB

- Emerson Electric Co.

- Carrier Corporation

- Rheem Manufacturing Company Inc.

- Uponor Corp.

- Ingersoll Rand Inc.(Trane Inc.)

- Nortek Global HVAC, LLC

第8章 投資分析

第9章 市場の将来

目次

The North America HVAC Equipment Market size is estimated at USD 31.12 billion in 2025, and is expected to reach USD 43.86 billion by 2030, at a CAGR of 7.1% during the forecast period (2025-2030).

Increasing disposable income, rapidly expanding construction activity, and changing weather patterns are driving the growth of the market studied. North America is witnessing a significant increase in the implementation of smart home and smart city programs, driving the market's growth.

Key Highlights

- Growing government support, in the form of higher budget allocations designed to increase sustainable community development, may contribute to the continually growing commercial and industrial construction sectors. Besides, increased construction activities, rapid urbanization, and infrastructural reforms result in an upsurge in HVAC unit replacements, thus driving the HVAC equipment market.

- The growth of the North American HVAC equipment market is driven by an increase in demand for smart systems and the integration of the Internet of Things (IoT), industrial automation systems, smart manufacturing, and industry 4.0. A significant portion of the market's above-average growth is anticipated from the uptick in green building construction activities. The smart home market, which is expanding rapidly, is projected to boost the HVAC system market's growth.

- Green building construction projects further support the empowerment of the HVAC equipment market in the region. For instance, in February 2022, Canada Green Building Council (CAGBC) announced that the country ranked second globally on the annual list of Top 10 Countries and Regions for LEED (Leadership in Energy and Environmental Design), a green building certification program used worldwide, in 2021. Installation of HVAC equipment with standards imposed by the governmental bodies for the rising awareness of occupants' health and energy consumption is becoming a vital criteria in green building designs.

- However, as per IEA and the U.S. Department of Energy, around 25-35% of electricity consumption is due to HVAC systems. According to the same source, a large part (20% - 60%) of this energy consumption is contributed by parasitic energy use (energy used to power fans and pumps used for the transfer of heating and cooling). Thus, centralized HVAC systems have burdened energy bills despite being more efficient (in terms of energy units' consumption per unit area of space conditioned) than unitary systems.

- There is a lack of employment in the whole manufacturing sector. Sadly, there is no exception in the heating and air conditioning industry Whether or not current workforce shortages are caused by these, they will likely be exacerbated might hamper the market gorwth

North America HVAC Equipment Market Trends

Heat Pumps to Witness Significant Growth

- The market share that heat pumps are predicted to command is significant. Due to various factors, including climatic conditions, the convenience provided by the equipment, government tax credit benefits, regulations, etc., the use of heat pumps has steadily increased in the North American region.

- Owing to a paradigm shift toward adopting energy-efficient products and rising consumer spending, the residential heat pump market in the United States would continue to expand steadily. The business environment will be stimulated by the ongoing progress toward a decarbonized economy, which will be supported by legislative energy policies and incentives. As the number of old buildings that are being fixed up goes up, there will be more demand for flexibility and better comfort. This will make the industry more dynamic.

- The heat pumps are been categorized based on types, such as water source, air source, and ground source. The air-source heat pump (ASHP) takes in electricity, extracts heat from the surrounding air, and produces hot water up to 90 degrees Celsius. Due to the extraction of heat from the ambient air, it gets cooler. Thus, the requirement for both hot water and cold air is driving the growth of air-source heat pumps.

- Moreover, Cold climate heat pumps are becoming increasingly popular in many regions across North America, and this has been driving significant innovation in the space. Cold climate heat pumps are developed to work efficiently in conditions down to -25 degrees Celsius, with some systems maintaining an efficiency of over 200% at -18 degrees Celsius.

- In June 2022, the U.S (DOE) announced that Lennox International had became the first partner in the U.S. Department of Energy's (DOE's) Residential Cold Climate Heat Pump Technology has Challenge to develop an next-generation electric heat pump which woyuld that can more effectively heat homes in northern climates relative to current models.

United States Holds Major Market Share

- The United States is one of the essential equipment markets, witnessing a steady growth rate. The growing construction activity, availability of high-efficiency systems, and extreme climatic conditions favour system installation across the facilities. Additionally, the presence of leading manufacturers, such as Carriers, Emerson Electric Co., and others, is complementing the growth of the North American market in the future.

- Additionally, with the Internet of Things (IoT) integration, several manufacturers have initiated smart heating, air conditioning, and ventilation system offers that, in turn, are propelling market growth across the United States.

- To ensure a sustainable future, the U.S. Department of Energy (DOE) is heavily investing in improving energy efficiency standards throughout the country. The DOE wants to make sure that America is safe and doing well by finding science and technology solutions to its environmental, energy, and nuclear problems.

- Moreover, the Energy Information Administration's (EIA) Residential Energy Consumption Survey (RECS) estimates that 76 million primarily occupied US homes (64% of the total) use central air-conditioning equipment. About 13 million households (11%) use heat pumps for heating or cooling. By 2023, all new residential air-conditioning and air-source heat pump systems sold in the United States will require meeting the latest energy efficiency standards, fueling the growth of HVAC equipment.

- Furthermore, according to the US Census Bureau, new home construction in the United States in June 2022 was around 1.36 million. There were approximately 1.55 million new privately owned housing units in the United States in June 2022. This is further expected to create significant new demand for heat pumps in the country over the forecast period.

North America HVAC Equipment Industry Overview

The competitive rivalry in the North American HVAC equipment market is high, as the market studied is home to prominent vendors like Daikin, Carrier, and Lennox that command a major market share in different segments and have access to well-established distribution networks. Owing to the HVAC equipment industry being one of the largest markets, the existence of such a high number of major vendors without compromising on their market shares is sustainable. However, each vendor, especially in the heating and cooling segments, is fiercely competing to gain a larger share of the market studied.

- February 2023 - Lennox enhanced its comprehensive selection of With the introduction of the Enlight and Xion product lines, packaged rooftop units have been introduced. The company's Enlight product family aims to minimize environmental impact and maximize efficiency.

- October 2022 - Carrier Corporation declared that it had increased In North America, the AquaEdge 19DV watercooled Centrifugal chiller offers a range of capacities. The AquaEdge19DV is capable of supplying the customer with up to 1150 tonnes in order to meet their demand for larger capacities, as regards Commercial Highrise and mixed Use Building Applications, Large Manufacturing Establishments or Health Institutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defnition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of Impact of Macro Economic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Residential and Non-residential Users

- 5.2 Market Restraints

- 5.2.1 High Energy Consumption of HVAC Equipment

6 MARKET SEGMENTATION

- 6.1 By Equipment

- 6.1.1 Air Conditioning Equipment

- 6.1.2 Heating Equipment

- 6.1.3 Heat Pumps

- 6.1.4 Dehumidifiers and Humidifiers

- 6.2 By End User

- 6.2.1 Residential

- 6.2.2 Industrial

- 6.2.3 Commercial

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Johnson Controls International PLC

- 7.1.2 Daikin Industries Ltd

- 7.1.3 Lennox International Inc.

- 7.1.4 Electrolux AB

- 7.1.5 Emerson Electric Co.

- 7.1.6 Carrier Corporation

- 7.1.7 Rheem Manufacturing Company Inc.

- 7.1.8 Uponor Corp.

- 7.1.9 Ingersoll Rand Inc. (Trane Inc.)

- 7.1.10 Nortek Global HVAC, LLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日