|

市場調査レポート

商品コード

1910530

塩酸:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Hydrochloric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 塩酸:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

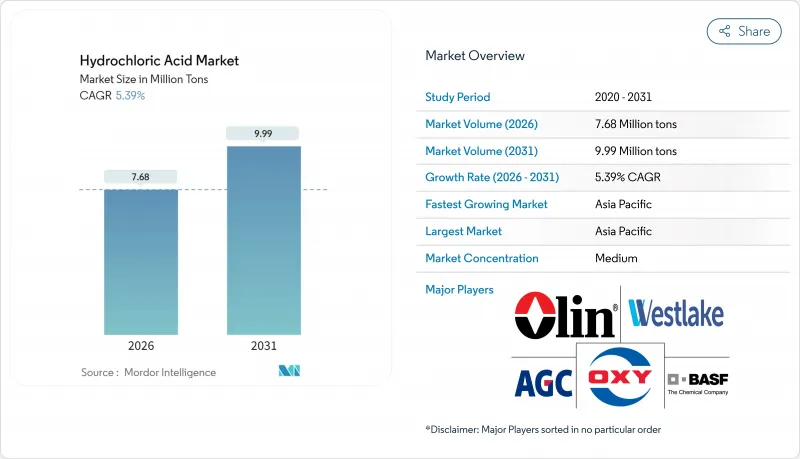

塩酸市場の規模は2026年に768万トンと推定され、2025年の729万トンから成長が見込まれます。

2031年の予測値は999万トンで、2026年から2031年にかけてCAGR5.39%で拡大する見通しです。

石油・ガス井の刺激処理、半導体製造、水処理、そして無数の中間体合成における本化合物の有用性は、世界の需要に堅調な下支えをもたらしています。供給の回復力は、塩酸が担う二重の役割に由来します。すなわち、専用プラントにおける主要製品であると同時に、塩素アルカリ電解装置の製品別でもあるため、生産者は苛性ソーダと塩素のサイクル変動に柔軟に対応できるのです。メキシコ湾岸地域の操業停止やアジアの半導体拡張によりスポット需要が吸収される際には短期的な逼迫が生じますが、統合生産者は規模の経済性、原料の安定供給、分散型物流ネットワークを背景に、長期契約市場での優位性を維持しております。

世界の塩酸市場の動向と展望

石油・ガス井刺激需要の急増

非在来型石油・ガス貯留層の開発により、塩酸市場はフラクチャリングおよびマトリックス酸処理プログラムに確固たる基盤を築いています。オペレーターは炭酸塩の溶解、閉塞した穿孔孔の再開放、坑井寿命の延長を目的として15~28%の酸濃度を使用しています。パーミアン盆地およびオマーンでのフィールド試験では、未処理のオフセット坑井と比較して18%高い流量が確認されています。乳化酸および遅延酸の化学技術により、高温・深部地層での作業が可能となり、従来は課題とされていた貯留層への需要が拡大しています。統合サービス企業は現在、腐食防止剤、鉄分制御剤、界面活性剤をパッケージ化しており、これらは井戸コスト項目を増加させますが、マトリックス浸透効率を向上させ、間接的に井戸当たりの塩酸消費量を押し上げます。シェール生産者が自然減衰曲線を相殺するための増産技術を導入する中、新規完成井戸数は減少しているにもかかわらず、ベースライン購入量は増加しており、少なくとも2029年までは数量成長が持続すると見込まれます。

水処理および食品加工における衛生ニーズ

地方自治体や食品加工業者は、pH調整や二酸化塩素生成のために塩酸の採用を継続しております。これは、通常の投与量では塩酸が塩素酸塩や臭素酸塩の副生成物を残さないためです。オーストラリアの飲料水ガイドラインでは凝集・軟化処理への塩酸使用が規定されており、世界の規制上の受容を反映しています。食肉加工・乳製品ラインでは、電解水システムが塩と希塩酸を組み合わせ、現場で次亜塩素酸を生成します。これにより60秒未満で5ログの細菌減少を実現し、残留塩化物濃度を1ppm未満に抑えるため、クリーンラベルの要求を満たします。小規模加工業者では、スキッドマウント型電解装置を採用し、必要に応じて10~15%の塩酸を生成することで、包装酸の輸送コスト(最大150米ドル/トン)を削減しています。

労働者の安全と環境毒性に関する規制

米国労働安全衛生局(OSHA)が15分間における許容暴露限界を2ppmに厳格化したことで、製鉄所や食品工場では局所排気換気設備や耐酸性床材の更新が求められ、1拠点あたり20万~50万米ドルのコンプライアンス関連設備投資が増加しています。欧州化学物質庁の候補リスト選定プロセスにより、塩化物含有量の多い廃棄物流が精査の対象となり、生産者は製造工程全体にわたる責任ある管理を実証するか、認可取得の障壁に直面することになります。ドイツやイタリアの小規模な亜鉛めっき業者は、老朽化した自社タンクを改修する代わりに、酸洗い工程を第三者の委託業者に外注するようになり、直接的な酸の購入量を削減しています。

セグメント分析

工業用グレード製品は、鋼材酸洗、アルミナ分解、バルク有機合成における主力試薬として、2025年出荷量の52.90%を占めました。このセグメントは、高純度下流製品の景気循環的な軟化から塩酸市場を保護しました。2024年の半導体調整期においても、建設用鋼材の受注が工業用グレードの出荷量をプラスに維持したのです。33~35%濃度のグレードは、特に内陸油田において、酸性度単位あたりの輸送コストが調達先を決定するニッチ市場で需要を維持しております。超高純度品は供給量のわずか4.14%ながら、商品グレードの12倍を超えるプレミアム価格により、総価値の18%を占めています。アジアのファブ拡張を基盤に、超高純度塩酸市場規模はCAGR5.71%で推移し、2031年には389千トンに達する見込みです。

表向きの数字の裏では、グレードの階層構造は流動的です。欧州3拠点における省エネ型膜式セルへの改修により変動費を28%削減し、新規設備投資なしで工業用グレードから電子グレードへの戦略的ボトルネック解消を実現しました。デノラのバイポーラプレート電極は、35%塩酸1トン当たりの比消費電力を2,000kWhに低減し、余剰工業用ストリームのグレードアップ余地を開拓しました。統合製油所では真空蒸留精製塔も導入され、従来は中和廃棄酸として扱われていたものから価値を回収しています。

塩酸市場レポートは、グレード別(工業用、濃縮、超高純度)、エンドユーザー産業別(化学、石油・ガス、鉄鋼・冶金、食品・飲料、繊維・皮革、その他エンドユーザー産業)、地域別(アジア太平洋、北米、欧州、南米、中東・アフリカ)に分類されています。市場予測は数量(トン)単位で提供されます。

地域別分析

アジア太平洋地域の主導的地位は、長江デルタおよび珠江デルタに広がる統合塩素アルカリ網に起因します。この地域では、自社消費用の塩酸が塩化ビニル、ポリカーボネート、エピクロロヒドリンの製造ラインに供給されています。中国の二重置換プログラムにより水銀電解槽は廃止されましたが、同時に年間300万トン超の塩酸製品別を生み出す膜分離プロジェクトが承認され、地域の自給体制が確立されました。インドのアトゥル社による投資により、100トン/日の市販塩酸が追加され、西インド地域の高運賃な湾岸輸入への依存度が低下しました。韓国と台湾では、半導体生産指数に連動した長期契約により高純度塩酸を調達しており、バルク化学品では珍しいヘッジ構造となっています。

北米では増産技術による石油回収キャンペーンが安定したフラクチャリング酸需要を生み、着実な成長を続けています。ハリケーン・アイダは脆弱性を露呈させました。3度にわたる上陸により米国湾岸地域の塩素アルカリ名目生産能力の80%以上が停止し、スポット価格指数は2週間足らずで40%急騰しました。対応策として地域分散が進んでいます。クロラム・ソリューションズ社はアリゾナ州カサグランデに7,000万米ドルの膜プラントを建設し、西部石油化学・鉱業クラスターへ供給を開始しました。エネルギーコストに制約される欧州では、PFAS樹脂再生や医薬品中間体など高付加価値用途への転換が進んでいます。アントワープ・ロッテルダム経由の輸入量は2025年に12%増加し、ドイツの電解装置が稼働を抑制した時期にはカナダ産が季節的な供給不足を補いました。東欧の鋼材亜鉛めっき業者は依然として汎用品グレードを調達していますが、塩化物排出規制の強化に対応するため、ゼロ排水式酸洗設備への投資を進めています。南米および中東・アフリカ地域は、鉱業、オイルサンド、海水淡水化プロジェクトの増加に伴い、生産量は小規模ながら成長傾向にあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 石油・ガス井刺激需要の急増

- 水処理および食品加工における衛生ニーズ

- 先端プロセス向け半導体グレード塩酸(エッチング用)

- PFAS除去樹脂の再生要件

- リチウムイオン電池リサイクル浸出化学

- 市場抑制要因

- 労働者の安全および環境毒性に関する規制

- 塩素アルカリ製品別の価格変動性

- 酸洗浴における有機酸の代替

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- グレード別

- 産業

- 集中型

- 超高純度

- エンドユーザー業界別

- 化学

- 石油・ガス

- 鉄鋼・冶金

- 食品・飲料

- 繊維・皮革

- その他のエンドユーザー産業

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- 北欧諸国

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- AGC Inc.

- BASF SE

- Coogee

- Covestro AG

- Detrex Corporation

- DONGYUE GROUP

- ERCO Worldwide

- Ercros S.A

- INEOS Group

- Jones-Hamilton Co.

- Merck KGaA

- Occidental Petroleum Corporation(OxyChem)

- Olin Corporation

- TOAGOSEI CO.,LTD.

- Vynova Group

- Westlake Corporation