|

|

市場調査レポート

商品コード

1851734

カメラモジュール:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Camera Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| カメラモジュール:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月14日

発行: Mordor Intelligence

ページ情報: 英文 194 Pages

納期: 2~3営業日

|

概要

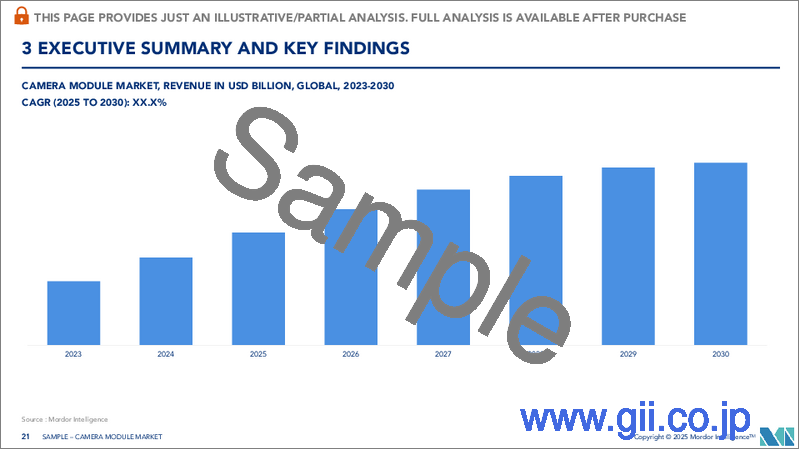

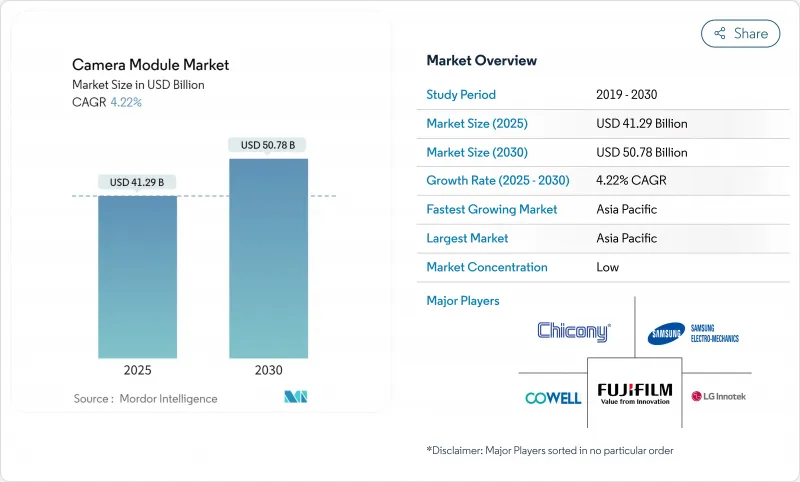

カメラモジュール市場の2025年の市場規模は412億9,000万米ドルで、2030年には507億8,000万米ドルに達すると予測され、この期間のCAGRは4.22%です。

携帯電話端末の飽和により、メーカーはマルチカメラアレイ、折りたたみ光学ズーム、オンデバイスAI処理へと舵を切っており、成長は純粋な数量拡大から豊富な機能を備えたイノベーションへとシフトしています。自動車の安全義務化、エッジ分析による監視、新興のXRデバイスは、従来のモバイル出荷以外にも収益源を広げています。2024年の台湾地震でボイスコイルモーター(VCM)調達の脆弱性が露呈した後、部品メーカーはサプライチェーンの回復力を優先しており、インドなどの政府は生産に連動したインセンティブを利用して組み立てを現地化し、新たな投資を誘致しています。韓国、日本、中国のサプライヤーは、ディスプレイ下カメラや潜望鏡モジュールなどの高価値ニッチ分野での知的財産ポジションを確保しようと競争力を高めています。

世界のカメラモジュール市場の動向と洞察

スマートフォンのマルチカメラ採用、中国のフラッグシップ機でレンズ3本を超える

中国の携帯電話ブランドはマルチカメラアレイを主流仕様にし、2025年までに平均レンズ数を5つに押し上げます。より大きなセンサーフットプリント、専用の超広角およびマクロシューター、ペリスコープ望遠モジュールにより、スマートフォンが主要なイメージングツールとして強化されています。コンピュテーショナル・フォトグラフィと組み合わせることで、これらのアレイはナイトモード、ポートレート、高ズーム機能を実現し、飽和状態の携帯電話分野でデバイスを差別化します。国内サプライチェーンは急速に拡大し、既存企業に圧力をかけると同時に、カメラモジュール市場をブランド・アイデンティティと消費者のアップグレード意欲の重要な場として高めています。ファーウェイの200MP潜望鏡プロトタイプは、光学的野心の飛躍を示しています。AIを活用したコンピュテーショナル・フォトグラフィは、小さなピクセルからより多くのダイナミック・レンジとノイズ制御を引き出し、ブランドが大型センサーを使わずにプロ級の画像を販売できるようにします。

後方視認性とADASカメラの義務化(FMVSS 111、EU GSR)

米国と欧州連合(EU)の安全規制により、リアビューカメラとサラウンドビューカメラはオプションのアクセサリから必須のコンポーネントへと変貌を遂げました。自動車メーカーは、ブラインドスポットモニター、レーンキープ、歩行者検知の要件を満たすために複数のレンズを統合しており、堅牢で温度耐性に優れたモジュールへの需要が繰り返し生じています。米国NCAPは現在、死角警告、車線維持支援、歩行者自動緊急ブレーキを採点しており、1台当たりのカメラ台数の基準値を引き上げています。そのため、自動車メーカーはコンプライアンス最低基準を上回るサラウンドビューシステムを注文し、センサーノードを増やし、カメラモジュール市場を後押ししています。

2024年台湾地震後のVCMアクチュエータ供給制約

2024年に台湾で発生した地震は、VCMの緊密なエコシステムを混乱させ、供給不足を引き起こし、世界中のスマートフォン組立ラインに波及しました。OEM各社はデュアルソースを加速させ、より低い消費電力とより速い応答時間を約束する圧電代替品を追求しました。部品メーカーは地理的多様化に乗り出し、将来の災害リスクを回避するために東南アジアに生産能力を増強しました。このエピソードは、韓国や中国の大手サプライヤーの垂直統合戦略にも拍車をかけ、重要なアクチュエーターへのアクセスがプレミアムカメラの発売スケジュールの決め手となりました。アルプスアルパインは、調達プレミアムによる利益圧迫を公表し、二拠点製造への多角化を進めています。圧電代替製品は、静音、低電力アクチュエーションを提供し、ニッチなコイルワインダーへの依存度を下げます。

セグメント分析

VCMアクチュエータは、高速オートフォーカスと光学式手ぶれ補正を支え、写真やビデオの性能を差別化する戦略的なレバーとなっています。このセグメントのCAGRは7.2%で、カメラモジュール市場全体のCAGRを上回っています。震災による供給不足が圧電素子やMEMSの代替品開発に拍車をかけたが、VCMはコスト面でも成熟度でも優位性を保っています。同時に、イメージセンサーは2024年に48.8%の売上シェアを占め、オンセンサーメモリを統合した積層アーキテクチャの恩恵を受けて、バーストキャプチャやマルチフレームHDRが可能になります。裏面照射の進歩はノイズフロアを低減し、モバイルや車載アプリケーションのダイナミックレンジを拡大した。

統合動向はVCMとセンサー内位相差検出アルゴリズムをリンクさせ、フォーカスシステムをハードウェアからソフトウェア共生へと移行させる。折り返し光学系や可変開口設計が普及するにつれてレンズセットは複雑化し、モジュール組立メーカーはミクロンレベルの公差を達成するためにアクティブアライメントロボット技術を採用しています。このような変化は、スマートフォンの成長が頭打ちになっても、カメラモジュール市場の単位当たりの価値を高める方向へのシフトを強化します。アクチュエーターの革新とセンサーとレンズの共同開発に投資するサプライヤーは、カメラモジュール業界のマージンカーブのプレミアムエンドに位置します。

CMOSテクノロジーは出荷台数の90.1%を占め、シングルチップ化と低消費電力化によってCCDはほぼ時代遅れになりつつあります。裏面照射型(BSI)はイノベーションの先頭を走っており、夜間撮影や自律走行ビジョン向けの量子効率を高めるため、CAGR 4.24%で拡大しています。ハイダイナミックレンジ(HDR)CMOS設計は、横方向のオーバーフローコンデンサを活用することで、1回の露光で極端な輝度範囲を捕捉できるようになり、厳しい自動車安全要件を満たすようになりました。

3次元スタッキングは、処理ロジックをフォトダイオードプレーンの下に押しやり、信号経路をスリム化し、ピクセルレベルの変化のみを出力するニューロモルフィックでイベントベースのセンシングへの扉を開きます。このようなアーキテクチャは、エッジAIの展開に不可欠な帯域幅とエネルギー需要を削減します。CMOSの継続的な最適化により、カメラモジュール市場は、画像サブシステム全体に連鎖するセンサーの進歩によって牽引され続ける。

8~13MPの帯域は、データ負荷、バッテリー消耗、画像の鮮明さのバランスのおかげで、業界の主力製品として34.7%の売上を維持しています。コンピュテーショナル・フォトグラフィ技術により、ファイルサイズを比例して大きくすることなくディテールをアップスケールできるため、OEMは画素数を増やすよりもソフトウェア・パイプラインを優先できます。デュアルゲインセンサーとマルチフレームフュージョンは、中解像度ハードウェアから優れたダイナミックレンジを引き出し、コスト重視のスマートフォンやIoTビジョンノードにおけるこのセグメントの優位性を強化しています。

逆に、13MPを超える解像度はCAGR 6.8%で上昇しており、フラッグシップのペリスコープカメラ、医療用画像プローブ、きめ細かいディテールを必要とする工業用検査システムなどが牽引しています。クアッドベイヤー・ピクセルビニングにより、これらの高解像度センサーは、フル解像度の日中撮影と低ノイズの夜間撮影を切り替えることができ、電力バジェットを守ることができます。モジュール厚さの制約が続く中、マイクロレンズ設計とディープトレンチ絶縁の技術革新が量子効率の維持に貢献し、カメラモジュール市場のプレミアム層での成長を支えています。

地域分析

アジア太平洋地域は、日本と台湾のセンサー、中国本土のレンズアセンブリ、ベトナムとインドの仕上げラインにまたがる緻密なサプライチェーンに後押しされ、2024年の世界売上高の59.7%を占めました。ニューデリーの生産連動型インセンティブ・プログラムは、国内モジュール組立のための資本支出を払い戻し、多国籍契約メーカーに生産の現地化と納期短縮を促しています。台湾の半導体の深さは、オンカメラAIコプロセッサ用の最先端ロジックを供給し、この地域のシステム的重要性を強化しています。

北米と欧州は、プレミアムハンドセット需要と厳しい車両安全基準を兼ね備えており、高信頼性モジュールへの安定した要求を支えています。米国を拠点とするXRヘッドセット・プログラムでは、深度センサー・アレイのプルアップが追加され、欧州連合のEN 303645サイバーセキュリティ・ベースラインでは、設計サイクルは延長されるもの、堅牢でアップグレード可能なコネクテッド・カメラが得られます。電気自動車の自動運転に対する補助金制度は、カメラを重要な知覚入力としてさらに定着させる。

中東・アフリカはCAGR 6.5%で最も急成長している地域であり、湾岸諸国では交通流と公共安全分析のためにエッジAIカメラを導入するスマートシティの展開が進んでいます。現地のインテグレーターはグローバルなハードウェアベンダーと提携し、FIPS準拠の監視グリッドを展開し、ストレージ、コンピュート、ネットワークのアップグレードの二次需要を喚起しています。南米ではスマートフォンの普及が進み、地域の自動車安全基準がEUや米国の先例に収束するため、長期的な上昇余地があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 中国フラッグシップスマートフォンのマルチカメラ採用率が3レンズを超える

- 後方視認性とADASカメラの義務化(FMVSS 111、EU GSR)

- 中東のスマートシティプロジェクトにおけるAI対応エッジアナリティクス監視の展開

- ペリスコープ/折りたたみ光学ブームモジュールあたりの昇降レンズ数

- インドにおけるPLIスキーム主導のモジュール現地組立

- 米国と韓国におけるXRヘッドセットの3D/深度センシング需要

- 市場抑制要因

- 2024年台湾地震後のVCMアクチュエータ供給制約

- アンダーディスプレイカメラモジュールにおけるウエハーレベル光学系の歩留まり損失

- 積層型CISアーキテクチャに関する特許訴訟の激化

- EN 303645、EUにおけるネットワークモジュールのサイバーセキュリティ対応に遅れ

- 業界エコシステム分析

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 価格分析

- 超小型カメラモジュールのダイナミクス

- 投資分析(組立とテストラインの設備投資)

第5章 市場規模と成長予測

- コンポーネント別

- イメージセンサー

- レンズセット

- カメラモジュールアセンブリ

- ボイスコイルモーター(AFおよびOIS)

- センサータイプ別

- CMOS

- CCD

- ピクセル/解像度別

- 最大7MP

- 8-13 MP

- 13MP以上

- フォーカスタイプ別

- 固定焦点

- オートフォーカス

- 製造工程別

- チップオンボード(COB)

- フリップチップ/ウエハーレベルパッケージング

- モジュール形式別

- コンパクト/CCM

- MIPIインターフェース・モジュール(CSI/DSI)

- 用途別

- モバイル/スマートフォン

- コンシューマー・エレクトロニクス(モバイルを除く)

- 自動車

- ヘルスケアとメディカルイメージング

- セキュリティと監視

- 産業およびロボット工学

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- 東南アジア

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的な動き(M&A、JV、設備投資)

- 市場シェア分析

- 企業プロファイル

- LG Innotek Co. Ltd

- Samsung Electro-Mechanics Co. Ltd

- Sunny Optical Technology(Gp)Co. Ltd

- O-Film Group Co. Ltd

- Hon Hai Precision/Foxconn(incl. Sharp)

- Chicony Electronics Co. Ltd

- LuxVisions Innovation Ltd(Lite-On)

- Cowell E Holdings Inc.

- Sony Group Corporation

- OmniVision Technologies Inc.

- STMicroelectronics N.V.

- AMS Osram AG

- ON Semiconductor Corp.

- Panasonic Corp.

- Largan Precision Co. Ltd

- MinebeaMitsumi(Mitsumi Electric)

- Canon Inc.

- Robert Bosch GmbH

- Continental AG

- Magna International Inc.

- Valeo SA

- e-con Systems Pvt Ltd