|

市場調査レポート

商品コード

1850353

UV LED:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)UV LED - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| UV LED:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 159 Pages

納期: 2~3営業日

|

概要

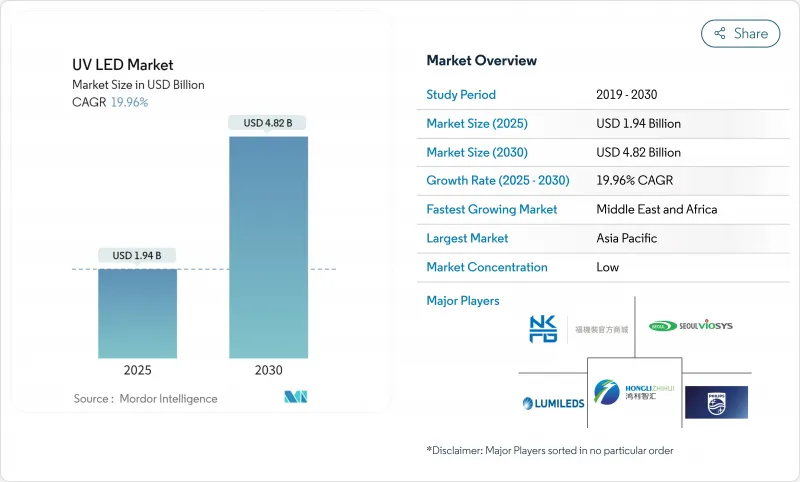

UV LED市場の2025年の市場規模は19億4,000万米ドル、2030年には48億2,000万米ドルに達すると予測され、CAGRは19.96%です。

成長の原動力は、世界的な水銀ランプ禁止、エネルギー効率の高い硬化ソリューションへの需要の急増、チップの量子効率の急速な向上です。水俣条約、EU RoHS、カナダの水銀規制のスケジュールは2027-2025年に収束し、エンドユーザーをUV LED採用に向けて後押しします。AlGaNエピタキシー、フリップチップ構造、熱管理の並列進歩により、ディープUVデバイスの外部量子効率は250mAで9.19%に上昇し、従来の水銀ランプとの性能差が縮まりました。印刷、包装、水処理分野での置き換えの勢いは強く、サプライヤーは2030年までの収益の見通しを強化しています。

世界のUV LED市場の動向と洞察

UV LED採用を加速する厳しい水銀ランプ段階的廃止政策

世界的な規制により、照明の水銀源が廃止されつつあります。水俣条約は、2027年の蛍光灯廃止に向け147の署名国を一致させました。EUのRoHS指令はすでに水銀含有量をランプ1個当たり5mgに制限しており、2027年以降は全面禁止となる見込みです。カナダの2025年規則はこの方向性を反映しています。ユーザーの移行に伴い、水銀ランプをソリッドステート・アレイに交換した印刷ラインでは、エネルギー使用量が85%減少したと報告されています。そのため、UV LED機器の事前認定を受けたベンダーは、長期的な改修契約を確保しています。

アジア全域で水の消毒需要が急増

急速な都市化により、インド、インドネシア、中国沿岸部では中央給水網にストレスがかかっています。ノルウェーの実地試験では、LEDリアクターを使用して545 m3/日で3-logの大腸菌群除去が実証され、この技術が市水域での利用が可能であることが証明されました。コンパクトな形状により、家庭用ディスペンサー、小規模工場、農村部の診療所などにUV-Cエミッターを組み込むことができます。アジアの機器メーカーは、ソーラー・マイクログリッドで動作する統合型モジュールの規模を拡大しており、オフグリッドでの水の安全性向上を加速しています。

高出力アプリケーションを制限する量子効率の天井

280nm以下の深紫外LEDのウォールプラグ効率は通常5%未満で、低圧水銀灯の20~30%をはるかに下回る。キロワットスケールの出力を必要とする水道事業者は、大規模なLEDアレイを導入しなければならず、資本コストが膨らみます。現在、量子ドット、超格子、透明基板に焦点を当て、正孔注入と光抽出を改善しています。AlGaN超格子の設計により、35mWでの外部量子効率は8.6%に向上したが、このような性能での量産にはまだ数年かかります。

セグメント分析

2024年のUV-Aシステムの売上シェアは72%で、グラフィックアートの硬化と偽造品検出で優位を保っています。一方、UV-Cは、ヘルスケアや自治体ユーザーが水銀フリーの殺菌ソリューションを導入することから、CAGRは22.5%となります。amsオスラムのOSLON(TM)UV 3535は、265nmで115mWを供給し、寿命は20,000時間で、信頼性の高い水および空気リアクターの重要なマイルストーンとなります。UV-Bニッチは光線療法と農業用光形態形成に対応し、特殊な需要ポケットを形成しています。

採用の動きは地域によって異なります。欧州では食品加工用パイプラインに255~275nmのエミッターを標準化し、日本では皮膚科用に308nmのUV-Bを模索しています。量子効率の向上が続く中、医療用空気殺菌をターゲットとするUV-CモジュールのUV LED市場規模は2030年までセクター平均の2倍で成長すると予測されています。遠UVC222nmエキシマエミッターのブレークスルーは、居住空間の人体に安全な連続殺菌を約束し、使用事例のフロンティアをさらに広げます。

モジュールは、統合が容易なため、2024年の売上高の42%を占める最大のスライスを維持した。しかし、チップは、民生機器や実験機器でのカスタム光エンジン需要を反映して、CAGR 23.7%を記録します。GaN-on-SiC基板は熱抵抗を低減し、2025年プロトタイプではチップレベル出力100mWを可能にします。ランプサブセグメントは、レトロフィットソケットに対応しているが、アレイが牽引するにつれて徐々に数量が減少しています。

超小型チップは、新たなバイオセンサーやラボオンチップ・デバイスを支えています。調査チームは、90nmの寸法で20%の外部量子効率を持つナノスケールのペロブスカイトLEDを実証しました。パッケージングがセラミックから成型複合材料に移行するにつれて、ミリワットあたりの中央コストは低下しており、ポータブル殺菌ガジェットのデザインインが刺激されています。その結果、チップレベルの売上におけるUV LED市場シェアは、2030年までに35%に上昇すると予測されます。

地域分析

アジア太平洋地域は、2024年のUV LED市場収益の55%を占める。中国の自立化推進により、現地エピタキシーサプライヤーやキャプティブデバイスパッケージングラインが誕生しています。日本と韓国は高精度製造のノウハウを加え、台湾は深紫外線チップ用の窒化ガリウム基板に特化しています。公衆衛生予算の増加により、巨大都市ではUVベースの水や空気浄化の需要が高まり、この地域の優位は揺るぎないものとなっています。

北米は第2位。カリフォルニア州では水銀ランプの段階的廃止が加速しており、国内チップ生産能力に対する連邦政府の資金援助も相まって、ヘルスケアと先端製造業での採用が進んでいます。しかし、特許の密集と人件費の高騰が、事業拡大のペースを抑えています。欧州は、エネルギー効率向上の義務化によって、その後に続いています。エコデザイン規則では、2030年までに設置されるランプの96%がLEDになると予測されており、UVソリューションを受け入れる環境が整いつつあります。

中東・アフリカは最も急成長している地域であり、海水淡水化プラントや新しい病院がLEDリアクターを導入しているため、CAGRは20.4%となっています。湾岸諸国は、水銀を含まない照明を指定するスマートシティプログラムに資金を提供しています。南米では、飲料ボトリングと水産養殖に勢いがあるが、自治体の水道事業は認証サイクルの関係で動きが鈍いです。どの地域でも、規制と技術の成熟が同時に進行しているため、UV LED市場は収束的な上昇を続けています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EUとカリフォルニアにおける厳格な水銀ランプ廃止政策がUV-LEDの導入を加速

- COVID-19後のアジア全域で使用場所での水消毒需要が急増

- 食品安全コンプライアンスのためのフレキシブル包装における低移行性インクへの急速な移行

- 欧州のエネルギー価格高騰により低出力UV-LED硬化ラインが有利に

- ミニLEDバックライトのロードマップが半導体工場における深紫外線検査ツールの採用を促進

- 空港や病院の占有空間の空気清浄に遠紫外線(222 nm)が広く受け入れられるようになっている

- 市場抑制要因

- AlGaNベースのUVCチップの量子効率の上限(<5%)が高出力アプリケーションを制限

- ロイヤリティ重視の知的財産情勢が北米の新規参入者のコスト障壁を高める

- 工業用硬化ラインにおける高密度アレイの熱管理の課題

- 新興国における地方水道事業の遅延を招いている遅い認証サイクル(NSF/ANSI 55-2022)

- 業界エコシステム分析

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- テクノロジー別(波長)

- UV-A

- UV-B

- UV-C

- 製品/フォームファクター別

- ランプ

- モジュール

- 配列

- チップ

- 出力別

- 低消費電力(10 mW未満)

- 中出力(10~100 mW)

- 高出力(100 mW超)

- 用途別

- 硬化(インク、コーティング、接着剤)

- 消毒と滅菌

- センシングと計測

- 医療と光線療法

- 偽造品検出とセキュリティ

- 園芸と屋内農業

- その他のニッチ用途(3Dプリンティング、リソグラフィー)

- エンドユーザー業界別

- ヘルスケアとライフサイエンス

- 印刷と包装

- エレクトロニクスおよび半導体

- 水道・下水道事業

- 食品・飲料加工

- 自動車と航空宇宙

- 住宅および商業ビル

- 工業製造業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- 東南アジア

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- ams OSRAM AG

- Signify N.V.

- Nichia Corporation

- Seoul Viosys Co., Ltd.

- Crystal IS Inc.(Asahi Kasei)

- Lumileds Holding B.V.

- Nikkiso Co., Ltd.(UV Business)

- LG Innotek Co., Ltd.

- LITE-ON Technology Corp.

- Honlitronics(Hongli Zhihui Group)

- Stanley Electric Co., Ltd.

- SemiLEDs Corporation

- Violumas Inc.

- DOWA Electronics Materials Co., Ltd.

- Nordson Corporation

- Luminus Devices, Inc.

- Heraeus Holding GmbH(Noblelight)

- Phoseon Technology(Excelitas)

- Sensor Electronic Technology Inc.(SETi)

- Bolb Inc.