|

市場調査レポート

商品コード

1850349

マイクロLED:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Micro LED - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| マイクロLED:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月22日

発行: Mordor Intelligence

ページ情報: 英文 143 Pages

納期: 2~3営業日

|

概要

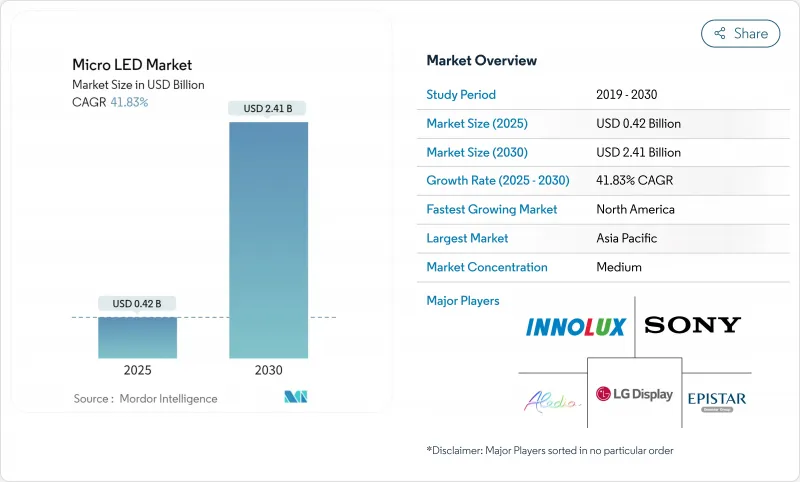

マイクロLED市場は、2025年に4億2,000万米ドル、2030年には24億1,000万米ドルに達し、CAGR 41.83%で成長すると予測されています。

商業的な牽引力は、この技術の高輝度、低電力消費、LCDやOLEDディスプレイを上回る実証済みの寿命にかかっています。メーカーは量産歩留まりを着実に引き上げており、台湾と韓国の資本集約的なパイロット・ラインは、ウェアラブル、大型看板、自動車のコックピット向けにこの技術を拡大しています。アジア太平洋は、成熟した半導体エコシステムと支援的な産業政策を背景に製造主導権を握っており、北米は防衛とAR/VRプログラムへの投資を加速しています。価格は高止まりしているが、電力、熱、太陽光の読み取り性能に厳しい制約があるエンドユーザーが先行しているため、マイクロLED市場の長期的な競争力が強化されています。

世界のマイクロLED市場の動向と洞察

AppleとSamsungのマイクロLEDウェアラブル向けロードマップが小型ディスプレイ需要を加速

アップルによるLuxVue買収後の30億米ドルの支出とサムスンの並行研究開発プログラムは、目先のスケジュール変更にもかかわらず長期的なコミットメントを示すものです。ドライバICと搬送装置サプライヤのデザインウィンの増加は、サプライチェーンが2インチ以下のパネルに軸足を移していることを示しています。スマートウォッチ用ディスプレイのCAGRは45%と予測されます。専門ツールベンダーは、高スループットのピックアンドプレースシステムを商品化しており、フラッグシップブランド以外のパイロット生産の民主化に貢献しています。このダイナミックな動きは、市場をリードする2社の戦略的ロードマップが、マイクロLED市場全体の広範な資本配分を形成していることを明確に示しています。

GCCと東アジアにおける透明でフレキシブルなリテールサイネージの普及

ドバイの高級モールやソウルの旗艦店では、ベゼルレスの透明なマイクロLEDファサードを設置し、デジタルコンテンツと実店舗を融合させています。Tianma社のPIDプロトタイプは、4,000nitの屋外輝度に対応するよう設計されており、LCDの代替品と比較した場合の性能の優位性を示しています。モジュラーアーキテクチャーは、カスタム寸法を簡素化し、リテールインテグレーターの設置サイクルを短縮します。また、エネルギー効率により、24時間365日稼動する場合の総所有コストも削減できます。これらの特性は、デジタル・サイネージが持つ38%のアプリケーション・リードを守り、マイクロLED市場内の新たな収益プールの舞台となります。

4インチウエハを超えるサブ10µm LEDの量産歩留まりは60%以下

大型基板上の数百万個のマイクロエミッターの配置精度は依然として60%以下であり、スクラップ率を高め、ライン稼働率を低下させています。装置メーカーは、99.99%の配置精度を達成するために、レーザー誘起転写と電磁ピックアップを試しており、ビューリアルのMicroSolid Printingはサブ7µmピッチの能力を実証しています。これらのソリューションが成熟するまでは、出力コストはOLED同等品よりも高く、マイクロLED市場内の量販テレビやスマートフォンへの短期的な普及は限定的です。

セグメント分析

デジタルサイネージは2024年の売上高の38%を占め、マイクロLEDがインパクトが強く、昼光でも読み取れるビデオウォールに適していることが実証されました。高級小売チェーンでは、シームレスなキャンバスを形成するモジュール式タイルが採用され、交通機関では、重要なインフォメーションボードにマイクロLEDの低故障率が採用されています。同分野の安定した受注が早期の稼働率を支えており、マイクロLED市場を強化しています。

これとは対照的に、スマートウォッチの出荷台数は家電製品のリリースサイクルに合わせて増加します。バッテリーが限られたウェアラブル端末は1ワット以下のディスプレイを要求し、ピーク輝度3,000ニットは屋外での使い勝手を向上させる。このセグメントの予測CAGRは45%であり、極めて重要な数量牽引役となっています。ニアアイARモジュールも、画素密度が4,000 PPIを超えるにつれて進歩し、より広範な採用の舞台を整え、小型パネルの末端におけるマイクロLED市場規模の長期的拡大を支えています。

高級テレビ、時計、スマートフォンがこの技術の高コントラストと長寿命を採用したため、家電が2024年の需要の72.1%を占めました。サムスンのフラッグシップ・テレビ「ザ・ウォール」は、大画面のショーケースに設置され、プレミアム価格を実現しています。この分野は、バックプレーン、ドライバIC、検査ツールなどの部品需要を安定させ、マイクロLED市場における中心的な役割を果たしています。

欧州の太陽視認性規制が強化される中、自動車需要はCAGR 47%で増加しています。HUDのプロトタイプは10,000ニット以上を達成し、偏光フロントガラスを通しての視認性を確保しています。拡張温度耐性と耐振動性もAEC-Q基準を満たしています。より多くの自動車メーカーが高度なドライバー用ディスプレイを統合するにつれて、コックピット・エレクトロニクスのマイクロLED市場規模は拡大し、消費者向けガジェット以外の収益も多様化します。

50インチ以上のパネルは2024年の収益の55.6%を占める。高級住宅や企業のロビーでは、設置の柔軟性と比類のないピーク輝度がプレミアム価格を正当化する110インチから220インチのアセンブリが採用されています。ハイエンドのホスピタリティ施設では、ベゼルフリーサーフェスを活用して没入感を演出し、マイクロLED市場でのシェア優位性を高めています。

10インチ以下のパネルは、製造上のブレークスルーによりダイ当たりのコストが低下するため、2030年までCAGR 49%で成長します。1インチ以下のマイクロ・ディスプレイはVRヘッドセット向けに6,500 PPIに達し、自動車のスマート・インストルメント・クラスターは小型で高解像度のフォーマットを要求しています。高度な転写印刷の採用は学習曲線を早め、10年後には小型パネルの数量がますます市場力学を再形成することを示唆しています。

地域分析

アジア太平洋地域は2024年の売上高の46.9%を占め、台湾の後工程における役割と韓国の深いディスプレイ・ノウハウがその原動力となっています。BOEによるHC SemiTekの買収とSananの20億米ドルのファブ計画は、継続的な資本流入を強調するものです。GaNウエハーの輸出リベートを含む政府の支援策により、地域のコスト優位性が維持され、マイクロLED市場でのリーダーシップが強固なものとなっています。

北米は2030年までCAGR 43%で最も急成長しています。CHIPS法に基づく連邦政府の優遇措置が新しい窒化ガリウム製造ラインに拍車をかけ、防衛とAR/VRプログラムがオフテイク契約を固定化します。アップルのマルチサイトR&D拠点とメタのヘッドセットへの意欲は、エコシステムの活動を集中させ、強固な設計の反復を促し、基板需要の増加を支えます。

欧州は、車載および産業用途で専門的な役割を果たします。太陽電池の可読性が義務化されたことでHUDの統合が加速し、現地のティア1サプライヤーはアジアのLEDメーカーと協力して安定したダイフローを確保します。クリーンルームの改修に対するEUの並行補助金は、アジア集中に対する戦略的ヘッジを提供しながら、新興ウエハー供給基盤を育成します。中東・アフリカでの採用は、GCCモールの高級小売店用サイネージから始まり、ラテンアメリカではスポーツ・インフラ投資と連動した大型会場用ディスプレイが試験的に導入されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- アップルとサムスン、マイクロLEDウェアラブル向けロードマップを発表、小型ディスプレイの需要を加速

- 湾岸協力会議諸国と東アジアにおける透明で柔軟な小売看板の普及

- 米国とEU政府が資金提供する防衛グレードのマイクロディスプレイ

- 台湾のミニLEDコスト低下によりマイクロLEDのパイロット生産が可能に

- 欧州の自動車太陽光視認性基準がマイクロLED HUDの統合を促進

- 市場抑制要因

- 4インチウエハーを超える10μm以下のLEDの質量移動収率は60%未満

- 非標準化自動車資格プロトコル

- GaN-on-Siウエハー供給のアジアへの集中

- 6億米ドル以上の設備投資要件が南米とアフリカでの事業拡大を制限

- 業界エコシステム分析

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 用途別

- スマートウォッチ

- 近接視デバイス(AR/VR)

- テレビ

- スマートフォンとタブレット

- モニターとラップトップ

- ヘッドアップディスプレイ

- デジタルサイネージ

- マイクロプロジェクター

- 医療および外科用ディスプレイ

- 産業用検査パネル

- 最終用途産業別

- コンシューマーエレクトロニクス

- 自動車

- 航空宇宙および防衛

- ヘルスケア

- 広告と小売

- 工業および製造業

- その他

- パネルサイズ別

- 10インチ未満(小型およびマイクロディスプレイ)

- 10~50インチ(中)

- 50インチ以上(大)

- ピクセルピッチ

- ファインピッチ(1.5 mm未満)

- 標準(1.5~2.5mm)

- 大きい(2.5 mm以上)

- テクノロジー別(カラー)

- RGBフルカラー

- モノクロ

- コンポーネント別

- エピタキシャルウェーハ

- バックプレーン

- ドライバIC

- 転写・接合装置

- 検査および修理ツール

- 製造工程別

- 物質移動

- エピタキシャルウエハーボンディング

- ハイブリッドボンディング

- 提供別

- ディスプレイモジュール

- 照明モジュール

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- 東南アジア

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Samsung Electronics Co. Ltd.

- Sony Corporation

- LG Display Co. Ltd.

- BOE Technology Group Co. Ltd.

- AU Optronics Corp.

- Epistar Corporation

- PlayNitride Inc.

- Innolux Corporation

- Apple Inc.(LuxVue Technology)

- Tianma Microelectronics Co. Ltd.

- Nichia Corporation

- Sharp Corporation

- VueReal Inc.

- Plessey Semiconductors Ltd.

- Aledia SA

- Ostendo Technologies Inc.

- Rohinni LLC

- Leyard Optoelectronics Co. Ltd.

- Seoul Semiconductor Co. Ltd.

- San'an Optoelectronics Co. Ltd.

- Allos Semiconductors GmbH

- Optovate Ltd.

- Foxconn(Hon Hai Precision)

- Konka Group Co. Ltd.