|

市場調査レポート

商品コード

1851637

小型風力タービン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Small Wind Turbine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 小型風力タービン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月28日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

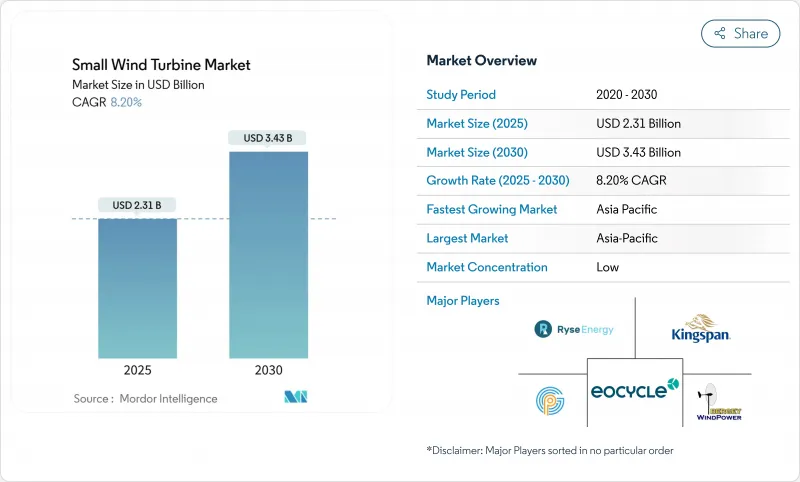

小型風力タービンの市場規模は2025年に23億1,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは8.20%で、2030年には34億3,000万米ドルに達すると予測されます。

成長の原動力は、政策的インセンティブ、垂直軸技術の進歩、電気通信、農業、分散型エネルギーシステムでの利用の高まりです。北米、欧州連合、アジアにおける公的資金援助プログラムが導入を加速し、機械学習によるタービンの最適化が生涯エネルギーコストの削減と信頼性の向上を実現します。企業の電力購入契約は送電網上のプロジェクトの需要を拡大し、風力と太陽光のハイブリッドシステムは、風力資源が変動しやすい地域で対応可能な市場を拡大します。10kW未満の分野では、屋上ソーラーとのコスト競争が依然として抑制要因となっているが、効率向上と新しい設置規則がその差を縮めています。

世界の小型風力タービン市場の動向と洞察

カリブ海の離島の急速な電化

離島の電力会社は、ディーゼルシステムを小型風力タービンを含むハイブリッド再生可能マイクログリッドに置き換えつつあります。政府および多国間金融機関は、プロジェクトの初期費用を削減し、開発者の参加を拡大する譲許的資金を確保しています。耐腐食性コーティングやモジュール式ロジスティクスパッケージを提供するタービンサプライヤーは、こうした市場で競争上の優位性を獲得しています。1カ所当たりの平均設置容量は50kW未満にとどまり、0~20kWの製品ラインナップを揃えています。安定した貿易風が35%以上の発電容量を支え、太陽光発電のみの設計に比べて投資回収期間が改善されます。島嶼部の電化プログラムでは、高い稼働率に見合うパフォーマンスベースの料金体系が採用されており、新型タービンに統合されたデジタル監視プラットフォームの価値が強化されています。

米国農務省の農村エネルギー補助金による5kW未満のタービン需要の急増

2025年に割り当てられる1億8,000万米ドルのRural Energy for America Programは、農場や地方の中小企業向けの小型風力発電システムを優先しています。助成金は資本コストの最大50%をカバーし、平均風速が6m/sを超える地域では6年以内の投資回収を可能にします。国立再生可能エネルギー研究所の競合改善プロジェクトは、プロトタイプ認証に資金を提供し、第三者の融資を受けられるようにすることで、過去の融資可能性のギャップに対処します。400カ所以上の農場を対象とし、2027年までにマイクロクラスの累積設置量を25メガワット増加させる。タービンとバーンルーフソーラーアレイを組み合わせることで、生産者は昼間のピーク負荷と夕方の灌漑需要を相殺することができます。このプログラムでUL 6141認証を取得したメーカーは、連邦政府からの調達で優遇される資格を得る。

欧州都市部における高さに基づくゾーニング規制

地方自治体の高さ制限により、多くの歴史的地区ではタービンのハブの高さが10m以下に制限され、エネルギー収量が抑制されています。可変性の要求には、シャドウフリッカーや視覚的評価が必要となることが多く、プロジェクトのスケジュールが長くなります。騒音測定規則が経験的データではなくモデル化されたものに依存しており、エンジニアリングコストがかさみます。管轄が分断されているため、同じプロジェクトでも隣接する自治体間でルールが異なり、開発者の都市全体への展開意欲を削いでいます。EUの風力発電パッケージのガイダンスは調和を求めているが、地元の文化財保護団体が拒否権を保持しています。サプライヤーは、パラペットの下に収まるスタブマストの垂直軸設計で対応しているが、掃引面積の減少により年間出力は減少します。

セグメント分析

水平コンフィギュレーションは、実証された空気力学とサプライチェーンの成熟度により、2024年の売上の68%を維持した。このセグメントは、大農場のリパワリングと農村の家庭用リプレースメントを支配しています。メーカーは、米国農務省やインドの通信事業者の入札仕様を満たすために2~20kWのモデルを標準化し、量的経済性を活用しています。垂直軸ユニットの小型風力タービン市場規模は、低いベースから急成長し、CAGR 14%を記録し、水平軸ユニットを上回ると予測されます。垂直軸型風力タービンは、屋上や街頭の電柱付近の乱れた風の流れの中で威力を発揮し、全方向性のブレードが多方向の突風をとらえます。各回転でピッチを調整する遺伝的学習アルゴリズムは、出力係数を最大0.45向上させ、ベッツ限界ベンチマークに近づけます。可動部品の削減により、地上ギアボックスの設置が可能になり、メンテナンス・トラック・ロールを30%削減し、商用フリートへの採用を促進します。

垂直軸のサプライヤーは、ファサードエンジニアと提携し、タービンをカーテンウォールに組み込むことで、EUの革新的技術割当を満たします。ローターが逆回転するSavoniusとDarrieusのハイブリッドは、トルクリップルを最小限に抑え、5mの距離で35dB以内の音響シグネチャーを実現。東京大学のフィールドテストでは、台風の突風下でも15年の軸受寿命が確認され、耐久性に関する認識に対応。デベロッパーはサービスとリサイクル義務をバンドルしたリース契約を構成し、中国とEUの循環型経済規則を満たします。垂直タービンを破壊的ではなく補完的なものとして位置づけ、敷地内のエネルギー出力を平準化する混合アレイを可能にしています。

2024年の小型風力タービン市場シェアは、0~5kWのマイクロクラスが46%を占め、農場、キャビン、道路脇のセンサーへの補助金による設置に支えられています。電子機器のコモディティ化により平均販売価格は前年比6%下落したが、設置後のサービス収入は増加しました。21~100kWの中型ユニットは2030年までCAGR 11%で拡大し、通信タワー、工業団地、データセンター・キャンパスに供給されます。フォールト・ライドスルーと無効電力サポートを統合し、個別のコンバーターなしでグリッド接続を可能にするIEC 61400-2認証モデルが開発者に好まれています。60 kWの規模になると、kWあたりの単価は2,300米ドルを下回り、屋上ソーラー+蓄電スタックとの差が縮まる。

6~20kWの小型風力タービンの市場規模は、系統料金にデマンドチャージが含まれる都市近郊のビジネス団地で着実に成長しています。冷蔵負荷の高い農家では、夕方のピークを相殺するために15kWのタービンが選ばれています。歴史的な導入は、プロジェクトのリードタイムを短縮する設置業者のスキルの蓄積から恩恵を受けています。中堅クラスのサプライヤーは、97%の技術的可用性を保証する延長保証をバンドルし、グリーンバンクから低コストの負債を引き出します。相互運用可能なSCADAが、風力発電の出力をオンサイトのバッテリー配給にリンクさせ、自家消費を最適化し、相互接続の抑制を回避します。

小型風力タービン市場レポートは、軸タイプ(水平軸風力タービン、垂直軸風力タービン)、定格容量(0~5KW、6~20KW、21~100KW)、接続性(オフグリッド、オングリッド、ハイブリッド)、設置場所(屋上/ビル一体型、独立タワー)、用途(住宅、商業、その他)、地域(北米、欧州、アジア太平洋、南米、その他)で区分されています。

地域分析

2024年の小型風力タービン市場はアジア太平洋が48%のシェアを占め、中国の産業脱炭素化とインドの通信電化を背景にCAGR10%で成長しています。中国では、2030年までに認証グリーン工場生産量を40%にすることが義務付けられており、経済区は屋上や中庭にタービンを設置するよう求められています。インドのタワー事業者はバックアップ電源として再生可能エネルギーに取り組んでおり、ハイブリッドの入札では太陽光発電やリチウムパックとともに5kWのマイクロタービンが指定されています。日本は厳しい音響規制を維持しながらも、鉄道通路付近での垂直軸の実証実験を支援しています。ASEANの島国はコミュニティ・マイクログリッドを導入し、ベトナムのメーカーは地域の漁船団に10kWのタービンを輸出しています。

欧州は、規制の明確化が漸進的成長を支える成熟した基盤であり続けています。再生可能エネルギー指令の改正により、50kW未満のプロジェクトの許認可の遅れが削減され、都市部での導入が促進されています。ドイツでは、一部のランダーにおいて10m未満のタービンの計画認可が免除され、ソフトコストが25%削減されます。ノルスク・ハイドロ社の29年間235MW風力発電PPAは、長期売電の信頼性を示すものです。デンマークの厳しい騒音上限39dBは、世界中に輸出される製品の音響に影響を与えています。英国は、地域社会への利益配分を目的としたマイクロタービンを含む、島の陸上風力発電の拡張を支援しています。

北米の政策が需要を回復。米国農務省の1億8,000万米ドルの助成金プールは農場への導入を加速させ、NRELの320万米ドルの競争力強化基金は認証経路を前進させる。カナダでは、Nordex社のユーティリティ・スケール・タービンに対する247MWの注文が殺到し、部品の現地化が進んでいます。しかし、住宅用風力発電の導入は、屋根上太陽光発電の価格優位性により遅れています。ニューヨークのような州では、小形風力発電に特化した固定価格買取制度を試験的に導入しており、カリフォルニア州では、複数の技術によるシステムに報酬を与えるマイクログリッド料金制度を試験的に導入しています。メキシコの農村電化庁が、オフグリッド診療所向けの1.5kW風力ユニットを含むハイブリッドキットの入札を再開。

- Aeolos Wind Energy LtdBergey

- Windpower Co.

- City Windmills Holdings PLCWind

- Energy Solutions BVSD

- Wind Energy LtdUNITRON

- Energy Systems Pvt LtdNorthern

- Power Systems Inc.

- Shanghai Ghrepower Green EnergyTUGE

- Energia OURyse

- EnergyKingspan

- Group Plc(風力部門)

- Eocycle Technologies Inc.

- XZERES Wind Corp.

- Fortis Wind Energy BVHY

- EnergyEndurance

- Wind Power Inc.

- Kliux Energies InternationalPika

- Energy(Generac)

- Envergate Energy AGSuzlon

- Energy Ltd(<=100 kWセグメント)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- カリブ海の離島の急速な電化

- 米国農務省「アメリカのための農村エネルギー」補助金による5kW未満タービン需要の急増

- オンサイト再生可能エネルギーを義務付ける中国の「ゼロカーボン工業団地

- EUの屋上再生可能エネルギー指令がビル風力発電を後押し

- インドとASEANにおけるテレコムタワー・ハイブリッド化のアジェンダ

- 北欧のデータセンター・クラスターにおけるマイクロウインドの企業PPAの増加

- 市場抑制要因

- 欧州都市部における高さによるゾーニング規制

- 日本で強化される音響放射基準

- 北米における10kW未満の屋根上太陽光発電と高LCOEの比較

- アフリカにおける長期的O&Mエコシステムの不在によるバンカビリティ・ギャップ

- サプライチェーン分析

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場規模と成長予測

- 軸タイプ別

- 水平軸風力タービン(HAWT)(アップウィンド、ダウンウィンド)

- 垂直軸型風力タービン(VAWT)(サボニウス、ダリウス、ジャイロミル)

- 定格容量別(kW)

- 0~5 kW(マイクロ)

- 6~20 kW(小型)

- 21~100 kW(中型)

- 接続性別

- オフグリッド

- オングリッド

- ハイブリッド(風力+バッテリー/PV)

- 設置場所別

- 屋上/ビル一体型

- 独立型タワー(地上設置型)

- 用途別

- 住宅用

- 商業(小売、オフィス、ホテル)

- 工業および倉庫業

- 農業・水産養殖

- テレコムタワーと遠隔監視サイト

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- 北欧諸国

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- エジプト

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 戦略的な動き(M&A、パートナーシップ、PPA)

- 市場シェア分析(主要企業の市場ランク/シェア)

- 企業プロファイル

- Aeolos Wind Energy Ltd

- Bergey Windpower Co.

- City Windmills Holdings PLC

- Wind Energy Solutions BV

- SD Wind Energy Ltd

- UNITRON Energy Systems Pvt Ltd

- Northern Power Systems Inc.

- Shanghai Ghrepower Green Energy Co. Ltd

- TUGE Energia OU

- Ryse Energy

- Kingspan Group Plc(Wind Division)

- Eocycle Technologies Inc.

- XZERES Wind Corp.

- Fortis Wind Energy BV

- HY Energy Co. Ltd

- Endurance Wind Power Inc.

- Kliux Energies International

- Pika Energy(Generac)

- Envergate Energy AG

- Suzlon Energy Ltd