セメント板- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Cement Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687387

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

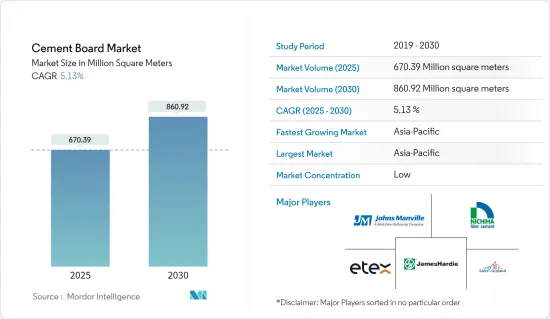

セメント板市場規模は2025年に6億7,039万平方メートルと推定され、予測期間(2025年~2030年)のCAGRは5.13%で、2030年には8億6,092万平方メートルに達すると予測されます。

主なハイライト

- 住宅および商業建築における採用の増加と、耐衝撃性と耐久性という望ましい特性が、予測期間中のセメント板市場を牽引すると予想されます。

- しかし、従来のものと比べて初期コストが高いことが市場成長の妨げになると予想されます。

- とはいえ、美観を向上させようとする動向の高まりは、市場に新たな機会を生み出すと予想されます。

- アジア太平洋地域が市場を独占すると予想され、需要の大半は中国とインドによるものです。

セメント板市場の動向

住宅および商業建築における採用の増加

- セメント板は、耐久性、耐火性、耐湿性、費用対効果などのユニークな組み合わせを提供するため、住宅建設によく使われます。

- 商業分野は、セメント板市場における極めて重要な企業として際立っており、オフィス部門がその先頭を走っています。世界の商業活動の急増に伴い、この分野でのセメント板の需要も増加しています。

- オフィススペースの拠点として急成長しているアジア太平洋は、商業建築のトップ市場にランクされています。インドや中国のような国々では、テクノロジー、eコマース、銀行などのセクターに牽引され、オフィススペースの需要が一貫して増加しており、新規オフィス建設が相次いでいます。

- インドでは新興企業のエコシステムが急成長しており、オフィススペースに対する意欲が高まっています。政府の取り組みも後押しし、インド産業・国内貿易振興省(DPIIT)は2023年12月までに1,17,254の新興企業が設立されると予測しています。

- 米国もまた、建築・建設業界にとって巨大な市場です。米国国勢調査局のデータによると、2023年、米国は民間の非住宅建築物の新築に7,061億米ドル以上を費やし、2022年の5,965億米ドルから大幅に増加しました。さらに、2023年の住宅建設は8,649億米ドルにとどまりました。

- 2023年には、推定146万9,800戸の住宅建設が許可され、2022年の166万5,100戸を11.7%下回りました。さらに、2023年に着工された住宅戸数は推定1,413,100戸で、2022年の1,552,600戸を9%(+2.5%)下回りました。

- 2024年7月の建築許可による民間住宅着工戸数の季節調整済み年率は1,396,000戸でした。この数値は、6月の改定値145.4万戸から4%減少し、2023年7月の151.1万戸から7%減少しました。

- ドイツの堅調な経済は、商業スペース、特に高品質でESGに準拠したオフィスビルへの需要を促進しており、これはプライム賃料の上昇からも明らかです。2023年第3四半期には24万6,000平方メートルのオフィススペースが竣工し、2024年には180万平方メートルに達すると予測されています。小売スペース開発、特にショッピングセンターも2023年に一貫した成長を見せた。

- ブラジルの住宅セクターは、急速な都市化に後押しされ、大幅な民間投資を集めています。この急増する需要に対応するため、政府は2023年2月に「Minha Casa, Minha Vida(我が家、我が人生)」プログラムを再導入し、2026年までに200万件の新規プロジェクトを建設するという野心的な目標を掲げました。

- サウジアラビアでは、ジェッダ・セントラル巨大プロジェクトに代表される建設ブームが起きています。公共投資基金(PIF)の子会社であるジェッダ中央開発会社(JCDC)が主導するこの野心的な200億米ドルのプロジェクトには、博物館、オペラハウス、スポーツスタジアムなどのランドマークに加え、17,000戸の住宅と3,000軒以上のホテルが含まれます。第1段階は2027年に完成予定で、さらなる開発は2030年以降まで続きます。

- こうした動きは、住宅と商業建築の両方におけるセメント板の需要が世界的に旺盛であることを裏付けており、予測期間中の成長も有望です。

アジア太平洋が市場を独占する見込み

- アジア太平洋は、中国を筆頭に世界のセメント板市場で支配的な地位を占めています。セメント板は、住宅と商業の両分野にまたがる中国の多様な建設活動で広範な用途を見出しています。

- 中国は積極的に都市化を進めており、2030年までに都市化率70%を目指しています。この都市化は、より多くの居住空間に対する需要を促進し、より良い住環境を求める中間層の願望を反映しています。こうした力学は、住宅市場と住宅建設を後押しし、セメント板市場にプラスの影響を与えると思われます。

- 中国の香港では、住宅当局が手ごろな価格の住宅建設を開始するために複数の施策を開始しました。当局は、2030年までに30万1,000戸の公共住宅を供給する目標を掲げています。

- 2025年までに2億5,000万人の農村住民を新たな巨大都市に移転させる計画もあり、中国政府の野心的な建設構想はセメント板市場を後押しすることになりそうです。

- 苦境にあえぐ経済への対応として、中国の知事は主要な建築プロジェクトの予算を20%近く増額しています。中国の3分の2以上の地域が、交通インフラや工業地帯を含む重要なプロジェクトに取り組んでおり、2024年の総予算は12兆2,000億人民元(1兆8,000億米ドル)を超えます。

- 中国における可処分所得の増加は、ショッピングモールやホテルなどの高級商業スペースの需要を促進しています。中国はショッピングセンター開発の最前線に立っており、既存のセンターは4,000近く、2025年までにさらに7,000になると推定されています。2021年第3四半期に着工し、2025年第4四半期に完成予定の武漢Fosun Bund Center T1のようなプロジェクトは、市場をさらに強化しています。

- インドでは、手ごろな価格の住宅が70%増加する見込みです。インベスト・インディアによると、建設セクターは2025年までに1兆4,000億米ドルの評価額を達成すると予測されています。2030年には人口の30%以上が都市居住者になるという予測もあり、2,500万戸以上の中級住宅と手頃な価格の住宅が急務となっています。不動産法、GST(物品・サービス税)、REIT(不動産投資信託)などの最近の改革は、認可を迅速化し、建設業界を強化することを目的としており、市場の成長を促進しています。

- 韓国は大規模な産業建設事業に取り組んでいます。特筆すべき例は、S-Oil Corp.が蔚山に建設中の野心的なシャヒーン製油所統合石油化学プラントで、2026年の完成を目指しています。この施設には、世界最大のナフサ供給型スチームクラッカーが設置され、年産180万トンのエチレンを生産することができます。

- こうした動きから、アジア太平洋のセメント板の需要は、予測期間中に大きく成長するものと思われます。

セメント板業界のセグメンテーション

セメント板市場は部分的に細分化されています。主な企業(順不同)には、James Hardie Industries PLC、Etex Group、Saint-Gobain、Johns Manville、NICHIHAが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 住宅および商業建築における採用の増加

- 耐衝撃性と耐久性という望ましい特性

- その他の促進要因

- 市場抑制要因

- 従来の競合品と比較して高い初期コスト

- その他の阻害要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ別

- ファイバーセメント板(FCB)

- ウッドウールセメント板(WWCB)

- ウッドストランドセメント板(WSCB)

- セメント接着パーティクルボード(CBPB)

- 用途別

- フローリング

- 外壁および間仕切り壁

- 屋根材

- 柱・梁

- ファサード、ウェザーボード、クラッディング

- 遮音・断熱材

- その他の用途(プレハブ住宅、常設シャッター、耐火構造など)

- エンドユーザー産業別

- 住宅用

- 商業

- 産業・施設

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Etex Group

- Elementia Materials

- Everest Industries Limited

- James Hardie Industries PLC

- Johns Manville

- Knauf Gips KG

- Saint-Gobain

- BetonWood SRL

- Cembrit Holding A/S

- HIL Limited

- GAF

- NICHIHA Co. Ltd

第7章 市場機会と今後の動向

- 審美性向上のための動向の高まり

- その他の機会

目次

Product Code: 62218

The Cement Board Market size is estimated at 670.39 million square meters in 2025, and is expected to reach 860.92 million square meters by 2030, at a CAGR of 5.13% during the forecast period (2025-2030).

Key Highlights

- The increasing adoption in residential and commercial construction and desirable properties of impact resistance and durability are expected to drive the cement board market during the forecast period.

- However, the high initial cost compared to its traditional counterparts is expected to hinder market growth.

- Nevertheless, the rising trends for aesthetic improvement are expected to create new opportunities for the market.

- Asia-Pacific is expected to dominate the market, with the majority of demand coming from China and India.

Cement Board Market Trends

Increasing Adoption in Residential and Commercial Construction

- Cement boards offer a unique combination of durability, fire resistance, moisture resistance, and cost-effectiveness, making them a popular choice for residential construction.

- The commercial segment stands out as a pivotal player in the cement board market, with the office sector leading the way. As global commercial activities surge, so does the demand for cement boards in this segment.

- Asia-Pacific, a burgeoning hub for office spaces, ranks among the top markets in commercial construction. Countries like India and China have seen a consistent uptick in demand for office spaces, driven by sectors such as technology, e-commerce, and banking, leading to a flurry of new office constructions.

- India's burgeoning startup ecosystem highlights an increasing appetite for office spaces. Bolstered by government initiatives, the Department for Promotion of Industry and Internal Trade (DPIIT) recognized a remarkable 1,17,254 startups by December 2023.

- The United States is also a huge market for the building and construction industry. As per the data from the US Census Bureau, in 2023, the United States spent over USD 706.1 billion on new private non-residential buildings, a significant increase from USD 596.5 billion in 2022. Moreover, the residential construction in 2023 was only USD 864.9 billion.

- In 2023, an estimated 1,469,800 housing units were authorized by building permits, 11.7% below the 2022 figure of 1,665,100. Moreover, an estimated 1,413,100 housing units were started in 2023, 9% (+-2.5%) below the 2022 figure of 1,552,600.

- In July 2024, the seasonally adjusted annual rate for privately-owned housing units authorized by building permits stood at 1,396,000. This figure represents a 4% decline from the revised June rate of 1,454,000 and a 7% drop compared to the July 2023 rate of 1,501,000.

- Germany's robust economy is fueling a demand for commercial spaces, especially high-quality, ESG-compliant office buildings, which is evident from rising prime rents. In Q3 2023, 246,000 square meters of office space were completed, with projections reaching 1.8 million sq. m by 2024. Retail space development, particularly in shopping centers, also saw consistent growth in 2023.

- Brazil's residential sector is drawing substantial private investments fueled by swift urbanization. In response to this burgeoning demand, the government reintroduced the "Minha Casa, Minha Vida" (My Home, My Life) program in February 2023, setting an ambitious goal of 2 million new projects by 2026.

- Saudi Arabia is witnessing a construction boom, highlighted by the Jeddah Central megaproject. Spearheaded by the Jeddah Central Development Company (JCDC), a subsidiary of the Public Investment Fund (PIF), this ambitious USD 20 billion project includes landmarks like a museum, opera house, and sports stadium, alongside 17,000 residential units and over 3,000 hotels. The first phase is set for completion in 2027, with further developments extending to 2030 and beyond.

- These dynamics underscore a robust demand for cement boards in both residential and commercial construction globally, with promising growth during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Asia-Pacific holds a dominant position in the global cement board market, led by China. Cement boards find extensive applications in China's diverse construction activities, spanning both residential and commercial sectors.

- China is actively pursuing urbanization, aiming for a 70% urban rate by 2030. This urbanization drives a demand for more living spaces and reflects the middle class's aspirations for better living conditions. Such dynamics are set to boost the housing market and residential construction, positively influencing the cement board market.

- In Hong Kong, China, housing authorities have initiated multiple measures to kickstart the construction of affordable housing. Officials have set a target to deliver 301,000 public housing units by 2030.

- With plans to relocate 250 million rural residents to new megacities by 2025, the Chinese government's ambitious construction initiatives are set to boost the cement board market.

- In response to a struggling economy, Chinese governors are ramping up budgets for major building projects by nearly 20%. Over two-thirds of China's regions have committed to significant projects, including transportation infrastructure and industrial zones, with a combined budget exceeding CNY 12.2 trillion (USD 1.8 trillion) for 2024.

- Rising disposable incomes in China are fueling the demand for upscale commercial spaces, including malls and hotels. China stands at the forefront of shopping center development, boasting nearly 4,000 existing centers and an estimated 7,000 more by 2025. Projects like the Wuhan Fosun Bund Center T1, with construction starting in Q3 2021 and completion slated for Q4 2025, further bolster the market.

- India is set to witness a 70% surge in the availability of affordable housing. According to Invest India, the construction sector is projected to attain a valuation of USD 1.4 trillion by 2025. With forecasts suggesting that over 30% of the population will be urban dwellers by 2030, there is a pressing need for 25 million more mid-end and affordable housing units. Recent reforms, such as the Real Estate Act, GST (goods and services tax), and REITs (real estate investment trusts), aim to expedite approvals and strengthen the construction industry, driving market growth.

- South Korea is undertaking significant industrial construction ventures. A notable example is S-Oil Corp.'s ambitious Shaheen refinery-integrated petrochemical plant in Ulsan, set to finish by 2026. This facility will house the world's largest naphtha-fed steam cracker, capable of producing 1.8 million mt/year of ethylene, underscoring the project's potential to elevate industrial demand and support market growth.

- Given these dynamics, the demand for cement boards in Asia-Pacific is poised for significant growth during the forecast period.

Cement Board Industry Segmentation

The cement board market is partially fragmented in nature. The major players (not in any particular order) include James Hardie Industries PLC, Etex Group, Saint-Gobain, Johns Manville, and NICHIHA Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Adoption in Residential and Commercial Construction

- 4.1.2 Desirable Properties of Impact Resistance and Durability

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 High Initial Cost in Comparison to Traditional Counterparts

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Product Type

- 5.1.1 Fiber Cement Board (FCB)

- 5.1.2 Wood Wool Cement Board (WWCB)

- 5.1.3 Wood Strand Cement Board (WSCB)

- 5.1.4 Cement Bonded Particle Board (CBPB)

- 5.2 By Application

- 5.2.1 Flooring

- 5.2.2 Exterior and Partition Walls

- 5.2.3 Roofing

- 5.2.4 Columns and Beams

- 5.2.5 Facades, Weatherboard, and Cladding

- 5.2.6 Acoustic and Thermal Insulation

- 5.2.7 Other Applications (Prefabricated Houses, Permanent Shuttering, Fire-resistant Construction, etc.)

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial and Institutional

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Etex Group

- 6.4.2 Elementia Materials

- 6.4.3 Everest Industries Limited

- 6.4.4 James Hardie Industries PLC

- 6.4.5 Johns Manville

- 6.4.6 Knauf Gips KG

- 6.4.7 Saint-Gobain

- 6.4.8 BetonWood SRL

- 6.4.9 Cembrit Holding A/S

- 6.4.10 HIL Limited

- 6.4.11 GAF

- 6.4.12 NICHIHA Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Trends for Aesthetic Improvement

- 7.2 Other Opportunities

セメント板- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日