|

市場調査レポート

商品コード

1687354

インドのチョコレート:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)India Chocolate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのチョコレート:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 158 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

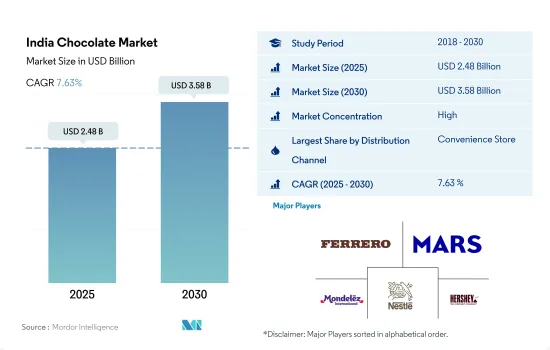

インドのチョコレート市場規模は2025年に24億8,000万米ドルと推定され、2030年には35億8,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは7.63%で成長する見込みです。

コンビニエンスストアはアクセスのしやすさから、全国で販売チョコレートの主要シェアを占める

- コンビニエンスストアは、インドでチョコレートを購入する際に最も広く好まれている流通チャネルです。コンビニエンスストアは住宅地や商業地域の近くにあるため非常に近づきやすく、一般的に手頃な価格のチョコレートを提供しています。コンビニエンスストアにおけるチョコレートの販売額は、2023年には2022年比で7%増加しました。

- スーパーマーケットとハイパーマーケットは、インドのチョコレート市場で2番目に大きな小売チャネルです。都市化の進展とスマートシティ開発政策が、国内のスーパーマーケットとハイパーマーケットの拡大を促進しています。ミルクチョコレートとホワイトチョコレートは、スーパーマーケットとハイパーマーケットを通じて販売される菓子が多く、2023年の市場数量シェアは77.74%です。

- Reliance Retail、Future Retail、D-Mart、Big Bazar、Hypercityなどが国内の大手スーパーマーケット事業者です。これらの事業者の全国的なネットワークにより、地元のチョコレート・ブランドと主流チョコレート・ブランドの両方へのアクセスが容易になっています。2023年現在、Big Bazarはインド国内で285以上の店舗を運営しています。また、D-Martは全国で約200のスーパーマーケットを運営しています。

- オンライン・チャネルは、予測期間中に最も急成長する流通チャネルとして認識されています。同国におけるチョコレートのオンライン販売はCAGR 9.04%を記録し、2030年には4,667万米ドルに達すると予想されています。インターネットの普及に伴うオンライン買い物客の増加が、同国における主要な市場促進要因として認識されています。また、消費者はオンラインプラットフォームが提供する利便性と迅速な配達を選ぶようになっています。2023年現在、インドの家庭消費者の3%が配達料を支払い、30分以内に食料品を配達してもらっており、11%の消費者は3時間まで待ち、少額の配達料を支払っています。

インドのチョコレート市場動向

ナッツ入りチョコレートの人気の高まりは強力な広告費に支えられています。

- インドのチョコレート市場は、伝統的な甘い嗜好品からの消費者嗜好の変化、可処分所得の増加、プレミアム製品に対する消費者の期待の高まり、健康に対する意識の高まりなど、さまざまな要因によって需要と消費が急増しています。

- 顧客ベースを拡大するため、主要市場プレーヤーは、プレミアム・カカオ、ユニークなフレーバー、フルーツやナッツ、キャラメル、塩ベースや砂糖不使用の選択肢を含むオーガニック成分を含む斬新な製品ラインを導入しており、市場の有望な見通しをもたらしています。

- 平均的なチョコレート・バーの小売販売額は1~10米ドルです。チョコレートを作るにはカカオ豆が主原料となるが、その価格は天候や収穫量、インドの需要など、さまざまな要因によって変動します。

- 消費者の健康意識の高まりにより、健康効果を高めたチョコレート製品に対する需要が増加しています。2022年現在、インド人の大多数(44%)は、関連する健康上の利点により、より高品質なチョコレートへの投資を望んでいます。

インドのチョコレート産業概要

インドのチョコレート市場はかなり統合されており、上位5社で75.71%を占めています。この市場の主要企業は以下の通りです。Ferrero International SA, Mars Incorporated, Mondelez International Inc., Nestle SA and The Hershey Company(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子類

- ダークチョコレート

- ミルクチョコレートとホワイトチョコレート

- 流通チャネル

- コンビニエンスストア

- オンラインストア

- スーパーマーケット/ハイパーマーケット

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Chocoladefabriken Lindt & Sprungli AG

- DS Group

- Ferrero International SA

- Gujarat Co-operative Milk Marketing Federation Ltd.

- ITC Limited

- Mars Incorporated

- Mondelez International Inc.

- Nestle SA

- Reliance Industries Ltd

- Surya Food & Agro Ltd

- The Hershey Company

- YIldIz Holding AS

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The India Chocolate Market size is estimated at 2.48 billion USD in 2025, and is expected to reach 3.58 billion USD by 2030, growing at a CAGR of 7.63% during the forecast period (2025-2030).

Convenience stores accounted for major share of sales chocolate across the country due to easy accessibility

- Convenience stores are the most widely preferred distribution channels for purchasing chocolates in India. Convenience stores are very easy to approach as they are located near residential and commercial areas and generally offer affordable chocolates. The sales value of chocolates in convenience stores increased by 7% in 2023 compared to 2022.

- Supermarkets and hypermarkets are the second-largest retail channels in India's chocolate market. The rising urbanization and smart city development policies are promoting the expansion of supermarkets and hypermarkets in the country. Milk and white chocolate are largely sold confections through supermarkets and hypermarkets, with a market volume share of 77.74% in 2023.

- Reliance Retail, Future Retail, D-Mart, Big Bazar, Hypercity, and others are some of the leading supermarket operators in the country. A nationwide network of these operators allows easy access to both local and mainstream chocolate brands. As of 2023, Big Bazar operates more than 285 stores in India. Also, D-Mart operates around 200 supermarkets across the country.

- Online channels are identified as the fastest-growing distribution channel during the forecast period. Online sales of chocolates in the country are expected to register a CAGR of 9.04%, reaching USD 46.67 million by 2030. An increasing number of online shoppers in response to internet penetration is identified as the key market driver in the country. Also, consumers are increasingly opting for the convenience and fast delivery that online platforms offer. As of 2023, 3% of household consumers in India paid the delivery fee and got groceries delivered within 30 minutes, and 11% of consumers waited up to 3 hours and paid a small delivery fee.

India Chocolate Market Trends

The growing popularity of nut-infused chocolates is supported by strong spending on advertising

- The Indian market for chocolates is experiencing a surge in demand and consumption due to a variety of factors, including a shift in consumer preferences away from traditional sweet indulgences, increasing disposable income, increasing consumer expectations of premium products, and a heightened awareness of health concerns.

- To expand their customer base, key market players are introducing novel product lines with premium cocoa, unique flavors, and organic components, including fruit and nuts, caramel, and salt-based and sugar-free options, thus providing a promising outlook for the market.

- The retail sales value of an average chocolate bar ranges between USD 1 to USD 10. For making chocolates, cocoa beans are the main ingredients, and their price can vary depending on a number of factors such as weather, the harvest, and demand in India.

- The increasing awareness of consumer health has resulted in an increase in the demand for chocolate products with enhanced health benefits. As of 2022, a majority of Indians (44%) were willing to invest in higher-quality chocolates due to their associated health benefits.

India Chocolate Industry Overview

The India Chocolate Market is fairly consolidated, with the top five companies occupying 75.71%. The major players in this market are Ferrero International SA, Mars Incorporated, Mondelez International Inc., Nestle SA and The Hershey Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Dark Chocolate

- 5.1.2 Milk and White Chocolate

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Chocoladefabriken Lindt & Sprungli AG

- 6.4.2 DS Group

- 6.4.3 Ferrero International SA

- 6.4.4 Gujarat Co-operative Milk Marketing Federation Ltd.

- 6.4.5 ITC Limited

- 6.4.6 Mars Incorporated

- 6.4.7 Mondelez International Inc.

- 6.4.8 Nestle SA

- 6.4.9 Reliance Industries Ltd

- 6.4.10 Surya Food & Agro Ltd

- 6.4.11 The Hershey Company

- 6.4.12 YIldIz Holding AS

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms