パインケミカル:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Pine Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687343

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

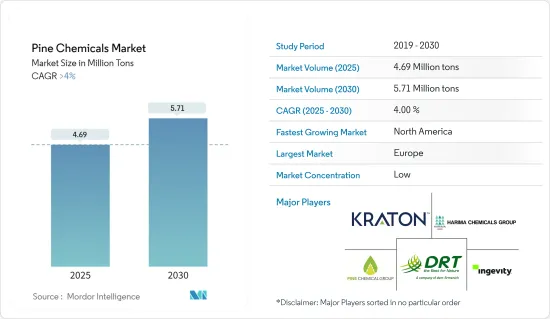

パインケミカルの市場規模は2025年に469万トンと推計され、予測期間中(2025-2030年)のCAGRは4%を超え、2030年には571万トンに達すると予測されます。

COVID-19はパインケミカル市場にさまざまな影響を与えました。当初は、サプライチェーンの混乱、産業活動の低下、個人消費の減少により需要が減少しました。このため、パインケミカルの生産と販売は一時的に減速しました。しかし、パンデミックが進行するにつれ、特定の松由来製品、特に消毒剤、除菌剤、医薬品に使用される製品に対する需要が増加しました。

鉱業部門と香料業界からのパインケミカルに対する需要の増加は、パインケミカル市場を牽引する主な要因です。

しかし、安価な代替品の増加や原料価格の変動は、パインケミカル市場の成長を妨げると予想されます。

様々なエンドユーザー産業におけるパインケミカルの用途拡大は、パインケミカル市場に新たな機会をもたらすと予想されます。

欧州は、ドイツやイタリアなどの国々からの消費が最も大きく、世界のパインケミカル市場を独占すると予想されます。

パインケミカル市場の動向

接着剤とシーラントセグメントが市場を独占する見込み

パインケミカル、特にロジンとその誘導体は優れた粘着特性を示し、接着剤とシーリング剤の理想的な原料となっています。これらの製品は接着強度と凝集力を高め、性能と耐久性を向上させる。

マツ由来の化学物質は、建築、自動車、包装、木工、電子機器などの産業において、多様な接着剤やシーリング剤の配合に使用されています。感圧接着剤、ホットメルト接着剤、ゴム系接着剤などの製品に利用されています。

さらに、建設業界の成長が接着剤とシーリング剤の消費を促進し、パインケミカル市場の成長を後押ししています。中国は世界最大の建設市場のひとつです。国家統計局(NBS)によると、中国の建設業界の事業活動指数は2023年11月の55.9から12月時点で56.9に上昇しました。

パインケミカルは、建築におけるコーキング、目地シーリング、耐候性に使用されるシーラントの調合における主要成分です。トール油ベースのシーリング材は、コンクリート、石積み、ガラス、金属など幅広い基材に優れた接着性を発揮するため、建物の外壁、窓、ドア、屋根の隙間、ひび割れ、目地などのシーリングに実用的です。

インドの建設産業は、2025年までに1兆4,000億米ドルに成長すると予測されています。2030年までに、推定6億人が都市中心部に住むようになり、その結果、中・超高級住宅が2,500万戸追加される必要があります。国家投資計画(NIP)の下、インドのインフラ投資予算は1兆4,000億米ドルで、予算の24%が再生可能エネルギー、道路・高速道路、都市インフラ、12%が鉄道に当てられています。

このように、自動車産業や建設産業における接着剤とシーリング剤の用途の増加は、今後数年間の市場調査を後押しすると予想されます。

市場を独占する欧州地域

欧州には広範な松林があり、特にスウェーデン、フィンランド、ロシア、バルト三国などに多いです。これらの森林は松脂の豊富な供給源であり、松脂は松脂化学製品の原料となります。豊富で持続可能なパイン資源を利用できるため、欧州の生産者は世界市場で競争優位に立つことができます。

欧州の企業は、接着剤、シーリング剤、塗料、コーティング剤、印刷インキ、パーソナルケア製品、医薬品など、パインケミカルを利用する幅広い産業と用途に対応しています。最終用途産業が多様であるため、同地域におけるパインケミカルの需要は安定しています。

さらに、パイン由来の樹脂は建築用接着剤の粘着剤として一般的に使用されています。これらの接着剤は、木材、金属、コンクリート、プラスチックなど、さまざまな建築材料の接着に使用されます。これらの接着剤は強力で耐久性があるため、建築における構造用および非構造用の用途に理想的です。

ユーロ統計局が発表した最新の推計によると、2023年12月の建設業生産は2022年12月と比べ、ユーロ圏で1.9%、欧州で2.4%増加しました。

ドイツは一般ゴム製品(GRG)とタイヤの欧州最大級の生産国です。コンチネンタルAG、ダンロップGmbH、ミシュランタイヤAG &Co.KGaA、Pirelli Deutschland GmbH、およびFreudenberg Groupは、ドイツにおけるタイヤおよび非タイヤ製品の主要メーカーの一部です。

ドイツ連邦統計局(Statistisches Bundesamt)が2023年6月に発表した推計によると、2022年現在、ドイツの建設業の売上高は、土木や特定建設業の売上高を上回っています。土木工事で最も売上高が多いのは道路・鉄道工事で210億ユーロ(228億3,000万米ドル)以上、公共事業は120億ユーロ(130億4,000万米ドル)でした。

このように、上記の要因によって、主に欧州地域のパインケミカル市場の需要が促進されると予想されます。

パインケミカル業界の概要

パインケミカル市場は断片化されており、上位5社が大きな市場シェアを占めています。市場の主要企業(順不同)には、KRATON CORPORATION、Ingevity Corporation、DRT、Harima Chemicals Group Inc.、Pine Chemical Groupなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 鉱業、浮遊化学、潤滑油におけるパインケミカル需要の増加

- 香料産業からの需要増加

- 抑制要因

- 政府の奨励策によるCTOのバイオ燃料への転用

- より安価な代替品の増加

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ

- トール油

- 粗トール油(CTO)

- トール油脂肪酸(TOFA)

- 蒸留トール油(DTO)

- トール油ピッチ(TOP)

- ロジン

- トール油ロジン

- ガムロジン

- ウッドロジン

- ターペンタイン

- ガム・ウッドターペンタイン

- 粗製硫酸ターペンタイン

- その他のターペンタイン

- 用途

- 接着剤およびシーラント

- 塗料

- 印刷インキ

- 潤滑油・潤滑添加剤

- バイオ燃料

- 紙のサイジング

- ゴム

- 石鹸および洗剤

- その他の用途(油田用化学品、化学添加物、チューインガム、食品添加物)

- トール油

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェアランキング分析

- 主要企業の戦略

- 企業プロファイル(概要、財務、製品・サービス、最近の動向)

- Arakawa Chemical Industries Ltd

- DRT(Derives Resiniques et Terpeniques)

- Forchem Oyj

- Harima Chemicals Group Inc.

- Ingevity Corporation

- Kraton Corporation

- Mercer International

- OOO Torgoviy Dom Lesokhimik

- Pine Chemical Group

- Respol Resinas SA

- Sunpine AB

- Synthomer Plc.

第7章 市場機会と今後の動向

- パインケミカルの新たな用途(DTO、TOFA、CTO、TOP、ウッドロジン)

- 接着剤とシーラントの食品・包装安全規制

目次

The Pine Chemicals Market size is estimated at 4.69 million tons in 2025, and is expected to reach 5.71 million tons by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

COVID-19 has had mixed effects on the pine chemicals market. Initially, demand decreased due to disruptions in supply chains, reduced industrial activity, and lower consumer spending. This led to temporary slowdowns in the production and sales of pine chemicals. However, as the pandemic progressed, there was an increased demand for certain pine-derived products, particularly those used in disinfectants, sanitizers, and pharmaceuticals.

Increasing demand for pine chemicals from the mining sector and the flavors and fragrances industry are the major factors driving the pine chemicals market.

However, an increase in the availability of cheaper substitutes and fluctuations in the price of raw materials are expected to hamper the growth of the pine chemicals market.

The expanding applications of pine chemicals in various end-user industries are expected to unveil new opportunities for the pine chemicals market.

Europe is expected to dominate the pine chemicals market globally, with the most significant consumption coming from countries such as Germany and Italy.

Pine Chemicals Market Trends

The Adhesives and Sealants Segment is expected to Dominate the Market

Pine chemicals, particularly rosin and its derivatives, exhibit excellent tackifying properties, making them ideal ingredients for adhesives and sealants. They enhance the adhesion strength and cohesion of these products, improving their performance and durability.

Pine-derived chemicals are used in a diverse range of adhesives and sealant formulations across industries such as construction, automotive, packaging, woodworking, and electronics. They are utilized in products like pressure-sensitive adhesives, hot-melt adhesives, rubber-based adhesives, and more.

Furthermore, the growth in the construction industry has propelled the consumption of adhesives and sealants, thus propelling the growth of the pine chemicals market. China is one of the world's largest construction markets. According to the National Bureau of Statistics (NBS), the construction industry's business activity index in China rose to 56.9 as of December 2023 from 55.9 in November 2023.

Pine chemicals are the key ingredient in the formulation of sealants used for caulking, joint sealing, and weatherproofing in construction. Tall oil-based sealants offer excellent adhesion to a wide range of substrates such as concrete, masonry, glass, and metal, making them practical for sealing gaps, cracks, and joints in building envelopes, windows, doors, and roofing systems.

India's construction Industry is projected to grow to USD 1.4 trillion by 2025. By 2030, an estimated 600 million people will live in urban centers, resulting in a need for 25 million additional mid- and ultra-luxury units. Under the National Investment Plan (NIP), India has an infrastructure investment budget of USD 1.4 trillion, with 24% of the budget earmarked for renewable energy, roads & highways, urban infrastructure, and 12% for railways.

Thus, the rising application of adhesives and sealants in the automotive and construction industries is expected to boost the market studied in the coming years.

Europe Region to Dominate the Market

Europe has extensive pine forests, particularly in countries like Sweden, Finland, Russia, and the Baltic States. These forests provide a rich source of pine resin, which serves as the raw material for pine chemical production. The availability of abundant and sustainable pine resources gives European producers a competitive advantage in the global market.

European companies cater to a wide range of industries and applications that utilize pine chemicals, including adhesives, sealants, paints, coatings, printing inks, personal care products, pharmaceuticals, and more. The diversity of end-use industries ensures a stable demand for pine chemicals within the region.

Further, pine-derived resins are commonly used as tackifiers in construction adhesives. These adhesives are then used to bond various construction materials, including wood, metal, concrete, and plastics. They provide strong and durable bonds, making them ideal for structural and non-structural applications in construction.

According to the latest estimate published by Eurostat, in December 2023, compared with December 2022, production in construction increased by 1.9% in the euro area and by 2.4% in Europe.

Germany is one of Europe's largest producers of general rubber goods (GRG) and tires. Continental AG, Dunlop GmbH, Michelin Tire Werke AG & Co. KGaA, Pirelli Deutschland GmbH, and Freudenberg Group are some of the significant manufacturers of tire and non-tire products in the country.

According to the estimate released by the Statistisches Bundesamt in June 2023, as of 2022, the turnover of the construction industry in Germany was higher than that of any civil engineering or specific construction sector. The highest turnover in civil engineering activities was for road and railway construction, at more than EUR 21 billion (USD 22.83 billion), and utility projects, which amounted to EUR 12 billion (USD 13.04 billion).

Thus, the factors mentioned above are expected to drive the market demand for pine chemicals, mainly from the European region.

Pine Chemicals Industry Overview

The pine chemicals market is fragmented, with the top five players accounting for a significant market share. The major players in the market (not in any particular order include) KRATON CORPORATION, Ingevity Corporation, DRT, Harima Chemicals Group Inc., and Pine Chemical Group, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Pine Chemicals in Mining and Flotation Chemicals and Lubricants

- 4.1.2 Increasing Demand from the Flavors and Fragrances Industry

- 4.2 Restraints

- 4.2.1 Diversion of CTO to Biofuels due to Government Incentives

- 4.2.2 Increase in the Availability of Cheaper Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Threat of New Entrants

- 4.4.3 Threat of Substitute Products and Services

- 4.4.4 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Tall Oil

- 5.1.1.1 Crude Tall Oil (CTO)

- 5.1.1.2 Tall Oil Fatty Acid (TOFA)

- 5.1.1.3 Distilled Tall Oil (DTO)

- 5.1.1.4 Tall Oil Pitch (TOP)

- 5.1.2 Rosin

- 5.1.2.1 Tall Oil Rosin

- 5.1.2.2 Gum Rosin

- 5.1.2.3 Wood Rosin

- 5.1.3 Turpentine

- 5.1.3.1 Gum/Wood Turpentine

- 5.1.3.2 Crude Sulphate Turpentine

- 5.1.3.3 Other Turpentines

- 5.1.4 Application

- 5.1.4.1 Adhesives and Sealants

- 5.1.4.2 Coatings

- 5.1.4.3 Printing Inks

- 5.1.4.4 Lubricants and Lubricity Additives

- 5.1.4.5 Biofuels

- 5.1.4.6 Paper Sizing

- 5.1.4.7 Rubber

- 5.1.4.8 Soaps and Detergents

- 5.1.4.9 Other Applications (Oil Field Chemicals, Chemical additives, Chewing Gums, and Food Additives)

- 5.1.1 Tall Oil

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles(Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 Arakawa Chemical Industries Ltd

- 6.4.2 DRT (Derives Resiniques et Terpeniques)

- 6.4.3 Forchem Oyj

- 6.4.4 Harima Chemicals Group Inc.

- 6.4.5 Ingevity Corporation

- 6.4.6 Kraton Corporation

- 6.4.7 Mercer International

- 6.4.8 OOO Torgoviy Dom Lesokhimik

- 6.4.9 Pine Chemical Group

- 6.4.10 Respol Resinas SA

- 6.4.11 Sunpine AB

- 6.4.12 Synthomer Plc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications of Pine Chemicals (DTO, TOFA, CTO, TOP, and Wood Rosin)

- 7.2 Food and Packaging Safety Regulations of Adhesives and Sealants

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日