スーパーコンピューター:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Supercomputers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 103 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687334

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

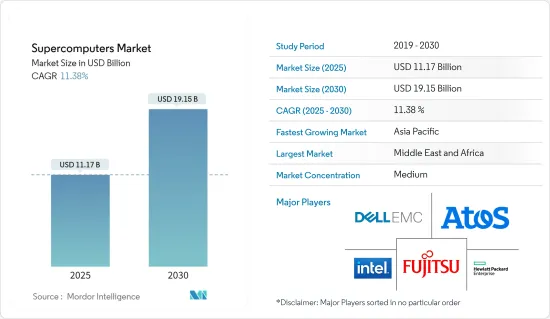

スーパーコンピューターの市場規模は2025年に111億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.38%で、2030年には191億5,000万米ドルに達すると予測されます。

高性能な処理能力を持つスーパーコンピューターは、人工知能(AI)プログラムを実行するための基幹機器として、ますますその存在感を増しています。そのアーキテクチャは、AIや機械学習アプリケーションの膨大なデータ要件を処理するのに長けています。

ハイパフォーマンスコンピューティング(HPC)アプリケーションの世界の利用拡大が市場を牽引

主なハイライト

- 膨大な計算能力とスピードで知られるスーパーコンピューターは、ハイパフォーマンスコンピューティング(HPC)システムで重要な役割を果たしています。その性能から、HPC分野では欠かせない存在となっています。科学研究がシミュレーションベースの技術に傾き、機械学習(ML)の重要性が高まる中、スーパーコンピューターに対する市場の需要は顕著に増加しています。

- さらに2024年10月、NVIDIAの株価は、最新のスーパーコンピューティング用AIチップ「Blackwell」の旺盛な需要に対する楽観的な見方の高まりに後押しされ、史上最高値を更新しました。これは、スーパーコンピューターの有望な成長軌道を強調し、市場全体の拡大を後押ししています。

- 組織が複雑なデータセットや分析ワークロードに取り組むにつれて、スーパーコンピューターの需要は高まると思われます。スーパーコンピューターは、教育研究機関にとってより身近で費用対効果の高いものとなりつつあります。さらに、特にクラウドコンピューティングに対応したPlatform-as-Serviceモデルを通じて、コンピューティングパワーを民主化する傾向が強まっていることも、市場をさらに押し上げる要因となっています。

スーパーコンピューティングシステムの初期コストの高さが市場成長の主な阻害要因

主なハイライト

- デバイスの価格、ハウジングインフラ、運用費用を含む所有コストの高さが、スーパーコンピューターを高価なものとし、市場成長の障害となっています。例えば、2024年3月、MicrosoftとOpenAIは、約1,000億米ドルのAIベースのスーパーコンピューターを共同で構築しました。これは、このようなスーパーコンピューターが主に大企業向けであり、中小企業には実現不可能であることを示しています。

各国間の地政学的対立が市場成長に影響を与える可能性

主なハイライト

- サイバー防衛と攻撃を強化するための防衛部門におけるスパコン需要が、政府部門の市場成長を支えています。さらに、2024年4月、米国国務省のサイバーセキュリティ担当者が異常な活動を検知し、中国が量子スーパーコンピューターを開発したことが明らかになりました。この進化は、欧米の暗号をすべて破壊することが可能であり、それによってサイバー防衛を無効化することができます。

スーパーコンピューターの市場動向

商業産業が最大のエンドユーザーに

- 自動車会社は、業務用スーパーコンピューターを急速に活用しています。グローバルベンダーと自動車会社は、業界固有のニーズに対応するために、これらのアプリケーションをカスタマイズしています。自動車分野におけるスパコンの主な用途には、衝突解析、構造解析、数値流体力学などがあります。これらにより、製品の品質が大幅に向上し、コストが削減され、以前は克服できなかった課題に取り組むことができるようになりました。業界の熾烈な競合を考えると、スーパーコンピューターの導入は世界の自動車セクターのベンダーにとって不可欠なものとなっています。

- 例えば、Teslaは2024年2月、ニューヨーク州バッファローのRiverbend GigafactoryにDojoスーパーコンピューターを設置するため、5億米ドルを投資すると発表しました。このスーパーコンピューターは、自律走行に不可欠なTeslaの人工知能(AI)システムを訓練します。主要なコンピューティングプラットフォームとして期待され、機械学習モデルを訓練し、テスラの電気自動車から得られる膨大なデータを処理します。

- エネルギー分野では、スーパーコンピューター、特にアクセラレータを搭載したスーパーコンピューターが、ハイパフォーマンスコンピューティング(HPC)ワークロードのエネルギー効率を高めます。膨大なデータセットを処理し、より高解像度の画像を得るための新しいアルゴリズムが開発されています。この進歩は、特にブラジル、メキシコ湾、アンゴラ、東地中海のような厳しい地質環境において、地下の炭化水素の位置を正確に特定するのに役立ちます。企業は、探鉱鉱区や資産の機会を早期に評価することで、より選択的に事業を進めることができます。

著しい成長が期待されるアジア太平洋地域

- アジア太平洋地域は、特にスーパーコンピューティングシステムの開発において、技術進歩のリーダーとして急速に台頭しており、中国や日本などの国々が大きく貢献しています。

- アジア太平洋地域では、急速な経済成長、研究開発(R&D)への多額の投資、高度な計算能力に対する需要の高まりが、ハイパフォーマンスコンピューティング(HPC)の一貫した導入と開発に拍車をかけています。

- 中国の研究チームは、ガウス粒子のランダムサンプリングによって最大76個の光子を識別できる量子コンピューターのプロトタイプを作成しました。この前衛技術の覇権をめぐり、中国の研究者たちはGoogle、Amazon、Microsoftといった米国の大手企業に挑戦しています。インドもまた、アジア太平洋の舞台で注目すべき進歩を遂げています。同国は国家スーパーコンピューティングミッションを開始し、2023年までに7億3,000万米ドルの投資を見込んで、73の高性能コンピューティング施設を備えたスーパーコンピューティンググリッドの構築を目標としています。

- 2024年2月、中国は世界最強のマシンと謳われるスーパーコンピューター「Tianhe-3」をひそかに公開しました。広州にある国立スーパーコンピューターセンターのために開発されたこのマシンは、その秘密主義的な性質からさまざまな憶測を呼んでいます。Xingyiと名付けられたTianhe-3は、中国国防科技大学が製作したスーパーコンピューターシリーズの最新作です。

- 2024年9月、インドは技術的な旅路における重要な飛躍となるパラルドラスーパーコンピューティングシステムを立ち上げました。先進コンピューティング開発センター(C-DAC)が開発したこの先進的な施設は、特に気象・気候コンピューティングにおけるインドの高性能コンピューティング能力を強化します。

- シンガポール政府は2024年10月、国家スーパーコンピューティングインフラの強化に向けて2億7,000万シンガポールドル(2億170万米ドル)を拠出することを発表しました。この投資は、シンガポールの国立スーパーコンピューティングセンター(NSCC)の能力を強化し、地元の研究イニシアチブを確実にサポートすることを目的としています。この発表は、ASPIRE 2Aおよび2A+システムの公式発表の中で、国立研究財団(NRF)の理事長でもある同国の副首相によって行われました。これらの先進的な研究用スーパーコンピューターはNSCCの管理下にあります。こうした進展は、予測期間中の同地域のスーパーコンピューター市場の成長を後押しすることになると思われます。

スーパーコンピューター産業の概要

同市場は、複数の世界的・地域的プレーヤーによって構成されており、競争の激しい領域で注目を集めようとしています。しかし、大きな市場シェアを持つ大手ベンダーが支配的であり、さまざまな地域市場で足場を固め、パイオニアになろうと競い合っています。

ベンダーは競争戦略を採用し、技術革新とR&Dへの投資能力を武器に市場での足場を固めています。したがって、この戦略は市場での競争を激化させます。

流通チャネルへのアクセス、既存の取引関係、より優れたサプライチェーン知識、高性能コンピューティングソリューションの開発は、既存のハイテク大手企業に、新規参入企業に対する市場優位性を与えています。全体として、ベンダー間の競争企業間の敵対関係は高く、予測期間中も変わらないと予想されます。

主な市場プレイヤーとしては、Atos SE、Intel Corporation、Hewlett Packard Enterprise Company、Dell EMC(Dell Technologies Inc.)、Fujitsu Limitedなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- マクロ経済要因が市場に与える影響の評価

第5章 市場力学

- 市場促進要因

- 処理能力の向上に対する需要の高まり

- 研究投資の増加

- 市場抑制要因

- 初期設定コストの高さ

- 広い設置スペース

第6章 市場セグメンテーション

- エンドユーザー別

- 商業産業

- 政府機関

- 研究機関

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Atos SE

- Intel Corporation

- Hewlett Packard Enterprise

- Dell EMC(Dell Technologies Inc.)

- Fujitsu Ltd

- IBM Corporation

- Lenovo Group Limited

- NEC Corporation

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Supercomputers Market size is estimated at USD 11.17 billion in 2025, and is expected to reach USD 19.15 billion by 2030, at a CAGR of 11.38% during the forecast period (2025-2030).

Supercomputers, with their high-performance processing capabilities, are increasingly becoming the backbone for running artificial intelligence (AI) programs. Their architecture is adept at handling the extensive data requirements of AI and machine learning applications.

The Growth In The Usage Of High-performance Computing (HPC) Applications Worldwide Will Drive The Market

Key Highlights

- Supercomputers, known for their immense computational power and speed, play a crucial role in high-performance computing (HPC) systems. Their capabilities make them indispensable in the HPC landscape. With scientific research leaning more towards simulation-based techniques and the rising importance of machine learning (ML), the market demand for supercomputers has seen a notable uptick.

- Additionally, in October 2024, NVIDIA's shares reached an all-time high, fueled by rising optimism regarding the robust demand for its latest supercomputing AI chips, Blackwell. This underscores the promising growth trajectory of supercomputers, bolstering the overall market expansion.

- As organizations grapple with complex data sets and analytics workloads, the demand for supercomputers will rise. Supercomputers are now becoming more accessible and cost-effective for educational research institutions. Furthermore, the growing trend of democratizing computing power, especially through cloud-computing-enabled platform-as-service models, is set to boost the market further.

The High Initial Cost Of Supercomputing Systems Is The Major Hindrance To Market Growth

Key Highlights

- High ownership costs, encompassing the device's price, housing infrastructure, and operational expenses, render supercomputers expensive and challenge market growth. For example, in March 2024, Microsoft and OpenAI collaborated to build an AI-based supercomputer costing approximately USD 100 billion. This shows that such supercomputers cater predominantly to large corporations, making them unfeasible for small and medium-sized enterprises.

The Impact Of Geopolitical Conflicts Among Countries Can Impact The Market Growth

Key Highlights

- The demand for supercomputers in defense departments to increase cyber defense and attack supports the government sector's market growth. Additionally, in April 2024, a cybersecurity official at the US State Department detected unusual activity, revealing that China had developed a quantum supercomputer. This advancement can destroy all Western encryption, thereby nullifying their cyber defenses.

Supercomputers Market Trends

Commercial Industries to be the Largest End Users

- Automotive companies are rapidly utilizing commercial supercomputers in their applications. Global vendors and automobile companies have tailored these applications to cater to the industry's unique needs. Key applications of supercomputers in the automotive sector include crash analysis, structural analysis, and computational fluid dynamics. These have significantly enhanced product quality, reduced costs, and tackled previously insurmountable tasks. Given the industry's fierce competitiveness, the adoption of supercomputers has become essential for vendors in the global automotive sector.

- For instance, in February 2024, Tesla announced a USD 500 million investment to install a Dojo supercomputer at its Riverbend Gigafactory in Buffalo, New York. This supercomputer will train Tesla's Artificial Intelligence (AI) systems, crucial for autonomous driving. Anticipated as a major computing platform, it will train machine learning models and process vast data volumes from Tesla's electric vehicles.

- In the energy sector, supercomputers, especially those with attached accelerators, enhance energy efficiency in High-performance Computing (HPC) workloads. New algorithms are being developed to process extensive datasets, yielding higher-resolution images. This advancement aids in accurately locating hydrocarbons underground, particularly in challenging geological environments like Brazil, the Gulf of Mexico, Angola, and the Eastern Mediterranean. Companies can be more selective in their ventures by assessing exploration acreage and asset opportunities early.

Asia Pacific Expected to Witness Significant Growth

- Asia Pacific is rapidly emerging as a leader in technological advancements, particularly in the development of supercomputing systems, with significant contributions from nations like China and Japan.

- In the Asia-Pacific, rapid economic growth, substantial investments in research and development (R&D), and an increasing demand for advanced computational capabilities have fueled the region's consistent adoption and development of high-performance computing (HPC).

- Researchers in China have crafted a prototype quantum computer that can identify up to 76 photons via random sampling of Gaussian bosons. In a bid for dominance in this avant-garde technology, China's researchers are challenging major US firms such as Google, Amazon, and Microsoft. India is also making notable advancements in the Asia-Pacific arena. The nation has initiated the National Supercomputing Mission, targeting the creation of a supercomputing grid with 73 high-performance computing facilities, backed by a projected investment of USD 730 million by 2023.

- In February 2024, China discreetly unveiled the Tianhe-3 supercomputer, touted as the world's most powerful machine. Developed for the National Supercomputer Center in Guangzhou, the machine's secretive nature has fueled widespread speculation. Dubbed "Xingyi," Tianhe-3 is the latest addition to a series of supercomputers crafted by China's National University of Defense Technology.

- In September 2024, India launched the Param Rudra Supercomputing System, a significant leap in its technological journey. This advanced facility, crafted by the Centre for Development of Advanced Computing (C-DAC), bolsters India's high-performance computing prowess, especially in weather and climate computing.

- In October 2024, the Singapore government unveiled its commitment of SGD 270 million (USD 201.7 million) towards the enhancement of its national supercomputing infrastructure. This investment aims to bolster the capabilities of the National Supercomputing Centre (NSCC) in Singapore, ensuring robust support for local research initiatives. The announcement was made by the country's Deputy Prime Minister, who also chairs the National Research Foundation (NRF), during the official launch of the ASPIRE 2A and 2A+ systems. These advanced research supercomputers are under the management of NSCC. These developments are set to bolster the growth of the supercomputer market in the region during the forecast period.

Supercomputers Industry Overview

The market comprises several global and regional players vying for attention in a contested space. However, it is dominated by major vendors that cover a significant market share and compete to gain a foothold and become pioneers in different regional markets.

Vendors adopt competitive strategies to gain a foothold in the market with innovation and the capability to invest in R&D, which is on the higher side. Thus, this strategy intensifies the competition in the market.

Access to distribution channels, existing business relationships, better supply chain knowledge, and the development of high-performance computing solutions give established tech giants a market advantage over new competitors. Overall, the intensity of competitive rivalry among the vendors is expected to be high and remain the same during the forecasted period.

Some of the major market players are Atos SE, Intel Corporation, Hewlett Packard Enterprise Company, Dell EMC (Dell Technologies Inc.), and Fujitsu Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment Of The Impact Of Macroeconomic Factors On The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Higher Processing Power

- 5.1.2 Increasing Investments in Research

- 5.2 Market Restraints

- 5.2.1 High Initial Setup Cost

- 5.2.2 Large Installation Space

6 MARKET SEGMENTATION

- 6.1 By End User

- 6.1.1 Commercial Industries

- 6.1.2 Government Entities

- 6.1.3 Research Institutions

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Atos SE

- 7.1.2 Intel Corporation

- 7.1.3 Hewlett Packard Enterprise

- 7.1.4 Dell EMC (Dell Technologies Inc.)

- 7.1.5 Fujitsu Ltd

- 7.1.6 IBM Corporation

- 7.1.7 Lenovo Group Limited

- 7.1.8 NEC Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 103 Pages

- 納期

- 2~3営業日